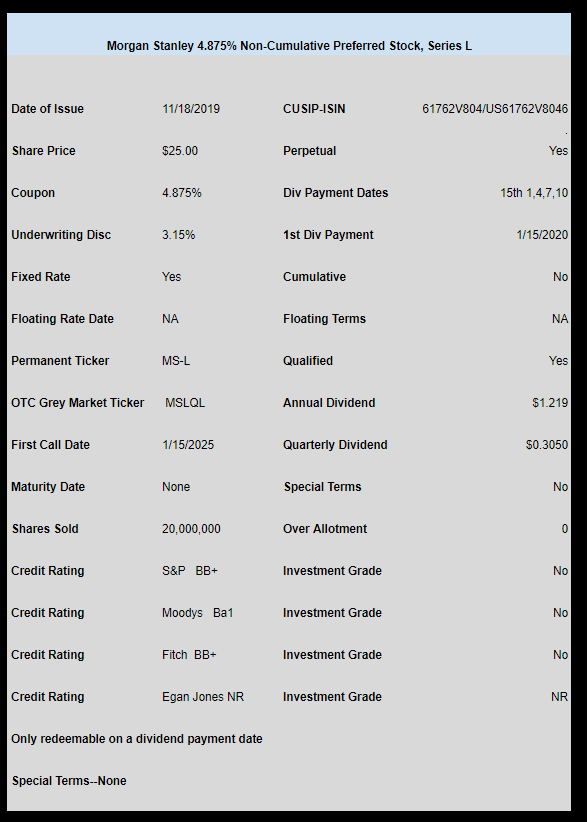

Morgan Stanley has priced their previously announced new fixed rate preferred.

The issue is non-cumulative, qualified, NON investment grade and 20 million shares priced at 4.875%.

With all the substandard coupons we have seen I should be used to being disappointed in these meager coupons–but I’m not!! If it was investment grade–then maybe 4.875% would be right–but they fall short of investment grade.

Oh well–it is what it is and my simple answer is –NO I won’t buy any.

The pricing term sheet is here.

Thanks SteveA for being on top of this one.