As many of you have noticed many of the baby bond stock quotes in spreadsheets went off last Friday and haven’t been back since that time.

Of course over the 14 years I have published websites this has been a persistent issue as Google doesn’t supply many baby bond quotes and Yahoo Finance cut us out maybe 3 years ago.

I am looking for alternatives, but thus far have not found a suitable alternative–I am about to the point where I am going to contract with a ‘real’ quote supplier for the quotes–we’ll see.

The issue was trading at $25.76 last Friday so there will be small losses on the call for some–the issue goes ex dividend today for about 34 cents and there will be a small stub payment on redemption.

Last week we saw a rare drop in equity prices as the SP500 fell by just a bit less than 1% on the week. The index traded in a range of 3633 to 3712 before closing at 3653.

It looks like for the coming weeks the release of the Covid-19 vaccine will drive the start of the week as equity futures are up by around 1/2% at 8 pm central time. Conversely any problem that arises with the vaccine plan could send the market tumbling. Any tumble should be shallow and short living.

The 10 year treasury yield fell back by 7 basis points last week closing the week at about .89% after hitting a high during the week of .96%. Treasury auctions last week came off very strong with high demand–a continuation of global liquidity sopping up all levels of note and bond supply.

The Federal Reserve balance sheet grew by $20 billion last week-as expected (at least the growth was expected–the amount is always anyone’s guess).

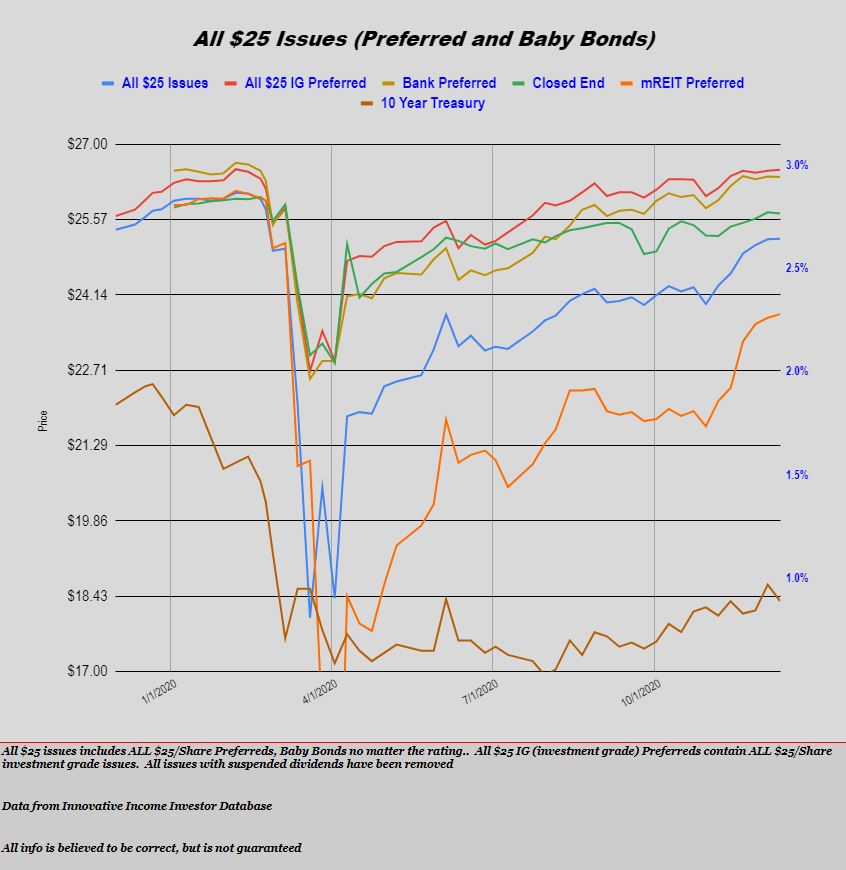

Last week the price of the average $25/share preferred or baby bond rose by just a penny. Investment grade rose by 2 cents, mREITs by 2 cents and CEF preferreds were off 1 penny. Not much movement at all.

There were 2 new income issues priced last week.

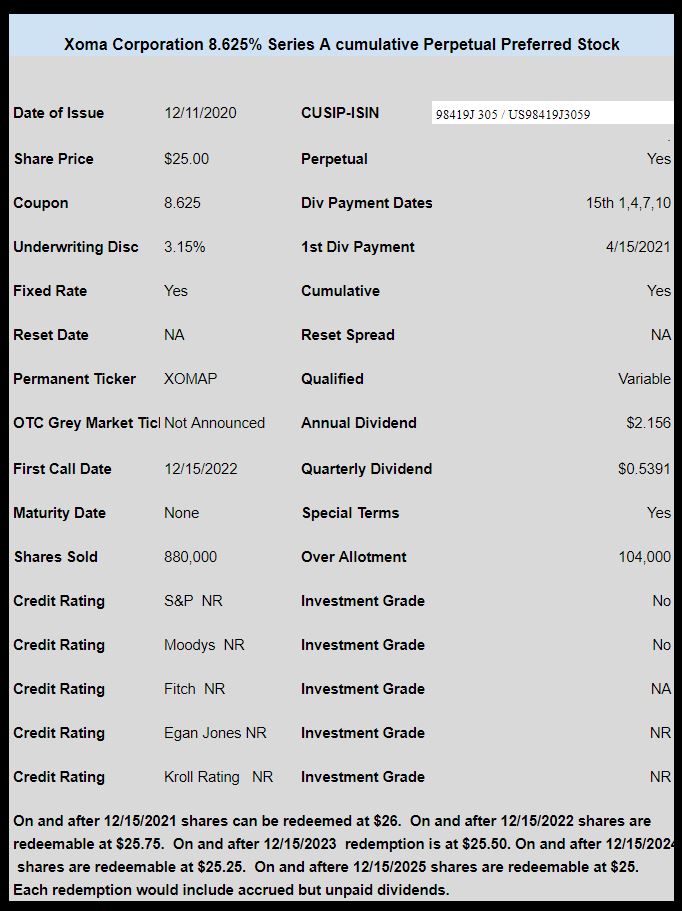

Biotech asset holder XOMA Corporation (XOMO) sold a cumulative preferred with a coupon of 8.625%–obviously plenty of risk with this one. I see no OTC grey market ticker.

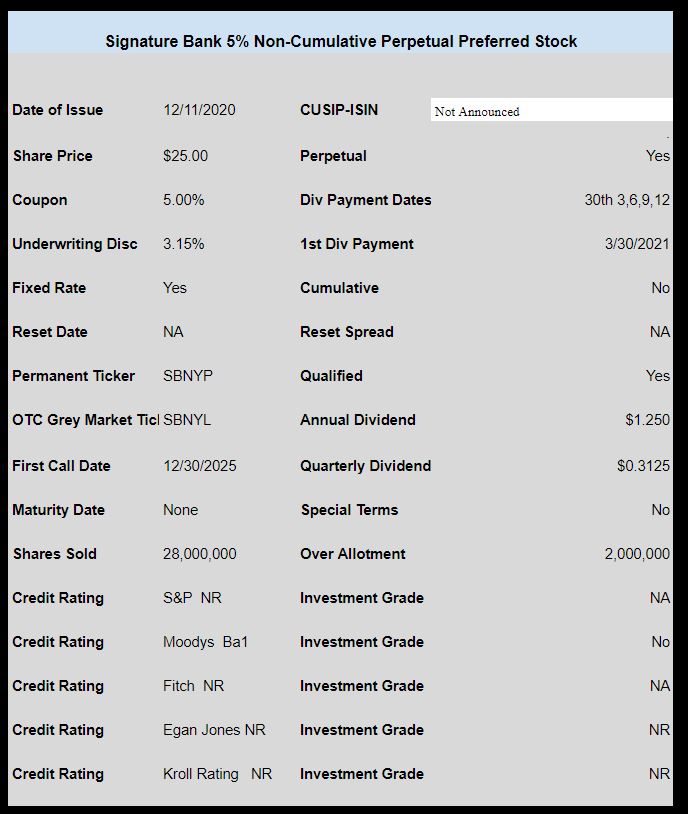

New York banker Signature Bank (SBNY) sold a new non cumulative preferred with a coupon of 5%. They have sold 28 million shares with another 2 million available in over allotment.

The issue is rated Ba1 by Moodys (below investment grade).

The ‘official’ pricing document has not been filed so information is incomplete.

The issue began trading on Friday under the OTC ticker SBNYL and closed at $24.86.

Almost 3 years ago the small company 1347 Property Insurance (PIH) sold a small issue of preferred stock. The issue carries a 8% coupon and of course is not rated. It is one of the few insurance company issues that is cumulative.

Below you can see the chart of the pricing since about 1.5 – 2 years ago. Honestly for the junk that it is trading has been strong.

Now I will just tell you now that the company is headed for the “trash heap” and holders of the preferred don’t seem to know that while they will receive a few more dividends it is likely they will see very little of their investment in a few more quarters–up in smoke–oh well I hope none of you are holding this issue. If the shares were trading at $5/share maybe it would be a good speculative–but that might be too high.

Now let’s turn to the reality of this issue–more specifically the company itself.

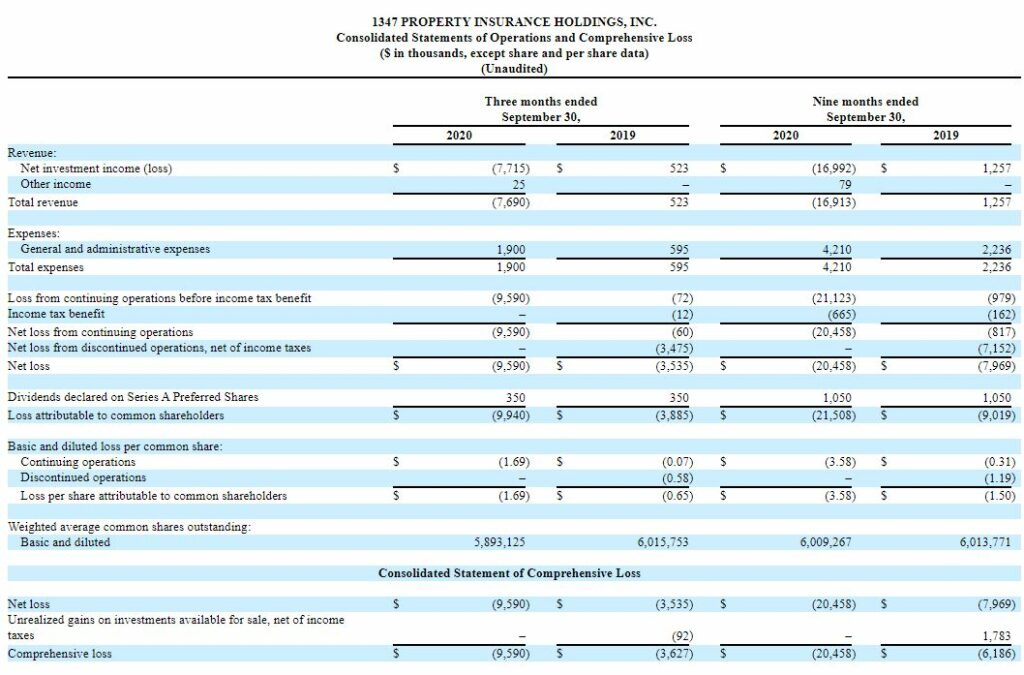

Here is the balance sheet for the quarter ending 9/30/2020. Note that the total assets have fallen by darned near 50% year over year. The cash hoard has fallen by near 50%. Sorry the data is small and hard to read. The SEC document is here.

Now let’s look at the income statement.

As you can see they have a loss of $20 million on the 9 months and a loss of almost $10 million during the most recent quarter.

Back in 2019 they sold a good deal of the business for cash and securities in buying company (FedNat). The buyer writes high risk homeowners policies in Florida and other gulf states–this is wonderful when there are no storms–but with all the storms the company has been hammered hard.

Xoma Corp (XOMA) has priced the previously announced new preferred stock issue. The issue prices at 8.625%.

The issue is unrated, cumulative and likely mostly unqualified. Qualified dividends can only be paid by corporations which have income–and generally this is not the case with XOMA. Dividends would instead by ‘return of capital’.

Note that the issue carries ‘bonus’ redemption prices.

We all have a different level of risk we are willing to take to garner some portfolio income and I have tried hard to push myself to buy some riskier assets. I still have plenty of dry powder–which I want to maintain at a healthy level, but I need to see some dividends and income flowing, or at least more–those $200-$500 payments hitting the account help motivate me.

Last week I wrote a bit about Oxford Lane (OXLC) and Eagle Point (ECC) issues I have bought—and folks chimed in with other suggestions.

Earlier this week I bought some of the term preferred shares issued by CLO owner Priority Income Fund (not traded). This collateralized loan obligation owner (organized as a closed end fund) is controlled by the hated (at least by many) business development company Prospect Capital (PSEC).

Priority Income Fund has 6 term preferred issues outstanding. The company became a ‘serial’ issuer of shares starting in 2018 and continued to sell new issues right through 2/2020. When the pandemic hit the company had registered to sell a another new issue, but it never happened.

Of the 6 issues outstanding only one is currently redeemable and 3 more issues will become redeemable in 2021—all but 1 issue trades under $25/share so they carry little to no call risk.

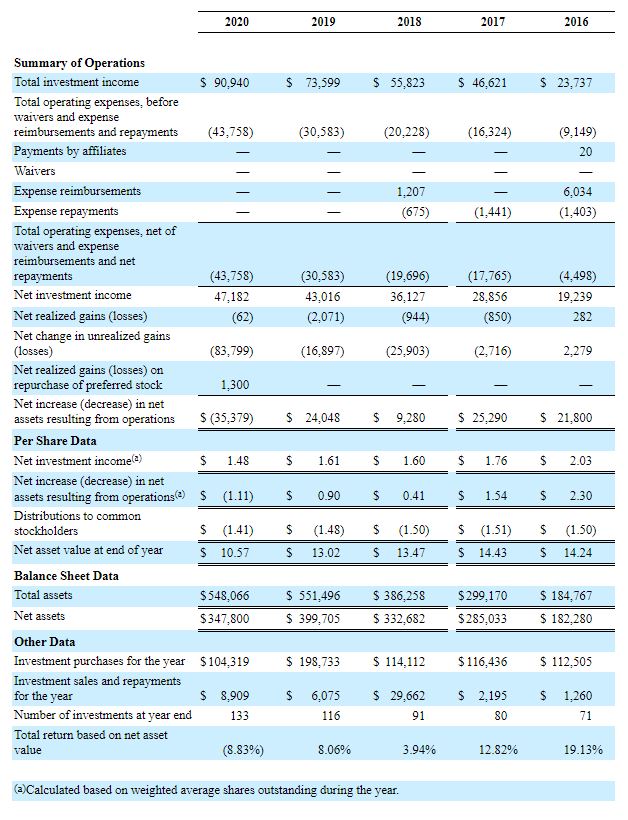

Below you can see a financial summary for the fund as of 6/30 for the last number of years. Really huge investment income, but pretty high expenses. High payouts to common holders with a slowly decaying net asset value (NAV)–on a per share basis. Generally the company pays out most of their investment income irrespective of unrealized losses.

Just remember with these closed end funds we care about the total asset value in dollars–not per common share. Funds like Priority Income Fund are always selling more common shares and below you can see that while the per share NAV is eroding the total assets continue to rise–at least until this year. The total asset value is what is used to provide our coverage ratio–closed end funds must have at least 200% coverage on the senior securities (i.e. preferred shares).

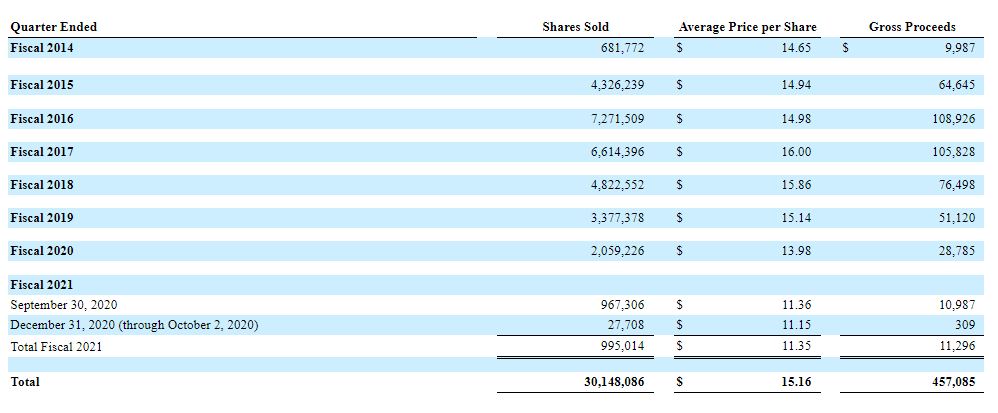

Below are the common shares the fund has sold over the last many years. These funds help keep the leverage ratio up–even if the common per share amount is falling.

As long as the total assets remain flattish I will feel comfortable holding some of the preferred shares assuming this economy doesn’t crash lower again. If the economy softens dramatically I will have to re-evaluate this one.

Xoma Corporation (XOMA) has announced they will be selling a new issue of cumulative, perpetual preferred stock.

Xoma appears to be a company that helps fund other biotech companies in exchange for a future royalty–honestly I don’t know anything about them, but I will be doing more research to help understand the company.

While it appears the coupon will be pretty high everyone should do some deep due diligence if you know as little as I do about Xoma.