Retailer QVC (owned by Qurate Retail:QRTEA) has announced a new offering of $25/share baby bonds.

The Senior Secured Notes will have a maturity date way out in 2068.

The notes will trade under the ticker QVCC when they begin to trade.

The company has a 6.375% baby bond already outstanding (QVCD) which can be seen here. While we don’t see a new rating today the QVCD notes are low investment grade (BBB-) per S&P and a below investment grade per Moodys Ba2

UPDATE–This will be just a partial redemption of the issue–amount yet to be determined.

REIT VEREIT (VER) has announced a new senior note offering with the intent to call the 6.70% perpetual VER-F, monthly paying preferred.

This has been a favorite of mine–another one gone. It looks like a small loss of capital this morning as the shares are trading at $25.48–the monthly dividend is about 14 cents. This is a case where I have held a small position knowing the call risk was there–but which I chose to incur for the 6.70% coupon–I have held it for a fairly long time.

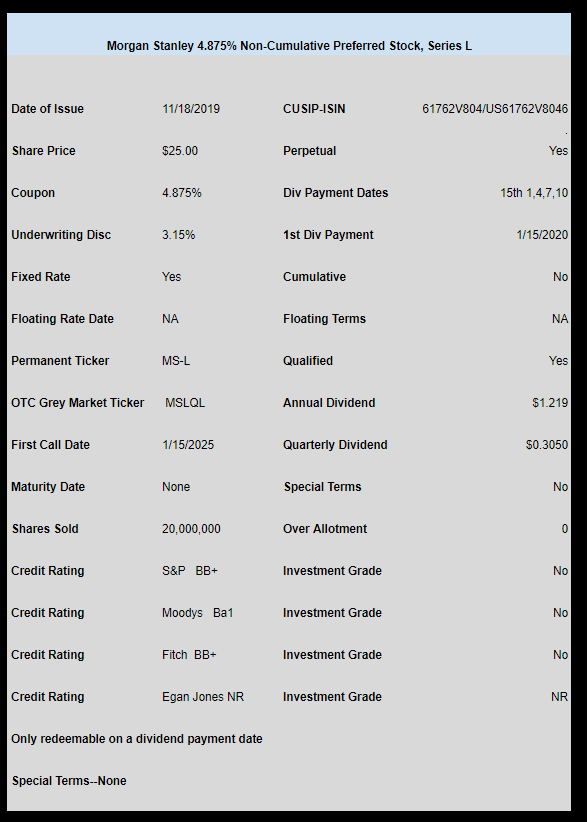

Morgan Stanley has priced their previously announced new fixed rate preferred.

The issue is non-cumulative, qualified, NON investment grade and 20 million shares priced at 4.875%.

With all the substandard coupons we have seen I should be used to being disappointed in these meager coupons–but I’m not!! If it was investment grade–then maybe 4.875% would be right–but they fall short of investment grade.

Oh well–it is what it is and my simple answer is –NO I won’t buy any.

Since the announcement came at the end of the day there will be some blood letting in these issues tomorrow morning–assuming they trade. If they do not trade holders will have to wait 5 weeks to be spanked.

The earnings for the quarter ending 9/30/2019 are pretty decent–as has been the norm in recent years. On revenue of $1.15 billion the company brought $156 million to the bottom line. Revenues grew 4% over the year ago quarter, but earnings were off 6%.

We do note that depreciation, a non cash charge, is always the one of the companies largest expenses, but unlike real estate companies the assets of the company do in fact depreciate and the company spends dramatic amounts of capital on replacement equipment. During the 1st 6 months of the fiscal year the company spent $1.6 billion on new equipment–obviously there are plenty of new UHAUL trucks running around the country.

Taking a look at the Amerco balance sheet should always bring comfort to investors. The company currently holds about $3.2 billion in cash and securities–nothing like cold, hard cash to make a lender (investors in the Investors Club) feel secure.

The companies common stock now trades at $366 giving the company a market cap of about $7 billion.

Morgan Stanley (MS) has announced a new non-cumulative preferred stock issue. The issue likely will be rated just below investment grade.

The shares will have an early redemption date starting 1/15/2025. The issue will only be redeemable on a dividend payment date.

The proceeds of this issue will be used to redeem the 6.625% preferred MS-G which is only redeemable on a dividend payment date – the next payment date is 1/15/2020.

The permanent ticker will be MS-L after it trades for a week or so on the OTC Grey market (temporary ticker not yet announced).

The stock market continues to party as the S&P500 hit new record highs last week trading in a range of 3075 to 3120 before closing on Friday at the high of 3120.

As the stock market trades at record highs interest rates have begun to drift lower with the 10 year treasury closing last week at 1.83% after trading in a range of 1.81% to 1.94%. We have seen this pattern occur many times over the last number of years–mostly certainly the bond markets isn’t in agreement about with the stock market party.

The Federal Reserve balance sheet grew by $8 billion last week. The non-QE, QE continues and I suppose we should all learn to accept that the global economy will need to be ‘juiced’ for the many years to come. Exactly what measures the central banks will use when we hit recessionary times isn’t known, but certainly they are shooting most of their ammo during times that are relatively decent (economically).

Last week 4 new income issues were announced and sold.

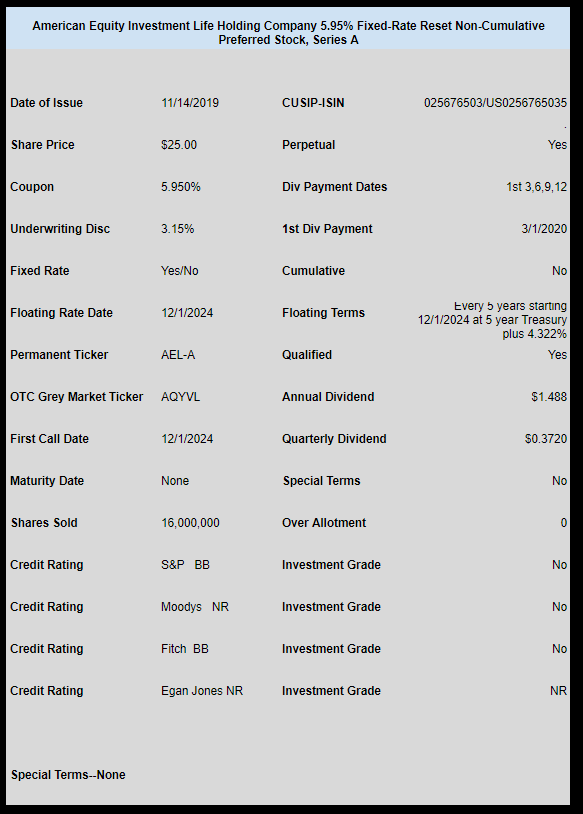

Annuity/insurance company American Equity Investment Holding Life (AEL) sold a new issue of non-cumulative Fixed-Rate Reset preferred. The issue will have a fixed rate until 12/1/2024 of 5.95%. At this time the coupon will be ‘reset’ at the sum of the 5 year treasury and a spread of 4.322%. This BB rated issue (junk) was greeted with very strong trading with a closing price on opening day of $25.50. The issue is trading on the OTC Grey market under temporary ticker AQYVL. Details of the issue can be found here.

Container ship owner Global Ship Lease (GSL) sold a new issue of junky baby bonds with a coupon of 8%. The issue will trade under the ticker of GLSD when it begins trading. Further details can be found here.

Regional bank BancorpSouth (BXS) sold a new issue of non cumulative preferred stock with a 5.50%. The issue is trading under the OTC Grey market temporary ticker of BCSBP. This junky issue is trading around $24.90/share. You can find further information here.

Lastly diversified manufacturer and distributor Compass Diversified Holdings (CODI) sold a new issue of fixed rate preferred with a juicy coupon of 7.87%. The issue is trading under the OTC temporary ticker symbol of CMPSP. Even a juicy coupon can’t lure buyers as the issue closed the week at $24.64. Almost without doubt the fact that CODI is a MLP which will mean a K-1 at tax time is not helpful to the market rebuke. Further info is here.

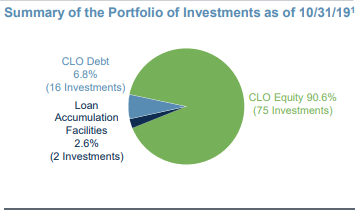

CLO (collateralized loan obligation) holder Eagle Point Credit Corporation (ECC) has released their monthly investment updated.

It is interesting that the price level of the common shares trades at a 45% premium to net asset value. ECC is trading around $14.40 while the net asset value is just above $10/share. Folks are obvious enamored by the 16% current yield. Of course if you held the common for a year or two you have a sizable negative total return–shares were at $21 2 years ago.

Of course we really don’t care too much about the commons shares–I don’t own them and never have owned any common shares.

We are interested in 2 term preferred that are outstanding as well as 2 baby bonds. The term preferreds have coupons of 7.75%, while the baby bonds have coupons of 6.6875% and 6.75%. All of these issues trade well with pricing between $25.70 and $26.50.

We are most interested–as an investor–or potential investor, 1st off in the asset coverage ratio–they must maintain a 200% or more asset coverage on their senior securities (debt and preferreds)–I currently calculate the ratio around 270%.

On the other hand we do care about the net asset value of the common shares–poor financials, over time can bleed into the baby bonds and preferred shares. The company showed a large unrealized gain of $38 million on holdings for the 6 months ending 6/30/2019. A year ago they showed a huge unrealized loss of $91 million. Of course virtually all of the assets are Level 3 (value can’t be directly observed)–the values are calculated by a 3rd party financial model. So you can expect plenty of volatility in net asset values.

ECC is a holder of primarily equity tranches of CLOs. The equity tranche represents almost 91% of the companies holdings. Potential investors always need to remember that the equity tranche represents the highest risk of the CLO.

I believe that as long as the economy is relatively strong (not in recession), the term preferreds and baby bonds present a risk/reward that might work for many folks. I have held a position in the past (term preferred and baby bonds) – and may again, but do not hold any at this moment.

Insurer/annuity company American Equity Investment Life (AEL) has priced the previously announced preferred issue.

The fixed-rate reset preferred will carry an initial 5.95% coupon until 12/1/2024. At this point it will reset to the 5 year treasury plus a spread of 4.322%. On each 5 year anniversary it will reset again.

The issue is rated BB (just below investment grade) by both S&P and Fitch.