Well with the little panic we had in bonds on Wednesday it is kind of nice to have the bond markets closed today. A 12 basis point increase is very close to where we could cause a stampede of folks out the low coupon preferreds and baby bonds.

We have had losses of about 1% (25 cents) on the average $25/share baby bond and preferred issue this week (of course some much more and some none at all). As you might expect the high quality, low coupon issues, fell by around 1.3% thus far on the week.

Now if you are an “immediate income investor” (you concentrate on the income stream versus total return) you might not care 1 wit whether prices are falling–you might even be saying that ‘more bargains for me’. On the other hand if you look at your total return and a few percentages here and a few there and pretty soon your capital has evaporated in sizable ways. There is no right or wrong way to look at these things–just the way that is best for you.

I started my move back into the short maturity issues this week–term preferreds and baby bonds–the list which you can see here. I am selling low coupons in particular those that are perpetual–I remain holding those that are low coupons with maturity dates in the next 5 years.

We all know from history that short dated maturities will move only modest amounts if interest rates continue to move higher since they have a date certain for repayment of your $25/share liquidation value at maturity.

Folks in low coupons will rotate out to some degree into higher coupon issues–say 6% and above.

Over time if rates continue to move higher all perpetuals are at risk of capital loss (which may or may not matter to some as noted above). The losses can be quite dramatic.

We all tend to forget where rates can go–we have been in a falling rate environment for so long – 40 years! No one can predict where rates are going, but it is always good to remember where they have been–because they can go there again.

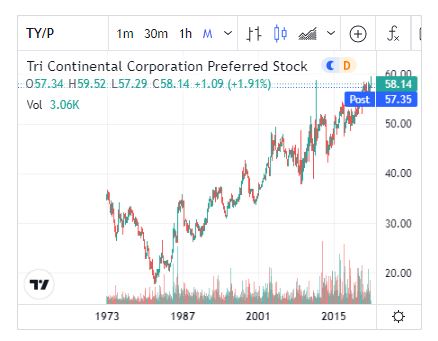

Here is my favorite chart of a perpetual that I love–the Tricontinental $2.50 Cumulative $50 Preferred which has been outstanding since 1963. This is an extremely high quality issue with asset coverage ratio of about 1,400%–it is redeemable anytime at $55/share.

Back in the early 1980’s it traded as low as $18/share. Now it is at $58. Never in my wildest dreams could I think of these shares revisiting $18–but it is a good illustration of the possible movement of share prices–let’s hope we never see this again (you all remember 13-18% mortgages).

It sounds like the microphone is getting passed around and each person has an opp to give a personal testimony. Amen! Each of us has rationalized life and the evidences we have seen to our own situation.

I have divided my treasure into three pools of about equal proportion. I do think we will see the ten at 2% sooner than later. Each of my pools have an income slant with differing performance expectation for each pool. All are slanted toward IG:

1) If rates go up then my resets benefit. All are decent income holdings at my cost Let them reset or be called. The Canadian adventure was particularly beneficial and guys like DE Bob, were instrumental in getting me to test the waters.

2) If the rates go up, then (in theory) the stocks ( mostly cyclical commodity and some pharma) should be benefitting by raising divs and growing price for cap gains to be peeled off. I have been trying to use sell limits over the top, but my ego keeps letting them expire. Kinda like waiting for a fat picth and not swinging at strikes.

3) Fixed rates with a term focus and long term annuity type holds if the prices decline steadily from rates/inflation, just take the income and sell the remainder after I am gone. At my age it beats buying an annuity. I have a ‘feeling’ (bad investment tactic!) that there will be an opp to sell those fixed rate out at another point in time when everyone, as has happened in every generation, swears off of equities again. Then I will consider strategic sells into that bond rally. Yes, I think we will see that as a possible outcome from this bullish equity rage.

I must say that this site, along with almost forty years of investing, got me to a place where I could retire and at least THINK I have something figured out. I am glad to have held real estate during the lucky (my birth timing) straightline interest rate decline. I was not that smart, but lucky indeed.

The Very Best to ALL!! Thanks for the honest sharing. JA

I am looking at the twilight years of my investing. I have enjoyed many years of in and out of preferreds. I can remember when GE and Wisconsin Power each had a series of preferreds, rated AAA and at reasonable rates. My wife and I have chosen Vanguard National Trust to manage our assets, when we are no longer able, and distribute the remainder to our beneficiaries when we are gone. Most of the assets are at Vanguard, but 25% are at Merrill Lynch which I would like to transfer to Vanguard to make the transition to the trust simple and complete. The problem is that there are some shares of AATRL and some shares of WTREP in the Merrill account which Vanguard will not accept because they are not traded on an exchange. Further, I am told that Merrill will not hold a security with “0” value by itself. I tried to sell the AATRL, but Merrill will not sell it. I had a position at Vanguard which sold, but Vanguard would not accept a transfer of my Merrill shares. My major concern is that some of the positions I hold will end up in the SEC 15c2-11 penalty box, as with AAPLL, which would prevent them from becoming a part of the Vanguard Trust. I am in the process of selling anything that does not have a maturity that I can see is on my horizon. Since the SEC penalty box does not affect dividends I will put the proceeds in a Preferred Stock Fund. I have never liked fixed income funds, but where I am in life, I can accept the lower return and the peace of mind it brings.

I lived as an adult through this time frame and it was difficult, but eventually it ended. I think the Fed will go all out to keep it from happening again—even by forcing a severe, long term recession if necessary. However, we need to service the federal debt at the same time. This is where it gets tricky. Somehow, Japan manages to service its debt and at the same time keep interest rates low while forever having a very low growth, recessionary environment. This is where the U.S. is headed as our population matures. Federal debt to GDP will continue to go higher. We are a mature economic nation. As investors, we need to adjust to it. I like these kind of discussions on this site because it gives me insight/feedback on what individual investors like myself are thinking. and doing.

Until I see actual evidence of rates going up and stay stable between 1.80% and 2.0% for the 10 year I will only make slow and gradual changes. Otherwise I won’t bother buy anything that pays less then 4.5% QDI today. Some opportunities have come up to offload 4-4.25% issues so I took it but there is no rush. We might not sit above 1.75% for the 10 yr for another 6 months. I still have quite a few IG grade lower yielders. But if I can sell a 4.25% QDI I bought at 25 for 25.50 I will probably take action and sell it if I know of something better to switch to.

What I have noticed is that when the market throws a fit is that even high grade 5% get wrecked. Use PSA-G as an example in early 2018, late 2018, and early 2020. We are talking 21-23 a share easy.

Otherwise using PSA-G once again as an example, knowing that the 10 yr yield was 2.12% at one point in 2017, knowing that the 10 yr yield was 2.8% at one point in 2018, etc.. it held up pretty darn well. It was the market downturns that wrecked it’s reasonably stable chart.

So if rates go up and the market has a fit I feel nothing will be protected for that period of time. Everything will go down which is becoming a more likely scenario. If the market stays down so do rates. I just don’t see inflation running hot much longer once things settle down around the world. I hate the word transitory but it is probably correct in a longer amount of time then people thought.

I will stay invested in the usual suspects but slowly upgrade where I can. REIT 4-4.5% yielders are a definite no go zone now. QDI has to be above 4.5% now. It is ok to have a nice pile of cash but nothing like 30% cash or above for me.

I also think by the time that list of preferred/BBs have a chance to mature we will have gone through a whole cycle of rates going up past 2.5% and back down again. I just don’t see the 1970s/early 1980s repeating. I won’t plan for that event. I am young enough where I don’t need to spend the divs/interest. I can just reinvest it in higher yielding new issues if it happens. Like you said everyone’s situation is different but I just think that planning on a day that the 10 yr will be above 2.75% anytime soon is probably unwise.

Yes, we have already had two interest rate increase cycles (failed ones) in past 10 years, and that did not stop the 40 year downtrend march of interest rates. The trend yet today remains unbroken. The most recent spike in rates this week has gotten us all the way back to… 16 bps below the years high back in March.

Yet its clearly understood the risk is a spike to the upside or a “market taper tantrum” without the actual interest rate follow through. I personally tweak where I can, but Im not going all in on letting the tail wag the dog. In other words letting the terms of an issue take precedent over the actual company.

If I dont trust a company the terms are irrelevant to me (well a few I own dont fit that mold unfortunately).

But, I do find it very troubling where buying a “lowly Ibond” presently nets a higher income yield than probably 90% of all preferreds outstanding. That causes serious pause, risk management wise. That being said almost half of mine are are resets, adjustables, or term dated (10 years or less if that can be construed as such)….Capital preservation versus present income want or need is a serious conflicting battle now. Getting both in conjunction now is a tough task indeed.

fc–that is what makes a market–we are all different.

Glad to see someone say the true fact that we have been in 40 years of falling rates. Get so tired of all the SA authors saying how well REIT’s and other stocks perform in a rising rate environment when we haven’t had such meaningful periods.

William – I made my first stock purchase 50 years ago last month–I remember the period of 1968 to 1982 – stocks were lousy for that entire period (falling) and we know where rates went in the 1980’s. Except for a few blips here and there the bond market has been like shooting fish in a barrel.

Tim – understood and agree with your plan to go short and term preferred (me too). What are your thoughts on fixed / floating rate preferreds such as NRZ-B and NLY-G? Do the FF’s afford protection to a potential rate increase?

I would think some protection but not full protection, prices may drop with rising rates just not as much. There may be some bargains on issues that don’t go float for a few years.

Yes, that is a very much “it depends” situation. In a market rout they all get thrown in the trash bin. That is why my WTREP is the safest preferred outstanding. Its already been remarked to $0.00 in my account but still pays 7.5% annually off of par value. Zero downside and all upside, lol.

Going forward too many things matter besides whether its just a floater or not. Long end movement, timely Fed hikes (or not), credit spreads versus IG and or Junk, stock market sentiment (most preferreds follow in sympathy more than most admit), etc. Also one has to be aware of the reset adjustment when it becomes a floater versus what it was issued at. Many were set a few years back with lower adjustments, and even with a several rate hikes they will become live floaters at a yield still under their issued yield which could pull its pricing down there, also.

Proto123–wish we had hard evidence of the value of FTF’s, but since we haven’t had truly rising rates for decades I don’t know. It is my opinion that no one can truly know if they are helpful. We need 3 month libor (or SOFR) to go 1.50% higher to find out what happens with these FTF issues. Sorry I am of no help on your question.

Proto, I can’t comment on those two particular issues, but I am dipping my toe in the f2f waters (thanks to this site) with a strong preference toward either

a) those which do not float with 3M Libor (5y/7y/10y treas far preferable) or

b) if I do choose to go with a 3M Libor float, ensuring that the corresponding fixed element is >= 5%

Tim said: “I remember the period of 1968 to 1982 – stocks were lousy for that entire period”

A history lessen for the younger crowd. The Dow hit 1,000 in 1966 and did NOT rise above it until 1982. So literally ZERO capital gains, but back then the dividend yield was higher. But that is not the bad part. With inflation factored in, a 1,000 Dow in 1982 was worth ~ 333. So you lost two thirds of your buying power over those 16 years.

If and it is a big if, inflation is high and NOT transitory, say 6+% ad infinitem, all of our preferreds will be crushed. Stocks will be crushed. Short term baby bonds that mature in say 1 to 5 years will be relative real winners.

It was a devastating time for many seniors that relied on social security and pensions. Many had to sell their homes because they could not afford the taxes/insurance/utilities. And yes, some of them literally were eating dog food. Not many of those seniors are still around to tell you firsthand what it was like. Let’s just say I had a front row seat.

I’m becoming more and more convinced that we may be headed into a world where inflation remains elevated but rates do not follow suit, therefore bonds may not be crushed but also won’t have great returns. My reasoning is that like Japan the Fed can’t afford to allow long rates to rise since the government can’t afford the higher interest rates. We enter a period of stagflation, higher inflation but low rates and low growth. That said I’m still staying short, avoiding perpetuals, and buying more stocks with the ability to grow dividends.

Agree,, IMHO I think we get some inflation but i don’t see interest rates going up much but I do think this will cause higher equity prices. I have sold most of my preferreds in the 4-4.5% yield range. For now I am keeping anything over 5%.