I continue to add mid level quality preferreds to our portfolios–some might say low quality for some of the issues–it is starting to feel like the ‘olden days’ after tending toward higher quality issues for the last 9 months. I will continue to hold plenty of dry powder–around 20 to 25%.

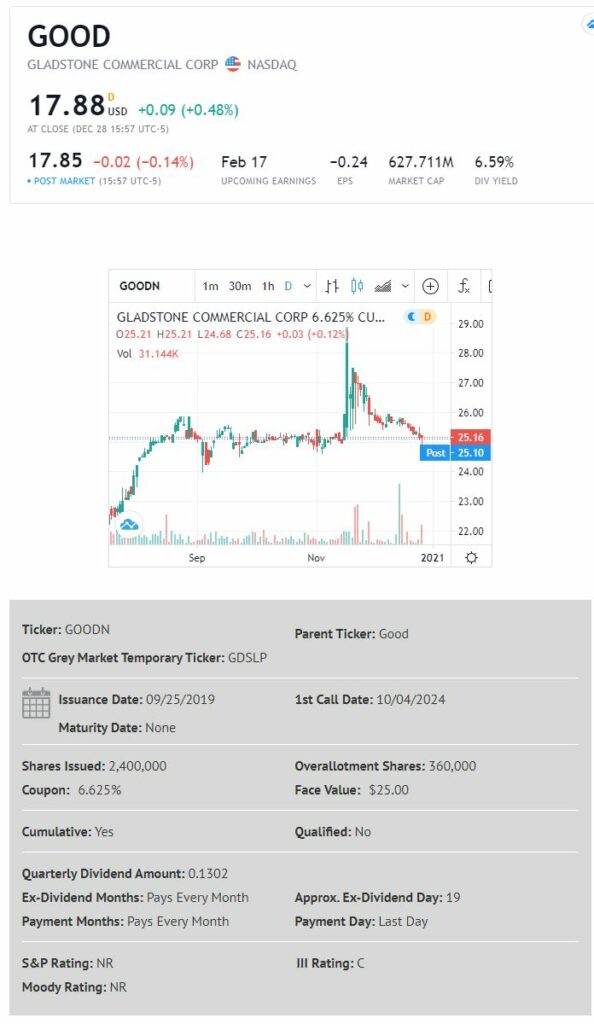

Today I added a 1/2 position in the Gladstone Commercial (GOOD) 6.625% monthly paying, cumulative, perpetual preferred (GOODN)

Gladstone Commercial is a triple net lease REIT focused office and industrial properties. I am not impressed by their financials, but they do cover their $1.50/share common stock dividend, which gives a nice level to safety for preferred shares. They have collected 99% of their lease payments in the most recent months–but personally one has to wonder about the future with ‘work from home’ likely to cut into office demand to some level.

The companies most recent earnings release can be read here.

These preferred shares trade up last month–a bunch, but now are back down to earth–seems like a good time to put a few shares in the portfolio.

Just a note that the REIT has a 7% issue outstanding (GOODM) as well which is trading at the same level as the 6.625% issue . An investor could well purchase this issue, but it has call protection only until 5/21 so the holding could be short term if bought–but either if fine.

I just read the Mad Money recap: https://www.cnbc.com/2021/01/05/cramer-lightning-round-hawaiian-airlines-stock-is-too-dicey.html

Here is the comment on Gladstone Commercial: “It’s got an 8.4% yield. That is too high for me, it’s a red flag. I’m going to have to take a pass.”

This kind of top-notch, bearish analysis would leave me concerned as I picked up a little GOODN recently but a wise man once said “Cramer is a simulation. He’s not real.”

Do you know of any stocks, bonds, real estate, literally ANYTHING that is yielding 9% right now that you would consider low risk? I’m not arguing whether it will be a good investment or not, but Cramer is right – a high yield is a sign of high risk.

Karma, while I agree, I think Cramer is thinking in terms of common stock which is lower stack and ultimately generally more pay out cash obligations for a company than a preferred issuance. If I got a $100 dollars every time preferred stock was mentioned on CNBC, I still wouldnt have any money, ha.

Presently I own 2 preferred stocks yielding plus 9% (well one actually is a baby bond, note) but I certainly dont consider them safe though.

As for GOOD debt at 6%+, that’s junk debt yield, so one should assume they are buying junk debt.

To those of you wanting to go broke I offer 2 suggestions:

1) Follow Cramer, so you can buy high and sell low consistently. Just look at his investment recommendations over time.

2) Follow HDO, so you van buy crap when it is hot and watch it sink when the market is stressed. They are the Bermuda Triangle of investment advice. They also front run all their recommendations.

Well, KC, I own a lot of EPD, now 9+% tax-deferred, I sleep very well with it, and have for many years.

But, hey, that’s just me. 😉

Preferreds are becoming a crowded trade. I’ve taken profit on probably 40 of them over the past 3 mos, some more than once. The prices frequently don’t reflect the quality of the underlying.

The wiser purchase at this point are first positions in quality holdings such as EPD (9.10%), MMP (9.70%), MO (8.45%) or T (7.30%). Scale into them, assume they will go down, treat them as bonds.

Bot some GOODM the other day at near par ok w potential call risk for some pennies thru May or holding if not called at 7%. Have GOODN on watch if there is some price distortion etc. Agree w Joel A. there could be slow int rate creep up over the next few years BUT investor interest in pfds is so strong and probably will be in light of retiree income demands and ETF/CEF needs that a few nibbles are fine here and there. I believe in general this demand should keep pfds stronger relative to other income producers.

Any time I can get 7-8% on a decent pfd I am ok w that. Best to all!

Bea–certainly 7% on anything now is spectacular (at least in my conservative mind)–and demand is crazy for most income issues, as you said–even the junkiest has crept higher as quality issues trade at sky high levels.

Each investor should follow their own needs and demeanor, esp since many here have honed their plans with years of actual experience.

Maybe I am a true skeptic and contrarian; many of the comments above can be markers of a topping, even if shallow. A general chasing, general acceptance of downgrading, FOMO, no dry powder, etc. Time will tell.

If this was not a environment where I could comfortably print this, then I would not. Seems this is the Big Boy Club.

For me? I have a full investment of 30% cash + margin, in a smattering of open buy orders in taxable accounts since I do not believe that every order would fill within a few days and zoom margin use. Would love to get a few cherries with great DNA for my solo-annuity-trust account.

I think that the bond-like elements of preferreds may reassert in a long, slow, protracted rising interest rate environment and I may have some very long holds (read: ’til death us do part). Grid has referred to why-call-issues that have been embedded in balance sheets from the decades past. Some of today’s perpetuals and super long bonds are going to be around ‘forever’ too. Gotta rely on the coupon? Maybe.

PS: Last March I had ALL my cash tied up waiting on two very deferred closings and watched the train roll by while the man in the caboose threw me a lump of coal.

Signed, Gun-shy

I agree with the topping, especially in preferreds. I never buy above call price, which has really limited the options to buy in this market, unless you are willing to dig through the garbage. I’m not sure that the level of dry powder really tells you anything though. From my view, there’s usually somewhere to invest, and it doesn’t have to be stocks. You should be on offense until the score is so high that you can setup the never homeless again lockbox.

Anyone have an idea why this (GOODN) spiked above 28? I got out around 26 (not smart enough to get 28+), and have bought back at 25.4 and less.

I bought a full position at initial offering, and have been pleased with performance to date.

I added yesterday. Landlord, I suspect you’re correct they’re doing ATM with GOOD. Given LAND’s announced purchases the past few weeks, I suspect they’ll be issuing common and preferred also. I’ve owned GOODN and M for years. GOOD never cut their distribution during the GFC and Tim, you’re right, the $1.50 gives nice coverage.

Just my humble opinion

David–I think the common dividend should be cut in half honestly, but I don’t think they will do that unless forced by much poorer business conditions. They are paying about $50 million in common dividends annually so this does provide a very good backstop toward preferred dividends. The risk reward is adequate for now–BUT if financials erode from here folks may dump the preferred issues along with the common.

Tim, I agree the common dividend should be reduced. I’ve avoided the common over the years but do like the Preferred. Any thoughts on ARRpC?

Based on price action, I suspect GOOD is issuing shares at the market in both the N and M series.

If it was ATM issuance, i think it was for GOODN only, not for GOODM. According to their most recent 10-Q, they have an ATM in place for GOODN (aka Series E), but I don’t see any mention of one for GOODM (aka Series D):

Page 24 of the 10-Q:

“We have an At-the-Market Equity Offering Sales Agreement with sales agents Baird, Goldman Sachs, Stifel, Fifth Third, and U.S. Bancorp Investments, Inc., pursuant to which we may, from time to time, offer to sell shares of our Series E Preferred Stock in an aggregate offering price of up to $100.0 million. We sold 239,399 shares of our Series E Preferred Stock, raising $5.6 million in net proceeds under the Series E Preferred Stock Sales Agreement during the nine months ended September 30, 2020. As of

September 30, 2020, we had remaining capacity to sell up to $94.4 million of Series E Preferred Stock under the Series E Preferred Stock Sales Agreement.”

Actually, GOOD now has a new (non-traded for now) 6% preferred called GOODF that is also being used to raise funds. Issued 45K shares of GOODF during the 3rd quarter.

It isn’t the best deal for common shareholders, since based on the prospectus filed on June 29th 11.5% (6% commission, 3.0% deal manager fee and 2.5% for expense) of any offering proceeds would go toward fees and expenses. This means that GOOD will get $20.80 for every share of the Series F it sells.

All of those large fees go to David Gladstone’s brokerage company.

Series F Preferred Stock

On February 20, 2020, the Company filed with the Maryland Department of Assessments and Taxation Articles Supplementary (i) setting forth the rights, preferences and terms

of the Series F Preferred Stock and (ii) reclassifying and designating 26,000,000 shares of the Company’s authorized and unissued shares of common stock as shares of Series F

Preferred Stock. The reclassification decreased the number of shares classified as common stock from 86,290,000 shares immediately prior to the reclassification to 60,290,000

shares immediately after the reclassification. We sold 45,102 shares of our Series F Preferred Stock, raising $1.0 million in net proceeds during the nine months ended

September 30, 2020. As of September 30, 2020, we had remaining capacity to sell up to $635.4 million of Series F Preferred Stock.

I have $22.45 cash across all my accounts. I keep buying the safest and best income play I can find whenever funds hit my account. My goal is income. More income. And even more.

So far so good.

JMO

Camroc, $22.45? That wont even buy you a bottle of wine. But with my palate it buys two!

camroc–you can get that to work with a fractional share purchase.

lol 😉

So, how much in each account?

As my folks used to say- Don’t spend it all in one place!

Live longer & prosper.

Well, Gary, not enough in any of them to buy even one share of anything on my list.

And despite Tim’s suggestion about fractional shares, there are just some things up with which I will not put. 😉

I was looking at these today as well, but no money to buy 🙁

DaddyDollars–I have had 30% for months and now moving it down to 20%ish so available cash was no problem.

Tim, thanks again for your sharp mind and eye. I sold some TDE, just pennies above if it get called and placed an order for GOODN, yield beating GJH (Gridbird’s safe haven USM, subsidiary of TDS). Thanks to Gridbird, Farmland preferred FPI-B is behaving like a SWAN eREIT preferred. That Preferred Investor’s pick (who became Rida Morwa’s occasional collaborator but highly regarded by Gridbird) has JMPNL, a 7.25% baby bond. I have small position in my IRA. However, JMP has not been paying dividend to its common shareholders throughout 2020, despite its price appreciation.

That fake electric company SPKEP is also above par before year end Ex Div date. My friend at Doug Le Du’s place uses technical analyses buy SPKE and then sell it to buy SPKEP using options at times. This is way above my skill level. I bought just 260 shares after buying and selling the SPKEP. I believe the market makers OR the company plays games with the commons and the preferreds. I will not buy at this junction. GLOP’s mother company GLOG is hurting for money. It stopped paying dividend or reduced to next to nothing to GLOG. But this Greek shipper is reasonably honest, has so far not stopped the dividend on GLOP-A, B and C. Earlier, I sold some A and replaced with the mother company’s Preferred, GLOG-A, which pays huge dividends all QDI. GLOG-A has been behaving nicely. Until recently, GLOP-A, B, and C has been behaving alright. Some year end selling with below average volume. For those who want to take some reasonably safe shipper stock, GLOG-A should be okay because the owners have lots of common general partner shares plus the A preferred units. Rumor says the risk for GLOP preferreds may become orphan. Except for Navio Maritime, most Greek ship owners are daring souls but generally not dishonest IMHO. BTW, Rida Morwa posted an article on WPG (Mall preferreds vs real unsecured senior bonds). Apparently according to Vanguard WPG rated C for both Moody and SP experienced some upgrade after they declared their financials. I sold my IRA position on the WPG-H with no net loss except for opportunity cost and replaced with the bond. Strange thing is: Preferreds stay firm, bond declined a little for a lousy fraction of one percent in yield. Lots of Yield hogs out there LOL.

johnkcal…so what happens if GLOP preferreds become orphaned? Do they continue to pay?

This question was debated. The market action however suggest that holders of GLOP A, B and C continue to AssUMe (Assume) that GLOG will not dump its “child” (GLOP and all the three grandchildren from GLOP, A, B and C). I brought it up to share with people who may still have positions with the GLOP-A, B or C. GLOG-A has been climbing nicely and this may be a reasonable bet for those who may want to speculate for a very attractive yield. My GLOG-A already saw some unrealized gain. With the trade war probably should subside and China recovering from its COVID, it should be reasonable to assume that the shippers should see some improvement in demand. Just my thought. Of course I could be totally wrong. BTW, many assume Teekey Offshore, now part of Brookfield’s empire would be delisted. After minority shareholders kept on posting SA articles urging Brookfield to offer some premium. Brookfield, being a classy private equity firm (real Billionaires with lots of assets) continue to pay the dividend without skipping and the share price has climbed nearly to $20. However, I was stupid and bought some near par still seeing unrealized loss. But I will hold. ALIN-E, B and A. I have moderate positions on the E and B. Teekay offshore is still losing money, but less. I sleep very well with Brookfield backing this company., BTW, BEP common for Brookfield Renewable (wind and sun) and BEPC (the Wind and Sun acquired TerraFarm) are both great. Then it dropped significantly because the yield was not competitive. I foolishly sold it and replaced with BIP (Infrastructure). That was dumb from a SA article. I am not preaching renewable energy because I hold EPD and MMP ( the worst investment is ET but EPD and MMP both suffer just like XOM and Chevron. Someone needs to tell Joe Bidan to contact Brookfield Renewable to LEARN how to do it without borrowing money and make the country STRONG. I still love my EVA (MLP but actually a great Renewable) with the best K1 I have seen. Currently the price seems very close to the analysts’ estimate. Be careful not to have more than $1,000 income in your IRA to avoid the awful UBIT.

Thanks for the reply johnkcal. I’m sitting with a small position in GLOP-b which has been underwater from nearly the day I bought it. If it gets back into the $17 range, I’m going to bail. Don’t totally understand the partnership setups so my bad, but fortunately only have a small amount.

ONlY the GLOG-A is called Partnership. If you look at the market action (simple price chart), you will see that GLOP-A, B and C all climbed after the reduction of the common GLOP to one penny. So, apparently the market ASSUMES that the savings from the One Quarter of dividends from commons will make everything alright. I moved some shares from my IRA account to taxable in the beginning of 2020, the share price actually increases. I will not be surprised that share prices could go up next week. Being a person who is slow to react as I did with CBL Mall tragedy (actually I forgot to sell and then thought it would recover. Ditto for Karfunkel family’s Amtrust. I pulled the trigger and sold 475 shares of B and 100 shares of A, bring a cap loss of almost $5000. Schwab told me that I can use that to offset the tax for 2020. Reducing both the Feds and State of California give a little over $1,000. I must learn NOT to bet big (or perhaps not at all) on these risky issues. Debt to equity ratio approximately 11 or 10. Nuts. I bought only 118 of OTRKP in my IRA account. Good luck and Happy New Year and please stay safe to all. My wife and daughter apparently had contact with a physical therapist who was found COVID 19 a few days ago. Thanks to Tim and Gridbird and all.

John

Why do you think TDE will be called? Its been callable for 5 years? Just hedging or is there some information out?

Thanks

It is difficult to tell. Hence, I quickly cancelled the rest of 300 shares SALE order. I typically err on the side of too fearful of CALL. TDE IMHO and at least one decent diligent SA writer (who no longer offer his service) is a safe sub Investment issue. These guys and gals at TDS and USM (its subsidiary) has learned how to compete against the GIANT but LAZY names like AT and T for decades. I thought about Gridbird’s BJH that USM 6.375% coupon trading above par. Then TDE is far more “generous”.