Last week the S&P500 opened up the week at 2782, hit a low at 2721 and a high of 2879 and finally closed the week at 2874–a gain of over 3%.

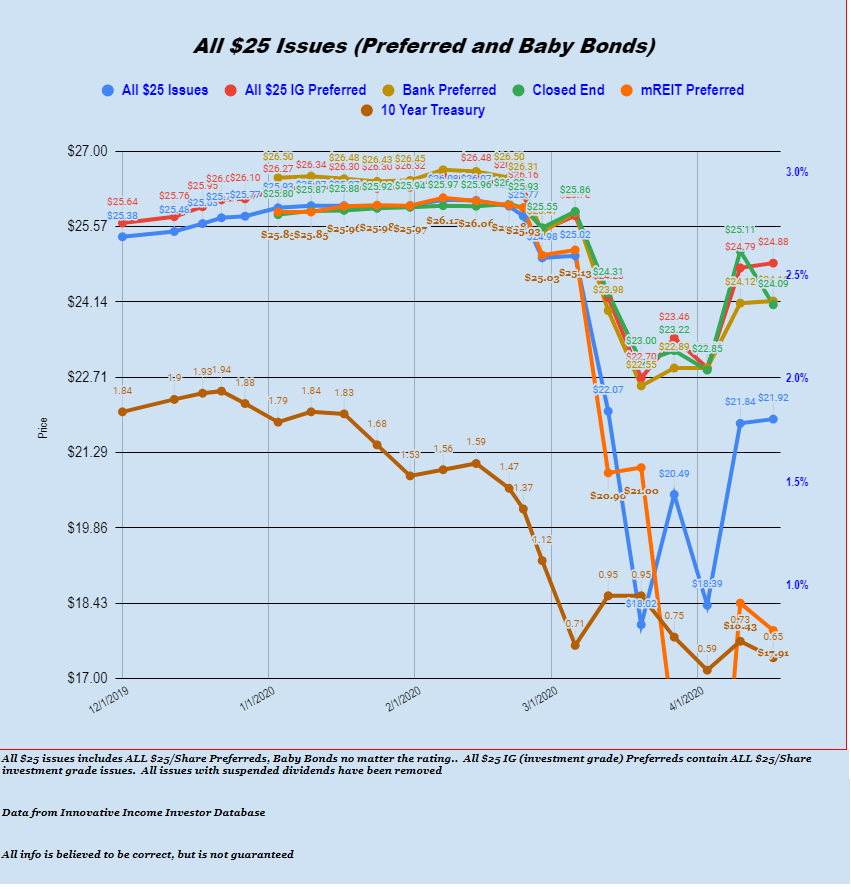

The 10 year treasury traded in a range of .58% to .76% before closing the week at .65%

The Fed Balance Sheet grew by almost a hefty $300 billion–to $6.4 trillion–a crazy number, but one which is heading higher–much higher.

The average $25 preferred stock and baby bonds moved higher by a measly 8 cents last week. Investment grade issues were 9 cents higher while utility issues we down 34 cents.

So this week we have the DJIA looking a bit weak to start off–down 400-500 points, but we have learned that the early pricing on stocks doesn’t mean very much as any minute the FED can step in and manipulate stock prices.

I believe I am around 63-64% invested (haven’t calculated exactly). As boring as it seems I will be watching–still watching for some bargains, but I still hold out belief that better bargains are likely coming.

As you all know by now crude oil (west Texas intermediate) is trading around $11-12/barrel–incredible. With little demand and an oversupply of about 20 million barrels/day how will energy move higher? I see that in the comments Fabrib posted that Oaktree Capital has given a $750 million unsecured loan to NuStar Energy (NS). The press release is here.