Looking at the equity futures this morning it looks like we are in for more ‘paint drying’ trading–and honestly if that continues I am fine with that. Unfortunately it won’t continue – it will break hard in the next 10 days if the debt ceiling stalemate continues.

Interest rates are moving up a bit this morning – we are at 3.74% on the 10 year treasury. This means mortgage rates are moving higher once again. I saw a Zillow article yesterday that values in some of the most heated housing markets (i.e. Boise and Austin) have dropped sharply. It happens (drops) on a regular basis – prices are driven up and of course they are going to correct–most are not dropping like Boise, which is off near 20%, but they are not rising. If interest rates remain high and we finally have the long awaited recession we will see a housing bloodbath.

I see the Philly Fed non manufacturing index was just released at down 16–these smaller report while not market moving help to point to a FOMC rate pause in June–of course lots and lots of data yet to come in prior to the meeting (June 13-14).

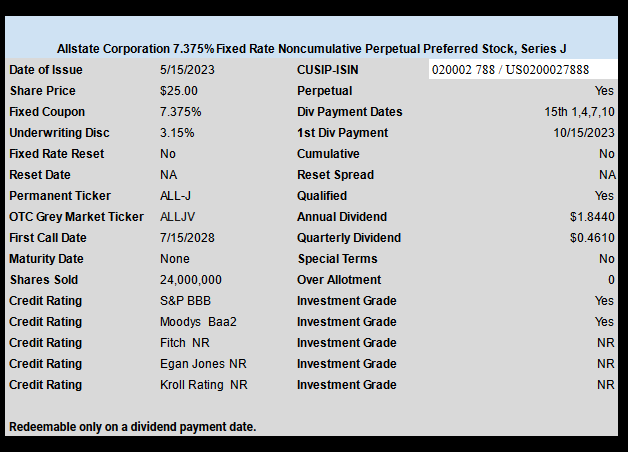

I note that Fitch downgraded Allstate (ALL) yesterday and rated the new 7.375% preferred (ALL-J) at BB+, which is a notch below investment grade. Given the hammering that insurance company’s have have taken in their investments and very high claims experience in their property and casualty businesses this is not a real surprise. But we all know how this works in insurance – a bad year means rates are jacked up and never come down again which creates giant profits down the road.

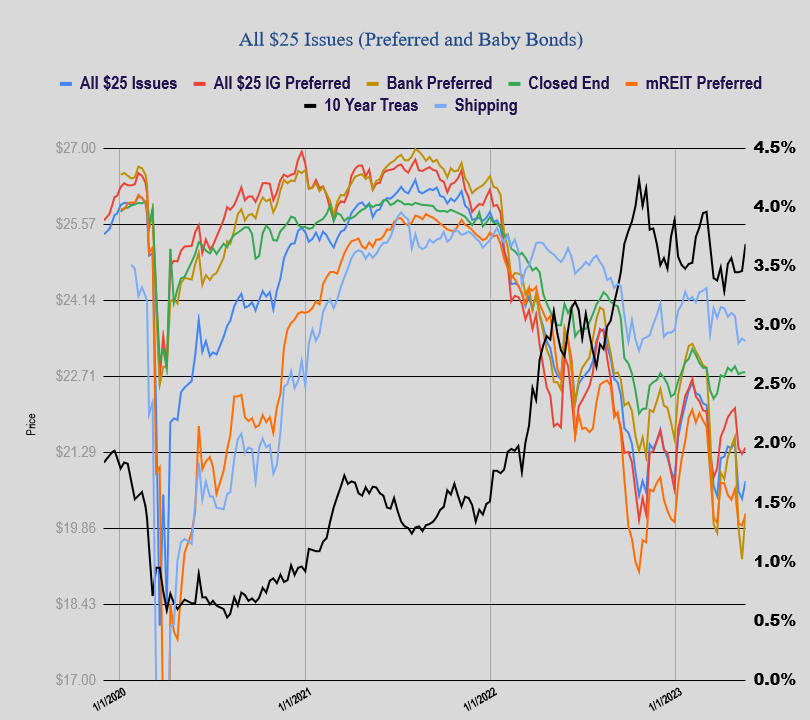

Banking preferreds were strong yesterday – we are near a point when one is going to have to buy if they want ‘bargains’–but there is risk obviously. I’ll be looking and nibbling this week. I hold no full positions in any banking issue–not even ½ positions. I own numerous issues in small quantities so will just nibble some more adding to the issues I own. If you want to lock down 8% current yields you have to expose yourself to risk – there is no way to get around it.