It is always amazing how poorly these shipping companies are operated—or maybe it is just amazing that supposedly educated lenders will lend them money knowing odds are high that they will never get their cash back.

Dynagas LNG Partners (DLNG) is one of those shippers that one would think had an opportunity to make a decent profit–they are a small partnership–revenue in the $135 million/annually area. They have only 6 LNG carriers and their sponsor has been in business since 2004. 5 of the 6 LNG ships are ice rated–they can travel the northern seas–up near the Artic circle–in fact their sponsor was the 1st LNG carrier to do so back in 2012.

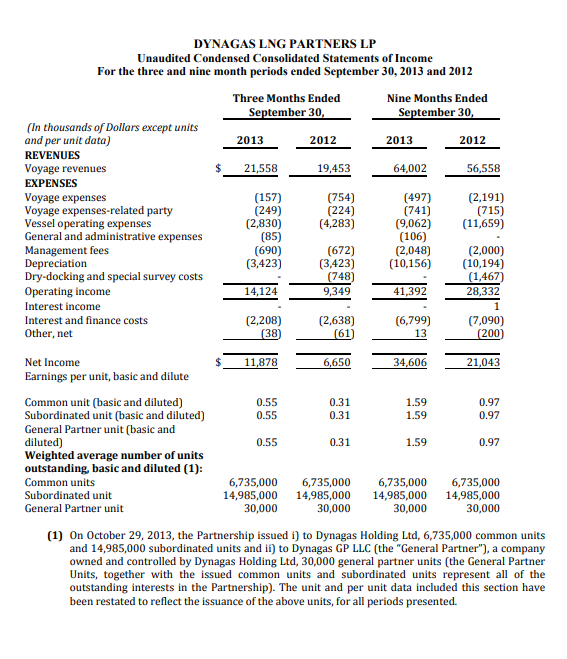

DLNG was formed in 2013 with an IPO in the 4th quarter. Reviewing the financials for the 9 months prior to the IPO we see a company with stellar numbers–in fact I can clearly remember reviewing these financials and thinking “maybe these LNG carriers have some real potential”. Take a look at the results for 3 months and 9 months ending 9/30/2013. The partnership operated only 3 ships at this time and they were contracted at $76,000/day each. This shows a net income of $1.59/share for 9 months.

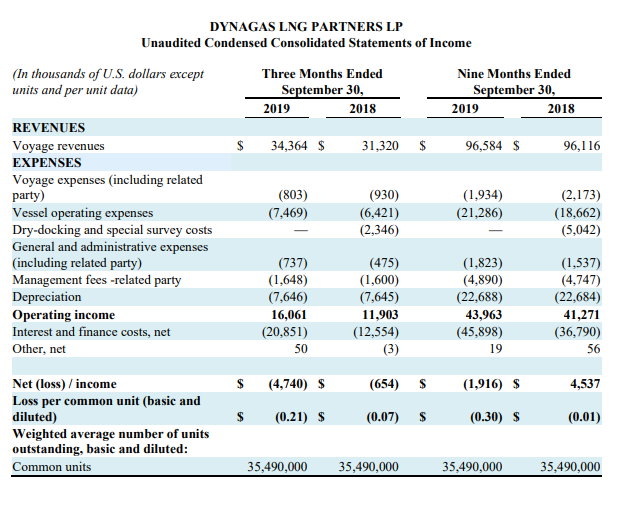

Speed ahead to 2019–the company operates 6 LNG carriers now instead of 3. Below is their recently released earnings statement. They are contracted at an average daily rate of $62,000—and they can’t even bring a single damned cent to the bottom line!!

One can look at these income statements and clearly see that while revenue is up 50% in 6 years, interest expense is up 400%–easy money and stupid lenders. But I am sure the sponsor of the partnership is happy – they get their management fees year end and year out irrespective of their incompetence.

Of course there is much more to the story–I’m am sure the sponsors screwed the partnership on ‘drop down’ assets–financed with easy money–but the point really is–BE DARNED CAREFUL WITH THE 2 OUTSTANDING DYNAGAS LNG PARTNERS PREFERRED SHARES–which can be seen here. The shares had big jumps when the company was able to refinance their debt–so instead of a instant bankruptcy they will now go into ‘slow motion’ bankruptcy.

The company has now been restricted from paying any further common share distributions while their new loan is outstanding–BUT the next available source of funds will be the preferred dividends. The company has only a bit of cash, but no doubt they will survive for a few years (the cash you see on the balance sheet 9/30/2019 is already restricted for debt repayment)–lenders will be forced to keep them afloat for a while. Honestly there is a 50/50 chance they will be liquidated within 5 years and common and preferred holders will get ZIP.

For all practical purposes this is now a Zombie company.

Here is their earnings release.