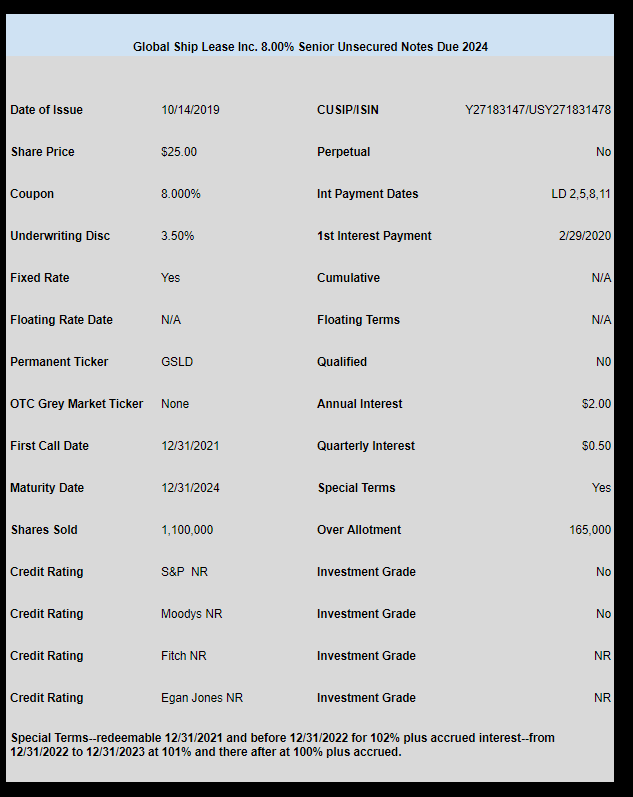

Container ship owner Global Ship Lease (GSL) has priced their previously announced $25 baby bonds.

The issue will carry a coupon of 8.00% and the issue will mature in 2024.

An interesting side note to this issue is that B Riley recently (10/01/2019) took a 11% position in the company and will be buying $2 million of this new issue.

Note the bonus rate for early redemption.

The pricing term sheet can be read here.