I recapped my buy of the new Capital Southwest Corporation (CSWC) last week–now for my 2nd buy in this sector (BDCs).

I am buying a 1/2 position of the newer Saratoga Investment (SAR) 8.50% senior notes (SAZ). 5 years to maturity, although 2 years to 1st optional call so one doesn’t want to pay too much above $25 for the issue in case we see sharp rate drops next year.

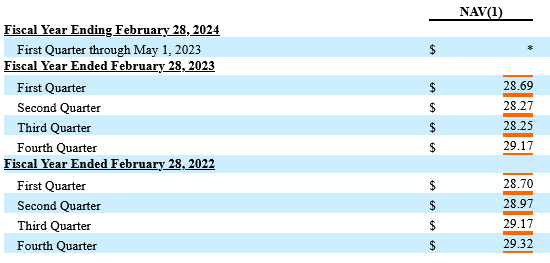

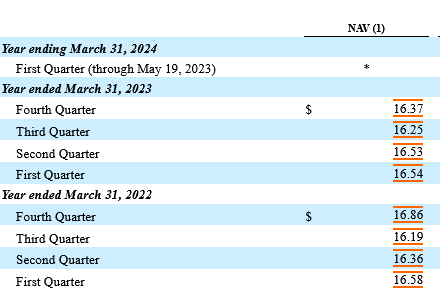

SAR is very similar to CSWC in many ways. They have assets under management of around $1 billion–so a decent sized business development company. Like CSWC they have maintained a relatively flat net asset value/share – always a good sign that they can maintain their NAV.

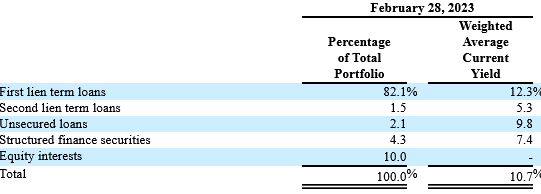

Also like CSWC the company invests primarily in 1st lien debt, although they do have 10% equity interests.

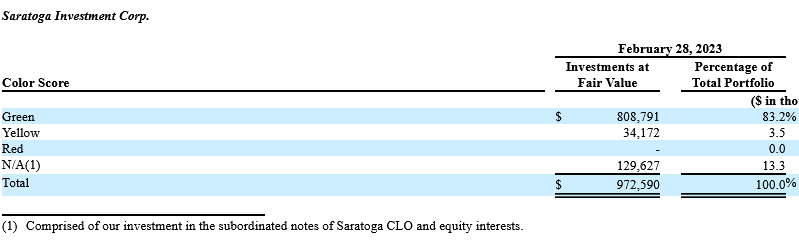

The company self grades their portfolio in colors green, yellow and red–obviously the red is the poorly performing issues of which the company claims to have none.

SAR has been around since 2007–while not as old as CSWC 16 years is ‘middle aged’ for a BDC and certainly they have seen the ups and downs in economic conditions in the U.S. In fact the company had issues in 2008 with a default on some debt–since then they have been straightened around and have performed very well in the last 10 years.

Last week we saw the S&P500 move in a range of 4304 to 4448 and closing on Friday near 4410—a gain on the week of over 2%. The 4448 high for the week is also a new 52 week high. On the surface one could call the equity markets overvalued, but with the massive amount of money resting in money market funds and other short term income vehicles there is plenty of ‘dry powder’ available to move values much higher.

The 10 year treasury closed the week at 3.77% after trading in a range of 3.68% to 3.85% on the week. Honestly a fairly tight range given the amount of news that occurred during the week. Both CPI and PPI were released and were approximately as expected. The FOMC ‘paused’ with rate hikes, but pretty much telegraphed more rate hikes to come–we’ll see as we watch what they do versus what they say.

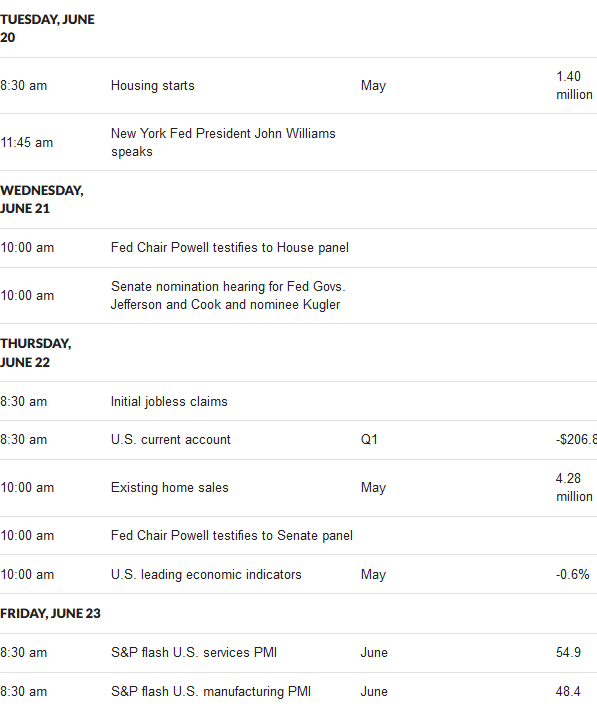

This weeks actual economic news is fairly sparse, but the big show will be the Fed chair testifying to congress – the house on Wednesday and the senate on Thursday. We will have the leading economic indicators on Thursday which will be closely watched. The LEI has sunk for 13 months in a row and has historically been a fairly reliable indicator of recessions–obviously, thus far in this cycle, we haven’t see a real recession.

The Federal Reserve balance sheet assets fell by $1 billion last week–the 2nd week in a row the balance sheet has been relatively flat. The constant reduction in assets will resume soon–quantitative tightening is still in place so the run off of the assets on maturity will tick up this week.

I am not publishing weekly prices of $25/share preferred shares and baby bonds. This is the 1st time since 1/3/2020 I have not published these values. Google quotes have been so bad over the course of the last week that I can’t come up with reliable numbers–hopefully things get corrected this week.

We did not have any new income issues priced last week, but the new issue 7.75% baby bonds from Capital Southwest Corp (CSWC) started trading and closed the week at $25,22.

NOTE–I just bought a 1/2 position for 24.94. If we get some slippage I will add to the position.

I have surveyed the Business Development Company (BDC) landscape and have come up with what I believe are the 2 best buys available for my level of risk tolerance.

1st I will be buying some of the new Capital Southwest Corp (CSWC) 7.75% baby bond (CSWCZ). Honestly this is one of the top BDCs available in my mind. The baby bonds were issued with a Baa3 rating from Moody’s (per June 7 ratings action)- this is very unusual – of course virtually no baby bonds from BDCs are rated. Ratings mean zip if the company is poorly managed–so I have scrutinized SEC reports.

Like most business development company’s CSWC is required to maintain a 150% asset coverage ratio–but they have a self imposed limit of 166% which is tighter than the official requirement.

CSWC has maintained a relatively flat share net asset value during the last 2 years–no small feat in these times of skyrocketing interest rates and indicates there have been very few write downs in the portfolio.

The investments made by CSWC are mostly 1st lien loans – I don’t want a BDC that have a portfolio full of 2nd lien stuff – that is worth zip to me – I want to be paid 1st.

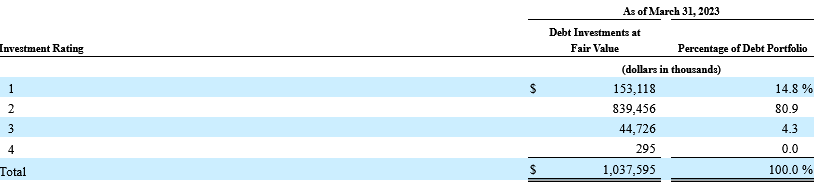

The portfolio is in the $1.3 billion dollar range (as of 3/31/2023)–a fairly large portfolio for a BDC. The debt portion of the portfolio has been self rated as shown below. 1 is performing ‘better than expected’–a 2 is ‘as expected’ 3 is ‘below expectations and 4 is ‘crap’. As of 3/31/23 .3% of the portfolio is on ‘non-accrual’.

CSWC was formed in 1961 and elected to become a BDC in 1988–so this one has been around quite a while.

As always this is not a recommendation to purchase this security and everyone should do their due diligence by reading the 10-K and by perusing the presentation and other pertinent data.

Below are press releases from companys with preferred stock and/or baby bonds outstanding–of just of general interest. With earnings season over news is more minimal.

The pause in rates was as I expected and the hawkish statement was also mostly as I expected. Although the hypocrisy of the statement – with numerous members expecting to see a need for further rate hikes, never ceases to amaze me.

For years these folks have made policy errors which were obvious – zero rates for years even when inflation started to roar – and now they (some members) think they have the ability to foresee the future – where did data dependency go?

My worry with the super hawkish statement is how many more banks will be seized – of course I am ‘talking my book’ since I own numerous banks without current financial information as to how they are performing which turns things into something of a crap shoot – I guess that is the ‘risk/reward’ and all of us know full well that there is plenty of risk in most banking issues. I had already pulled away from buying more bankers and this certainly will temper my desire to own incremental shares.

Well actually ‘day of reckoning’ is probably overstating the long term importance of today. Sure it matters whether the FOMC raises the fed funds rate–but whether it is raised or paused life will go on tomorrow. With the CPI being reported yesterday at or slightly below forecast no doubt the FOMC has cover to pause rate hikes which is what I think they will do–of course they could move rates up by 1/8%–there is no rule movements have to be in increments of 1/4%.

So we will see the producer price index in a few minutes–not likely to surprise or be a factor in today’s interest rate decision. Through the rest of the week the economic news is fairly minor – to me the most important news will be 1st time unemployment claims tomorrow–employment will determine where we are going – over time – with this economy.

No action in my portfolio yesterday – my portfolio just drifted no real gains or losses – with a bunch of CDs, treasuries and money markets portfolios move very modestly.

Below are press releases from companys with preferred stock and/or baby bonds outstanding–of just of general interest. With earnings season over news is more minimal.

So we have the FOMC meeting starting in a few hours, but leading on to the meeting we will have the consumer price index (CPI) released in less than an hour–the final piece to the puzzle before a interest rate hike/pause. Likely only a massive surprise (either higher or lower) will make a difference in the rate hike decision – as I have mentioned I think that the FOMC really wants to raise rates – but likely will pause. We’ll know in about 30 hours.

Markets are fairly quiet today with equities barely moving–although yesterday the S&P500 index was up about 1% – if you were to believe the pundits these markets are pretty darned overvalued and we could see a might tumble soon. Well no one knows for sure and I don’t fixate on that possibility – just like the coming ‘recession’ which never seems to arrive trying to forecast the macro movements is a fools errand and only causes one to cower in the corner and not act.

Once again I did nothing at all yesterday – no buying or selling. I am thinking that I have most of the banking issues I want/need and need to move onto a new sector. Some have suggested business development companys (BDCs) and it looks to me like that sector does hold some great opportunity–in the baby bonds not the common shares. I will be honing in on a few shares soon–without a doubt I will buy the new Capital Southwest Corp (CSWC) 7.75% baby bond when it becomes available.