After a few days of dipping into the 4.53% just a few days ago interest rates are trying to push higher once again–the 10 year treasury is trading at 4.74% right now at 5 a.m. (central). Folks are saying that these high rates are doing the work of the Fed and over time – months and months this may be true, but the underlying cause is a bit scary – too much supply period. We will see supply continue to be heavy for years to come–will there be demand for all the paper at current interest rates or will investors demand higher rates? A slowing economy caused by high interest rates isn’t much of an answer to a spending problem–in fact over the course of months and months (or a year) the slowing economy will cause larger deficits as tax revenues slow. Another fine mess we have on our hands.

I’ve continued to CD rates – on Fido this morning the top rate is 5.75% which is a 5 year, callable from Southern First Bank–the issue is callable starting in 6 months. Over at eTrade there are 5.7% CDs available for 1 or 2 years – both are callable. I think we will have higher rates soon–can we see 6% yet this year?

I am looking forward to earnings from the regional and community banks which we will see soon – starting next week and then into October. As noted I held preferreds in numerous small banks–and have unloaded some for decent gains, but I continue to hold a number of them. Almost all these issues are around break even (including dividends). I had decent gains in all of these issues, but let some of them slip away. I am looking to sell these issues and may do so at any time – I am concerned about commercial real estate with some of them although they haven’t shown great stress to this point in time.

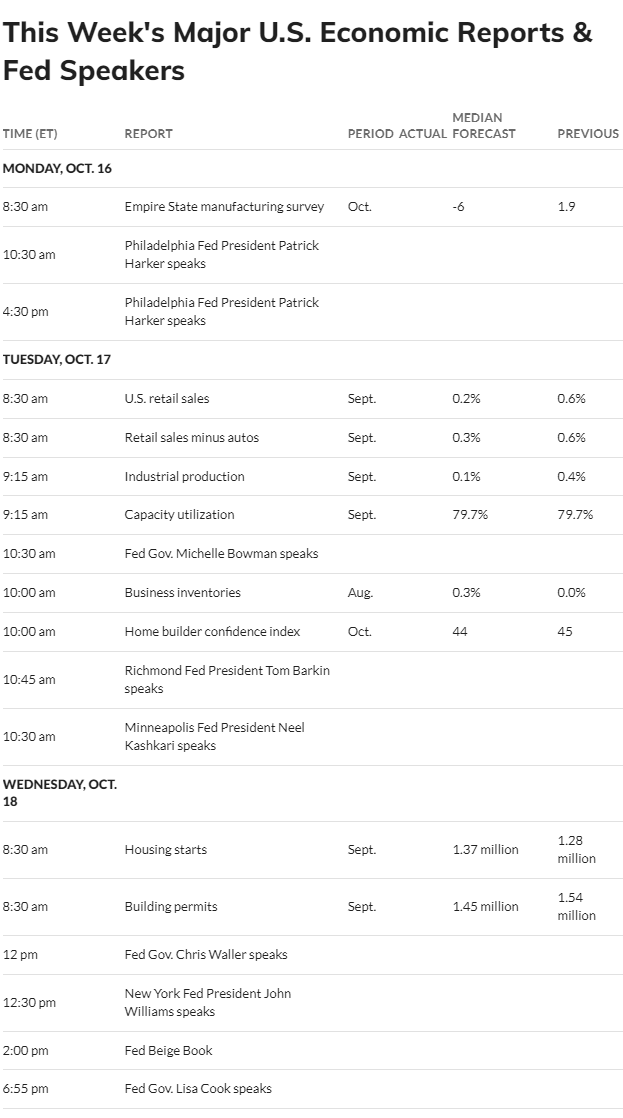

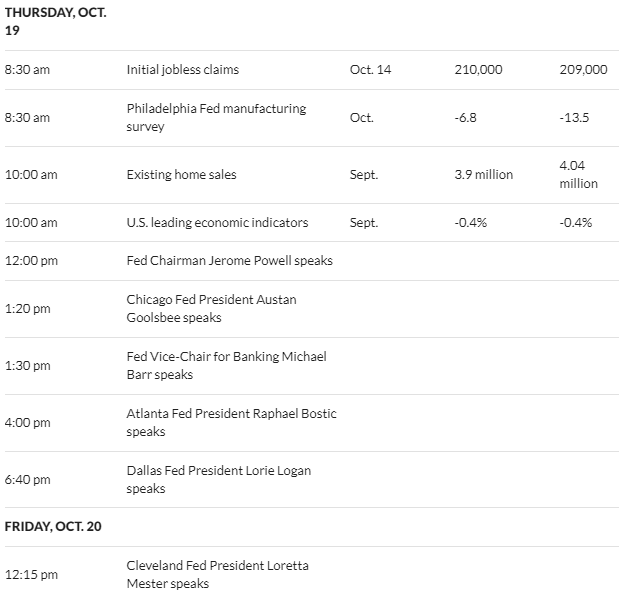

Once again today we have a number of Fed yakkers–and it is fair to assume they will be dovish in the short term, but this is baked into equity markets and interest rates will move independent of their jawboning for now–their yakking is loosing its punch.

We have a few economic reports this morning–retail sales will be parsed for the ‘health of the consumer’–we’ll see.