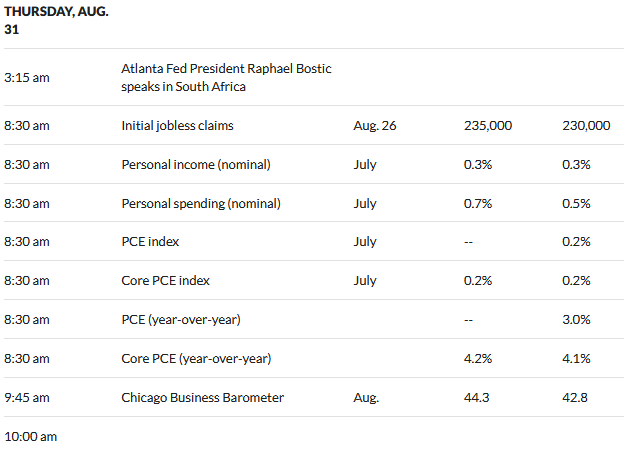

Every one is awaiting the release of the personal consumption expenditure (PCE) report–markets must be anticipating good news as the S&P500 is up 1/4% and the 10 year treasury is trading at 4.09%.

Of course we have the weekly initial jobless claims which has become more and more important as we track employment, which I believe is 1 of a handful of ‘most important’ indicators for the FED and the FOMC committee in interest rate decisions.

Personally I have had 3 good til cancelled buy orders execute in the last week–plus I have purchased a 5.6% 1 year CD (which of course is callable). None of the baby bond purchases were of any magnitude – actually they were all in the same security at lower and lower prices. I intend to get a ‘blurb’ out today or tomorrow outlining those small purchases and the logic behind them.

I continue to have multiple good til cancelled buy orders out there, but they will need the help of ‘nervous nellies’ selling to me at what I consider a bargain price. I have not sold anything recently but once again am considering lightening up on a few small bankers now that they have popped up from the recently sell-off–I have couple with 10% gains (capital gains plus 1 or 2 dividends) and may sell part of those positions–we’ll see.

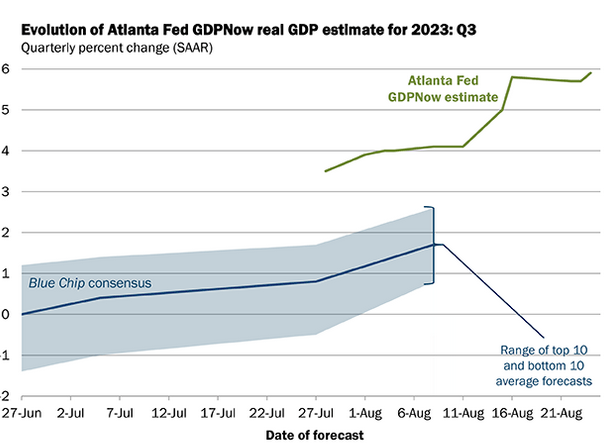

Have you noticed? I suspect most our readers are well aware that the Atlanta Fed model for GDP on 8/24/2023 shows growth predicted at 5.9% annually. If this is anywhere close we are going to have a lot of trouble getting interest rates much (if any) lower. Personally I think this is balony (I didn’t try to scrutinize the underlying data).

This morning we had the 2nd reading of GDP for the 2nd quarter and it was lowered. Something is wrong somewhere here – somebody’s model is broken I think.

Interest rates are dead flat this morning while equities are trying to decide where to go next – 1st way up and then a tumble, now the S&P500 is up 1/4%–of course where we end up nobody knows.

So much for treading water until Thursday and Fridays economic reports–equities are ripping with the S&P500 up 1.27% right now.

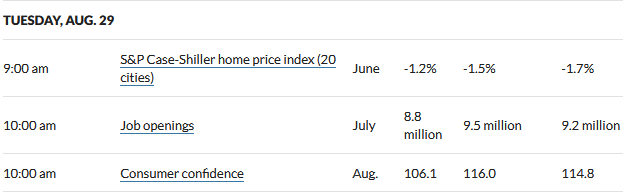

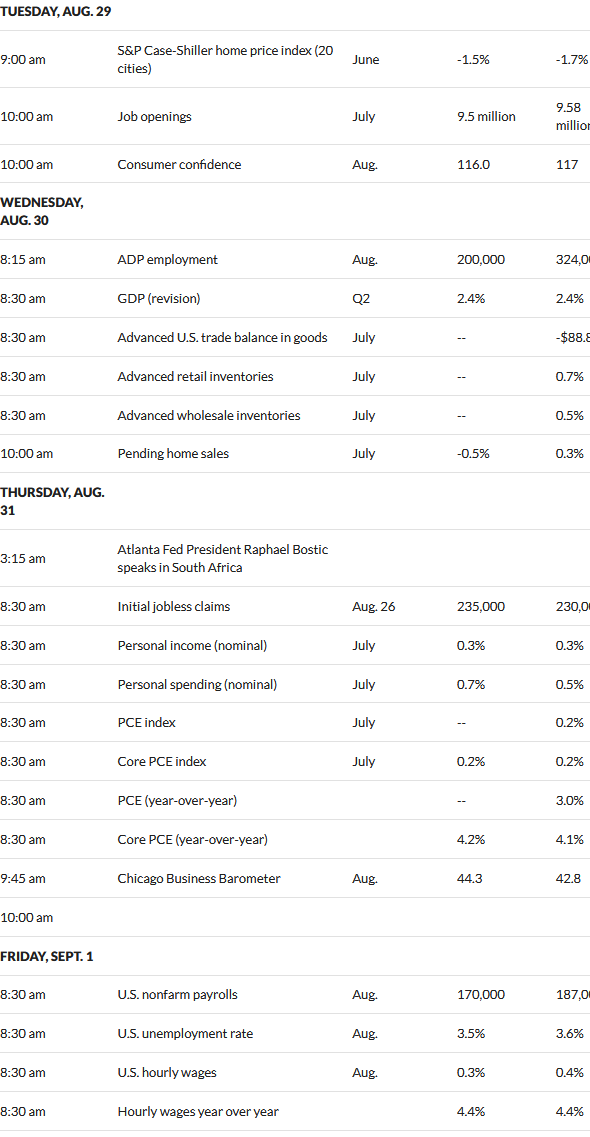

Along with equities ripping interest rates are tumbling pretty good as the consumer confidence numbers came in soft this morning and the Case Shiller home price index remains on the negative side of pricing–but slightly better than forecast. Right now the 10 year treasury is at 4.11% – down 10 basis poits on the day.

The job openings and labor turnover report (JOLTS) showed just 8.8 million jobs open right now – which while plenty high is a fair drop from 9.2 million last month and a forecast of 9.5 million.

Any report on employment is likely to get the FEDs attention – they absolutely want to see soft employment numbers – I am convinced it is 1 of just a handful of numbers that the FOMC committee wants to see soft as they are convinced inflation can’t be tamed without employment softening.

As most of you know already the stronger company’s are starting to eat the weak–I guess with interest rate where are where they are this shouldn’t be much of a surprise–it is hard to make money if you have to refinance your debt at super higher interest rates.

Also Kimco Realty (KIM) , a REIT owning open air malls, announced the pending acquisition of RPT Realty (RPT) which also owns open air malls. Again KIM is much larger and stronger than RPT which should keep the cost of capital favorable – at least relative to many smaller weaker company’s. RPT has a $50/share convertible preferred outstanding which is sounds like will remain outstanding.

I would expect we will see quite a few more acquisitions in the coming year–some will be forced of course, because of poor financials. Look to see quite a few deals in the banking space.

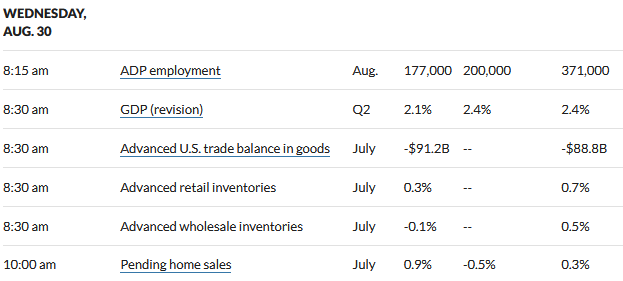

Yesterday equities moved relatively strongly higher–while today the indexes are essentially treading water—off less than 1/10%. Interest rates are up 1 basis points from the close yesterday–really just treading water awaiting the inflation number on Thursday (PCE) and employment report on Friday. We could see quiet markets for a couple of days, which I always welcome.

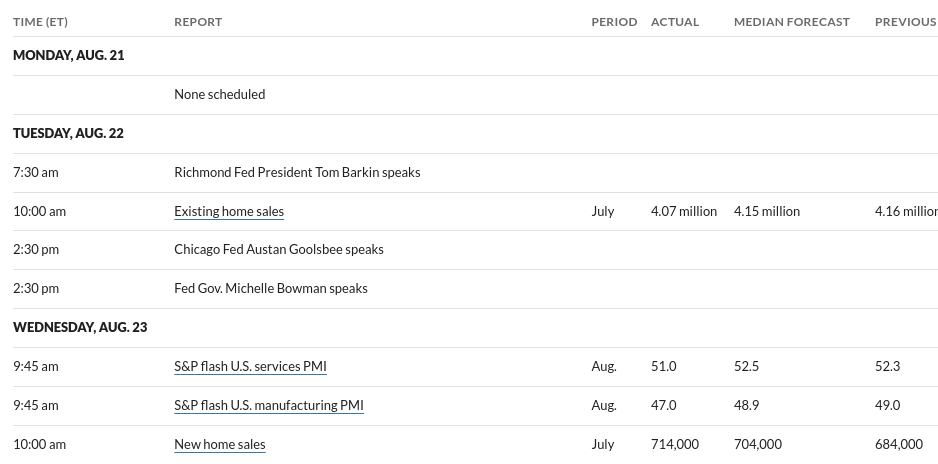

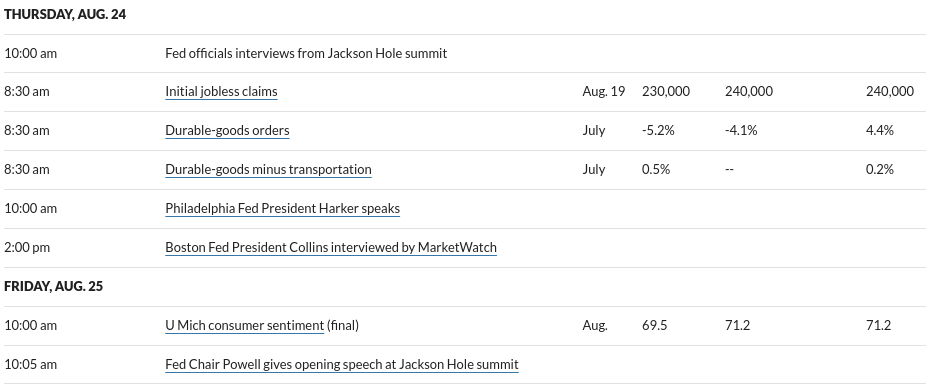

The S&P500 moved in a range of 4356 to 4458 a range of just over 2.3% before closing at 4406–a gain of .8% from the close the previous Friday. Markets seen to be undecided in which direction they would like to move. Friday started nicely up before heading way down and then way up as Fed Chair Powell was speaking at Jackson Hole. What is fairy clear is that without an economic collapse interest rates are going to remain at this level (if not higher) for the foreseeable future.

Interest rates, like equities, bounced up and down before settling near unchanged from the previous Friday–closing at 4.24% – up 1 basis point on the week. We are fortunate rates have not moved even further higher as new home sales were above forecast and 1st time employment claims were much lower than expected.

For the coming week we have the personal consumption expenditures report (PCE) on Thursday and then on Friday we have the employment report. Both of these reports could create fireworks–in particular the employment report is released on the Friday before the Labor Day holiday and volume could be lite.

The Fed Reserve balance sheet fell by just a measly $6 billion last week following a giant sized drop the week before (over $60 billion last week).

We had a week of near unchanged $25/share preferred and baby bonds last week with the average share rising 2 cents. Investment grade issues moved 4 cents higher while banking issues moved 7 cents higher.

NO Chart this morning – although I will post the chart when I am back in the office this afternoon. I am out of town yet until mid day this afternoon and hopefully I can get back in the swing of things.

Yesterday was a nicely green day in all my accounts—the 10 year treasury tumbling 13 basis points will do that. It is always helpful to have common shares move higher–although common shares being dragged higher and higher based on a few tech stocks seems like a long term recipe for trouble down the road, but once again with the amount of money on the sidelines (really in money markets, CDs and treasuries) there is plenty of future dry powder.

I see that the NASDAQ is up 1% this morning with the S&P500 being drug higher with the tech stocks composition–the DJIA is lagging. Interest rates are up by 4 basis points this morning. Yesterday we had the purchasing managers indexes for services and manufacturing come in soft and of course today we have 1st time unemployment claims which is one of the most closely watched pieces of data – the forecast is for 240,000 1st time claims–claims numbers at this level hardly indicates economic softness.

As I mentioned yesterday I am on the road for the balance of the week into Monday so likely will do no buying or selling, but I do have a number of good til cancelled buy and sell orders out there so maybe something will execute but doubtful since my price levels are aggressive.

I am checking CD rates while I am away—not seeing anything above 5.5% this morning so will just keep watching–by the end of September decisions will have to be made on whether to lock down some more as I have maturities throughout the next 5 weeks and I don’t want funds to build up to too high of a level when there good alternatives available.