Last week was a phenomenal week in equities as the S&P500 as the index it opened the week at 2578 and closed the week at 2789–a gain that was highly ‘juiced‘ by the Fed’s printing presses.

The 10 year treasury traded in a range of .64% to a high of .78% before closing at .73%.

The Fed balance sheet grew by $172 billion to a new all time high of $6.08 trillion–on its way to at least the $10-12 trillion area this year (my guess).

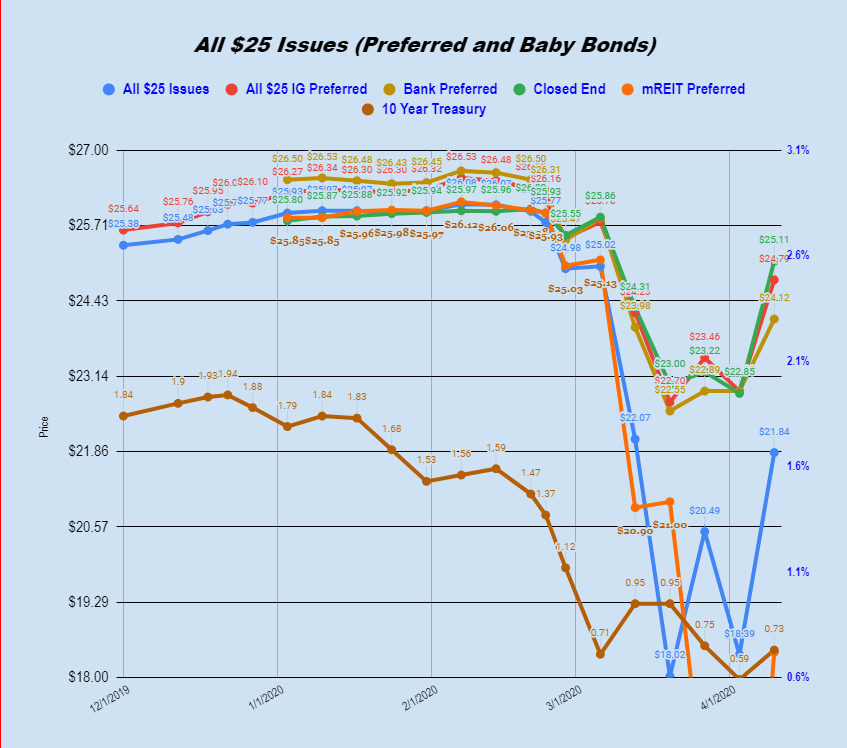

The average $25 preferred and baby bond closed last week at $21.84 after huge bounces in many areas–in particular mREITs. As expected CEF and UTE issues continued strong trading with CEF preferreds closing the week at $25.11 and all utility issues closing at $24.12.

So we are starting the week off with only small losses on equity indexes, but earnings season is about to begin. Whether investors pay too much attention is anyone’s guess , but does it matter anyway as the FED has taken the risk out of the risk/reward equation.

I am in the area of 62% invested and don’t really have a plan for the week. If there were bargains in CEF and UTE issues I would probably be a buyer–BUT I don’t expect any as they are already trading in the $25 area–and I want to buy lower.

Will the markets trade lower this week as the fundamental long term economic damage is finally admitted to? No one knows–but we always prefer to error on the side of being conservative.