Franchise Group (FRG), an operator of franchised businesses, has announced a new offering of cumulative preferred stock.

The issue will be cumulative and qualified.

I am not familiar with this company, but it looks like they operate vitamin stores, sell furniture and has a tax preparation business. Obviously plenty of due diligence needs to be done on this issue.

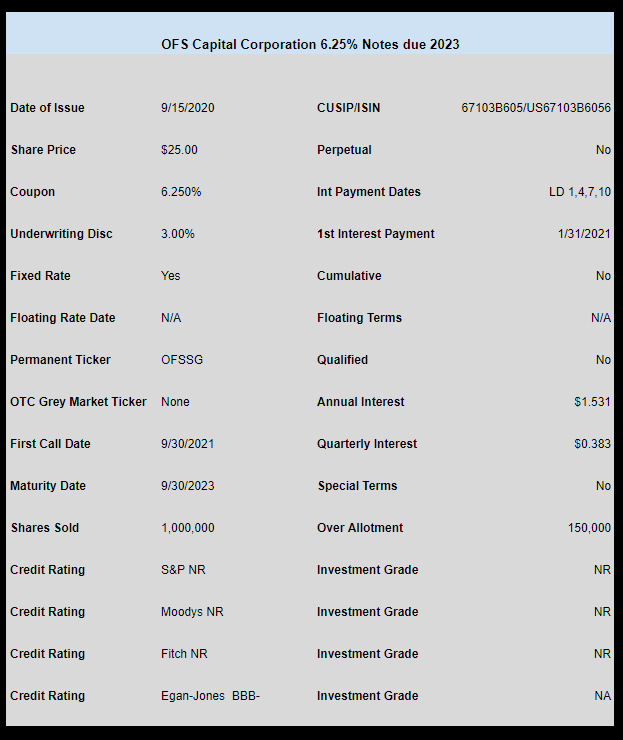

Business Development Company OFS Capital (OFS) has priced their new issue of baby bonds.

The issue priced at 6.25% which at first glance seems low–but the issue is just a 3 year issue, maturing in 2023 and shorter dated maturities price lower.

There will not be OTC grey market trading. The issue should begin trading in the next week or so.

Wesco International (WCC) which merged with Anixter International earlier his year is about to make their 1st dividend payment on the juicy 10.625% fixed rate reset cumulative preferred on the 30th of the month.

The WCC-A issue went ex-dividend today for around 73 cents–the first payment is for slightly over 3 months.

The company is a giant in the business to business distribution and supply chain business with revenue now in the $17 billion area.

You can be certain there is plenty of risk in Wesco as they are rate B1 by Moodys and BB- by Standard and Poors. You can read S&P’s take on the combined companies.

I only mention this issue because depending on your risk tolerance this may be a reasonable holding. The reset period isn’t until 6/22/2025 so at 10.625% there is plenty of ‘meat on the bone’ yet even though shares closed at $28.30 today.

Disclosure–I hold a position in this issue which I bought in the $26.90 area.

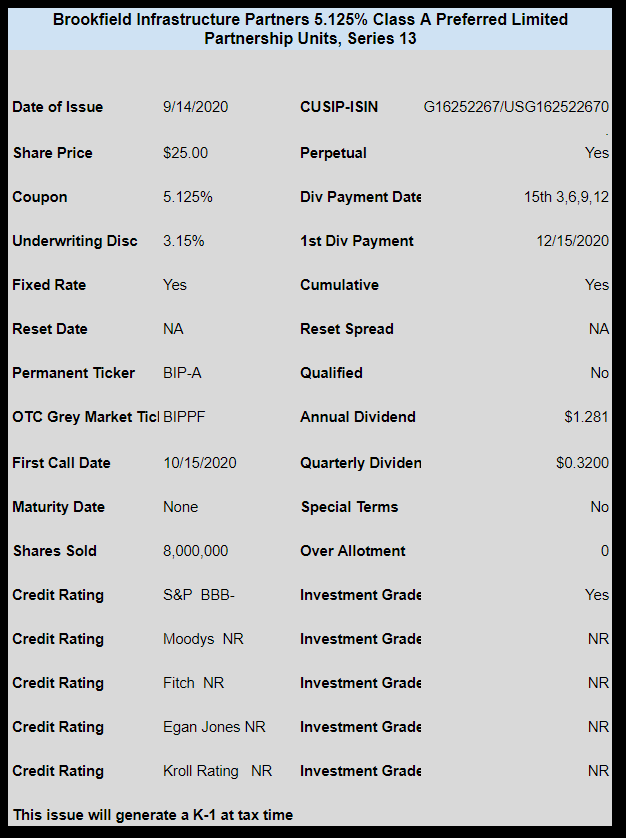

Canadian company Brookfield Infrastructure Partners (BIP) has announced a new issue of $25 preferred stock units (called units not stock if issued by a partnership).

This is a quality issue, but will come with a K-1 at tax time since it is a partnership.

BIP owns power generation, transportation assets, cell towers and other critical assets.

Business Development Company OFS Capital (OFS) will be selling a new issue of $25 notes.

The company already has 3 issues outstanding with coupons ranging from 5.95% to 6.50% and you can see them here. All issues are trading substantially under $25.

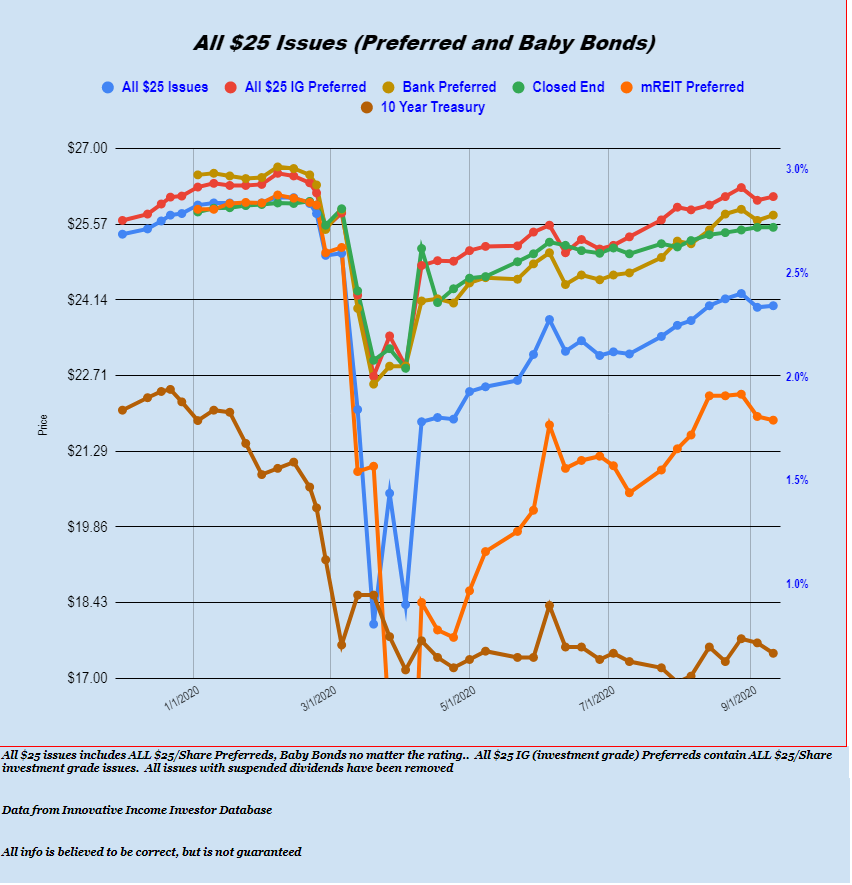

Trading in a range of 3310 to 3426 and closing at 3341 last week the Sp500 had a holiday shortened week loss of about 3%.

The 10 year treasury moved in a range of .66% to 72% and closed the week at .67%. Rates continue to hold fairly steady in spite of massive government borrowings–liquidity everywhere looking for a home. Plenty of bank liquidity and banks have had to do little to no repurchase agreements to garner cash.

The FED balance sheet fell by $7 billion last week–once again continuing the saw tooth pattern we have seen since early July.

The average $25 preferred stock and baby bond barely budged last week as the average issue was higher by 3 cents. No sector moved much–CEF preferreds were flat, utility issues fell 7 cents, banks were up a dime, investment grade issues were up 7 cents and the lodging REITs were up 15 cents.

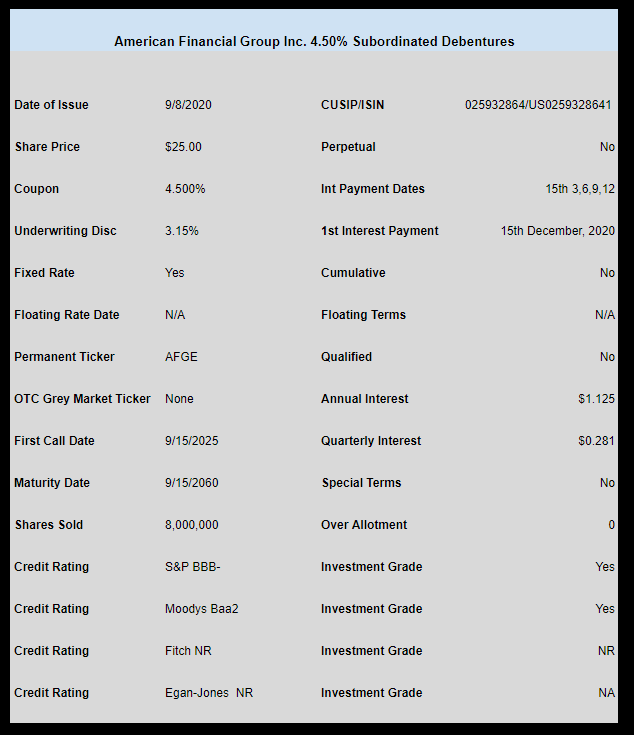

Last week we have 4 new income issues come to market.

American Financial Group (AFG) came to market with a 4.50% baby bond. We haven’t seen trading in this issue yet, although we would expect it this coming week.

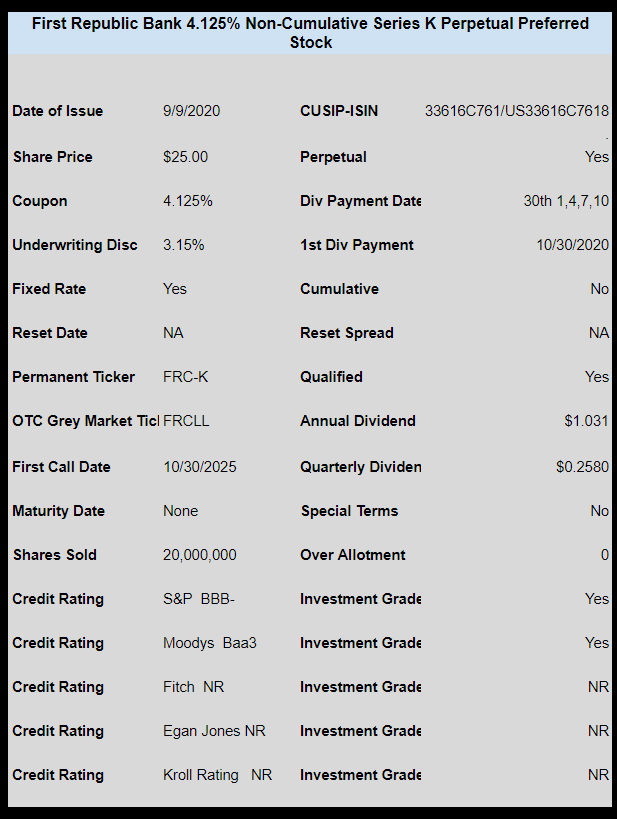

First Republic Bank (FRC) came to market with a 4.125% perpetual preferred issue. We see a OTC grey market closing trade at $25 on Friday–plenty of yield hungry folks even at 4.125%.

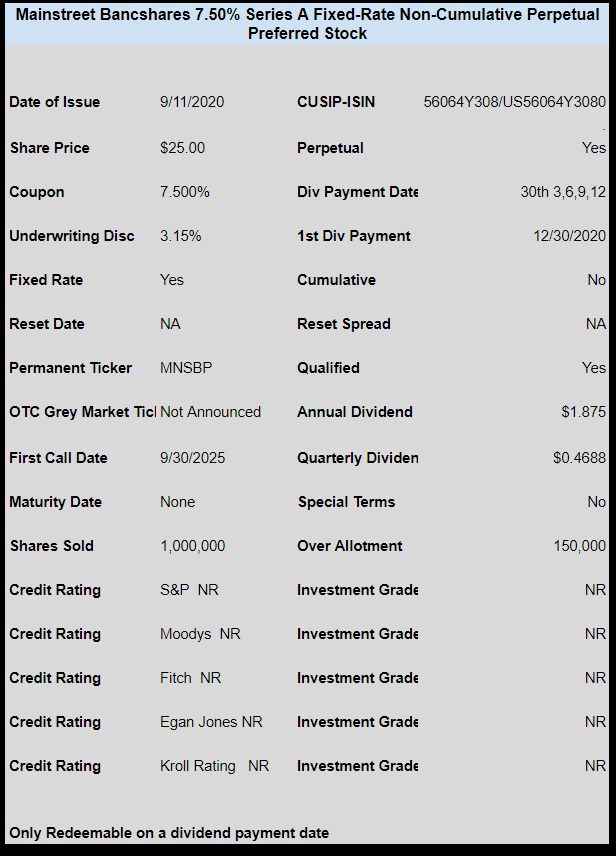

Small Virginia banker MainStreet Bancshares (MNSB) came to market with a 7.50% perpetual preferred. No OTC grey market ticker has been announced.

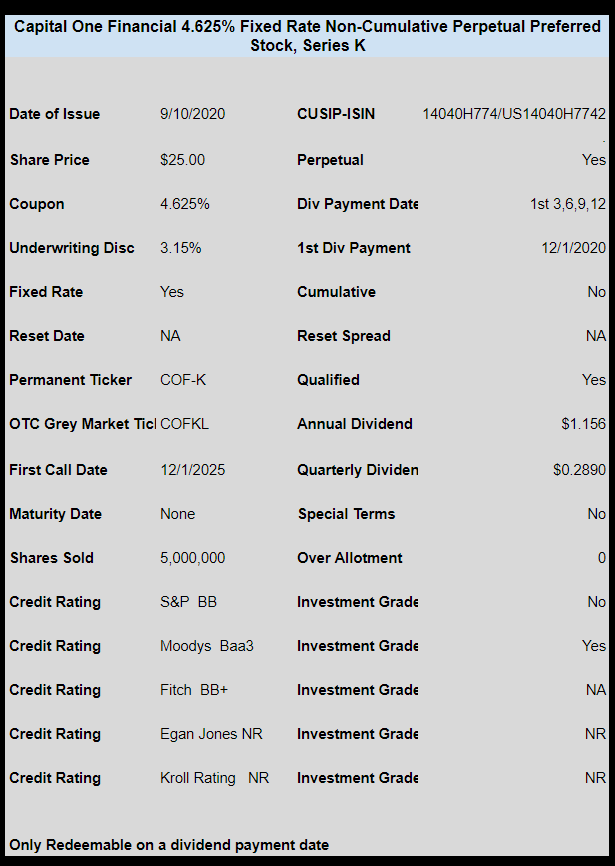

Lastly Capital One Financial (COF) sold a new 4.625% perpetual preferred issue. The issue is trading on the OTC grey marekt last trading at $24.67.

As predicted by some yesterday small Virginia community bank MainStreet Bancshares (MNSB) has priced their new preferred offering at 7.50%.

They are selling 1 million shares with an over allotment available of 150,000 shares.

The issue is non-cumulative and is not rated.

Make sure to understand the risk/reward with this issue–presently 22.5% of their loan portfolio is in ‘deferral’–so you can be fairly certain they will be taking large write downs in the near future.