Charles Schwab (SCHW) has just announced they will be selling a new preferred offering. While the company doesn’t list the redemption of the SCHW-C as a ‘use of proceeds’ I think there is a high likelihood they will call this 6% issue as it became redeemable on 12/1.

Business Development Company Gladstone Capital (GLAD) will be selling an issue of $1,000 notes.

Unfortunately the company will be calling all or a portion of the $25/share 6.125% GLADD notes due in 2023. The early redemption period for these notes started on 11/1/2020.

So another decent issue ‘bites the dust’. GLADD is trading at $25.33 right now so there will be no loss on the call.

Here we go on a another week which will be driven by news on Covid 19, vaccines and the never ending saga of the next ‘stimulus’ package.

The S&P500 traded in a range of 3594 to 3699 closing the week right at the high of 3699—a gain on the week of around 2%. For the coming week it is likely equity markets remain flat to 2% higher again–only a ‘spike’ in the 10 year treasury above 1% or maybe a ‘problem’ with initial vaccinations in England of the Pfizer Covid vaccine could put a major dent into equities.

The 10 year treasury closed last week at .97%. This was a 9 basis points move higher on the week. Income securities have paid little attention to higher rates thus far—rates don’t matter much until they do and no one knows where the point of ‘mattering’ is at–certainly something over 1%.

The Federal Reserve balance sheet rose by $6 billion last week–simply a stair stepping higher as has virtually been the case all year long. The upward curve on balance sheet assets will really steepen when a new stimulus package is launched.

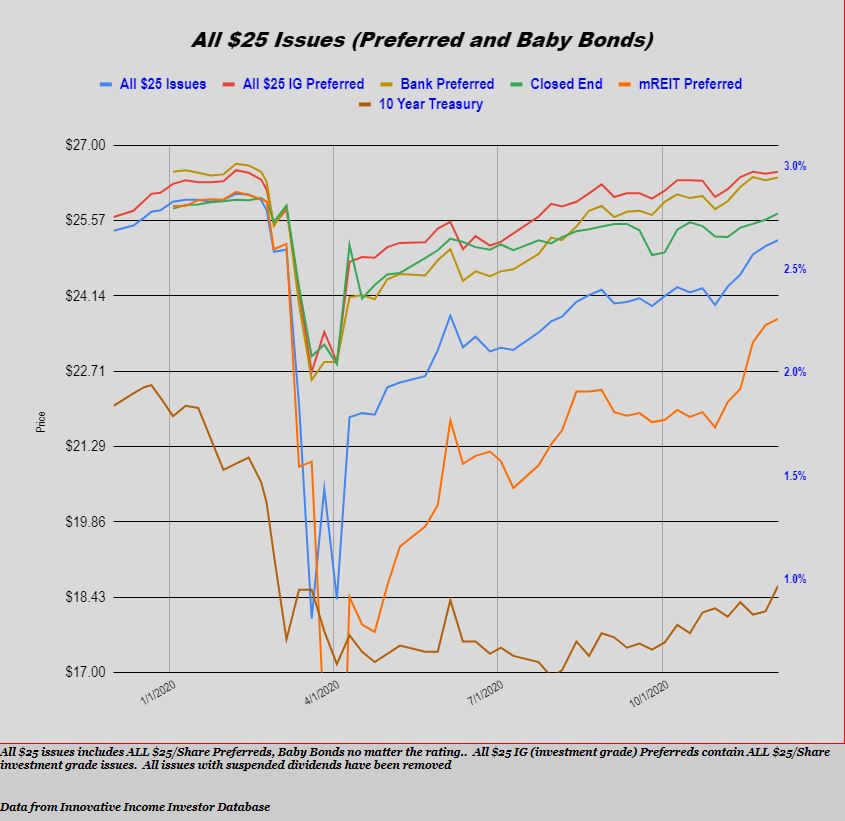

$25/share preferred stock and baby bonds have been following the lead of common stocks most weeks and last week was no exception as the average share moved higher by 11 cents–almost 1/2%. This move in the face of rising interest rates.

Last week we had 2 new income issues priced.

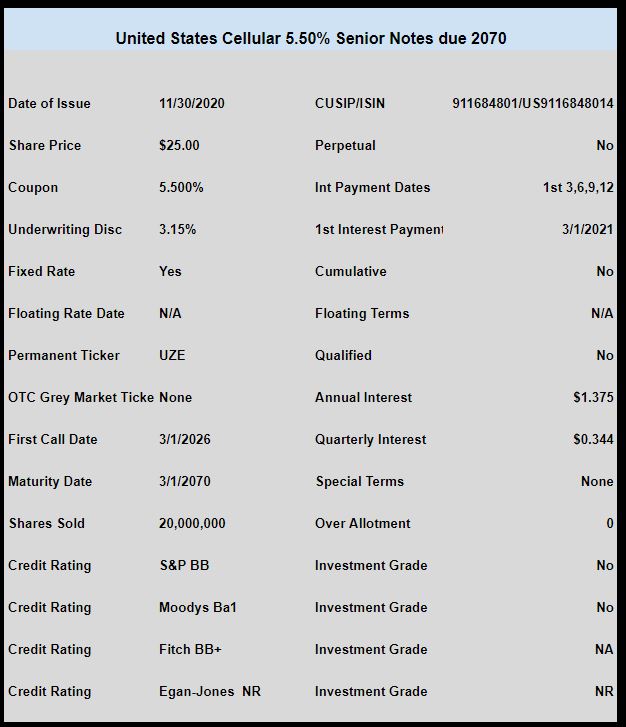

1st off we had a new baby bond issue sold by United States Cellular (USM) with a coupon of 5.50%. The issue has not traded as of Friday–but I would expect it anytime now.

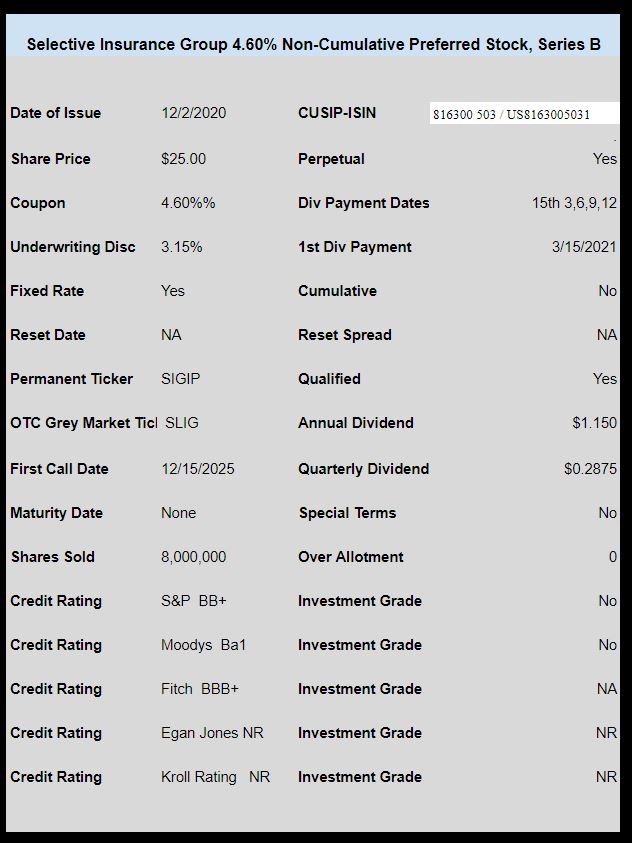

Then we had Selective Insurance Group (SIGI) sell a 4.60% non-cumulative preferred which has begun trading under OTC temporary ticker SLIG and closed last week at $25.80. This issue has traded strongly since the minute the 1st exchange trade took place.

Well it isn’t really too much of a wild side walk but I have started to buy some preferred issues that I haven’t owned for a few years–still in my comfort zone, but dicier than owning utility and CEF preferreds and baby bonds.

As most of you know these closed end funds invest entirely in CLO’s–collateralized debt obligations. These are not investments I really want to get into heavily, but it is all above risk and reward—and we all realize the reward has gotten pretty meager in investment grade issues—so here I am into higher risk issues.

It is my plan to simply hold these–in very limited quantity (a few hundred shares each) simply to help goose my dividends a bit. Given that they are term preferreds pricing should remain fairly flat until the next ‘tantrum’ or event and only God knows when this will happen.

The key with these issues is to watch the leverage–being organized as closed end funds they must maintain a 200% coverage ratio–this gives the senior security holders (preferreds and debt) some level of protection.

One thing to keep in mind with CHS is that the ag economy has improved drastically in the last 6 months. Commodity prices have risen 20-30% and farmers are in the black once again. It would seem logical that the ag end of the CHS business should improve dramatically in the quarters ahead. Recall that the company has been ‘carried’ by their refinery business for a few years now so some balance to net income would be a welcome development.

In one of the biggest disappointments of the year Selective Insurance (SIGI) has priced their new non cumulative preferred issue.

The issue is rated Ba1 (below investment grade) by Moody’s and has priced with a coupon of 4.60%—-yes 4.60%!! To say I am disappointed in this pricing would be a understatement–while we all knew it would be low–maybe 5.25%—but 4.60%. I had planned to buy a position tomorrow–but it would have to trade very weak for me to be interested.

Insurance company Selective Insurance (SIGI) will be selling a new issue of preferred stock.

It has been quite a while since SIGI has had an outstanding baby bond or preferred stock–they had a baby bond redeemed on 3/26/2019 and nothing since then.

I am not seeing new ratings on this issue, but I believe it will be a notch or so below investment grade.

The issue will be non cumulative, qualified and will have the normal optional redemption date in about 5 years–12/15/2025.

The permanent ticker will be SIGIP–it should trade on the OTC Grey market tomorrow, but the ticker is yet unknown.