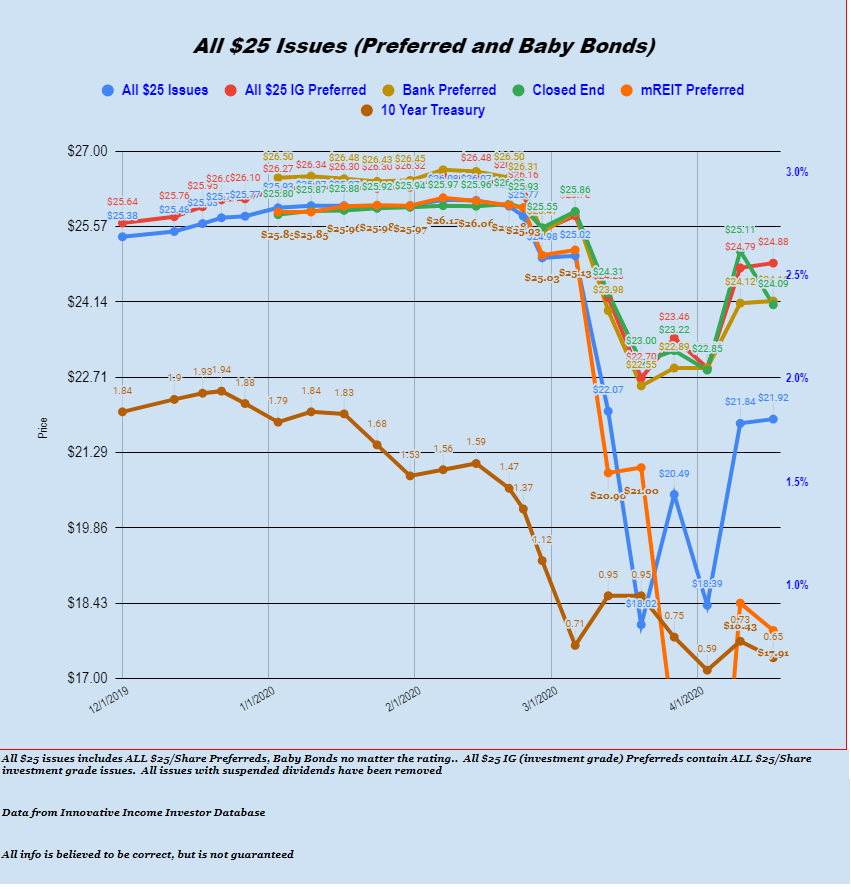

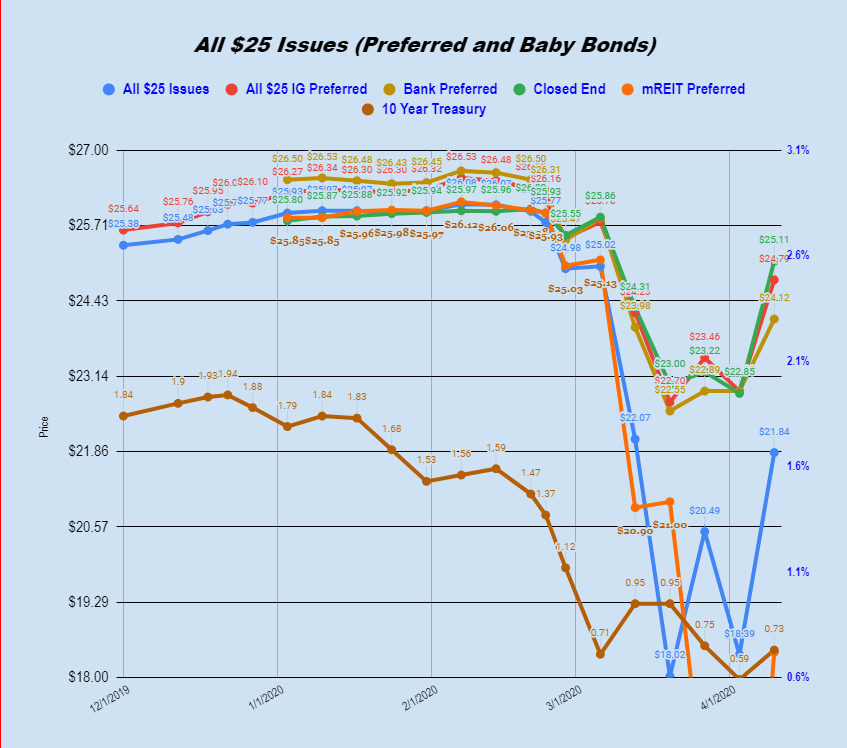

I give up on trying to predict these markets–I heard predictions yesterday and today of end of year SP500 values of 2,500 and I heard one of 3,700. 1 is a RECORD high and the other is 10-15% below current levels.

Personally I am highly suspect of current stock market levels–seems it is too optimistic–but in the end it doesn’t matter what I think.

Regardless of the predictions it seems as though some folks are predicting a return to normalcy in the 3rd quarter while others are looking for normalcy in early 2021. With the business destruction and desperation I am seeing I am more in the 2021 camp.

Yesterday I read that the airlines are so desperate for cash that they are selling ‘miles’ to the banks at large discounts–even with bail out money they all know they will not return to normal (or even 50% of normal) before at least the 4th quarter–if then.

Over in the comments this morning Charles M noted REIT CorEnergy (CORR) was taking a pummeling. Seems that Cox Energy, which accounts for 47% of the companies revenue has suspended payments. I see their common shares are down over $10 to around $14 while the companies 7.375% perpetual preferred shares (CORR-A) are off $4/share–around $14. The press release is here.

Hammerings like the one at CorEnergy are the type we will be seeing every week for the rest of the year–there is no visibility.

I know some folks are talking about large cooperative CHS. The company released earnings last Wednesday and they were typical with what we have been seeing from them for a couple years–almost all the earnings are coming from the refineries–very little from the ag end of the business. The press release is here. I suspect they will have reduced earnings from the current quarter as volumes of refined product will fall–and ag will not generate anything. codger mentioned today that their nitrogen investment (in CF Industries-CF) tossed off $5.7 million in net income last quarter–what a joke–$3 billion invested for $20-$25 million in annual income. That joke cost the last CEO his job.

Yesterday I bought a bit more VEREIT 6.70% preferred (VER-F) in the $22/share area–that was adding to current holdings.

Also as I mentioned yesterday I bought 100 shares of the Tri-Continental (TY) 5.0% perpetual--I paid a little below the $55 redemption price. I bought this as part of my 50-55% safe portion of the portfolio.

Here is how I am being forced (foreced because I have little visibility of the future) to set my investments up – like this—55% safe issues, which by their nature are lower coupons—maybe around 25% decent quality unrated issues-for instance American Homes 4 Rent (AMH) perpetuals and then 10% more speculative issues–i.e. mREIT and lodging preferreds.