The Standard and Poors 500 moved in a range of 3091 to 3127, about a 1% range, before closing the week at 3110–around a 1/2% loss for the week.

Interest rates, as measured by the 10 year treasury, stayed pretty tame last week, moving in a range of 1.73% to 1.85 before closing the week at 1.77%.

The Fed balance sheet actually fell last week by $17 billion–this is the first fall in the balance sheet since 8/28/2019.

Last week we had the following new income issues announced.

Morgan Stanley (MS) announced a new preferred stock with a coupon of 4.875%. The issue is trading under OTC Ticker MSLQL and last traded at $24.98. Further details are here.

QVC Inc. sold a new issue of baby bonds that while investment grade rated carry a coupon of 6.25%. The issue will trade under ticker QVCC, but it is not yet trading on public exchanges. Further details are here.

Insurance company AXA Equitable (EQH) sold a new perpetual preferred with a coupon of 5.25%–not toop bad for a split rate investment grade issue. The shares are trading on the OTC Grey market under ticker AXQEL and last traded at $24.85. Further details are here.

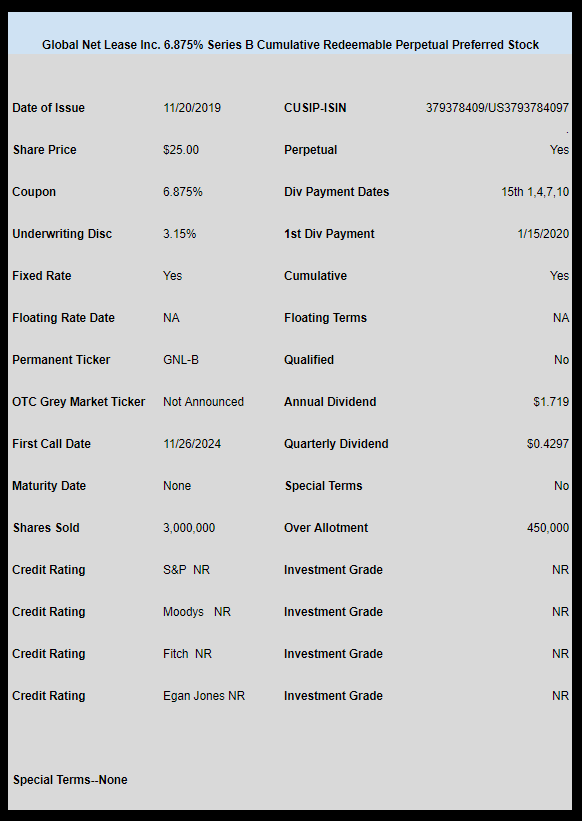

REIT Global Net Lease (GNL) sold a new preferred with a 6.875% coupon. This is an unrated issue which is now trading under the OTC Grey market ticker of GBLNP–last trading at $24.64. Further details can be found here.

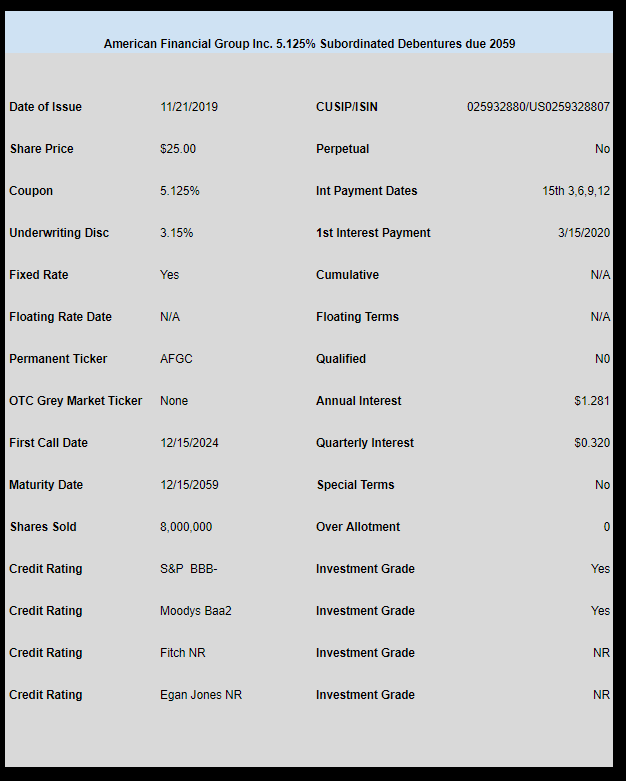

Insurer American Financial Group (AFG) priced an investment grade baby bond with a coupon of 5.125%. There is no OTC Grey market trading in the issue, but the issue will trade soon on the NYSE under ticker AFGC. Further details are here.

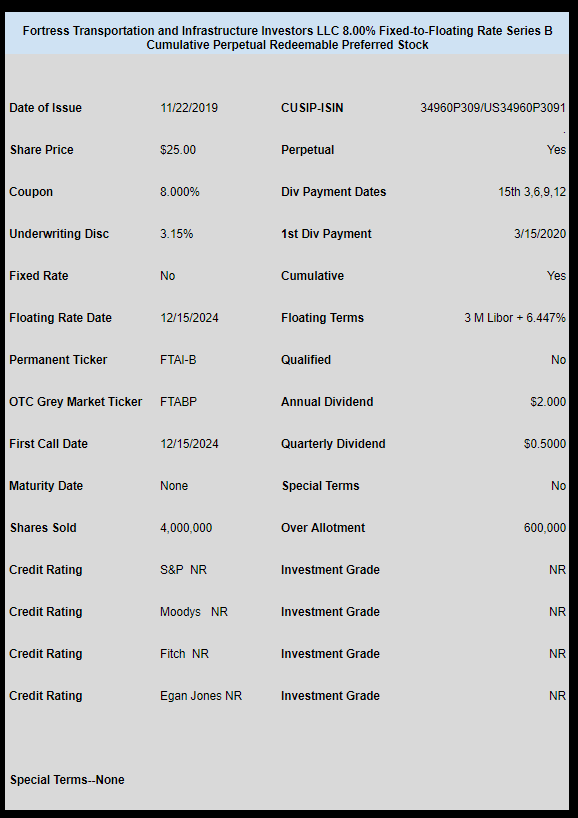

Lastly partnership Fortress Transportation and Infrastructure (FTAI) sold a fixed to floating rate preferred with an initial coupon of 8%. Being a partnership the shares will bring a K-1 at tax time and the issue, while cumulative, will not be a qualified distribution. Shares will trade today (Monday) on the OTC Grey market under ticker FTABP. Further details can be seen here.