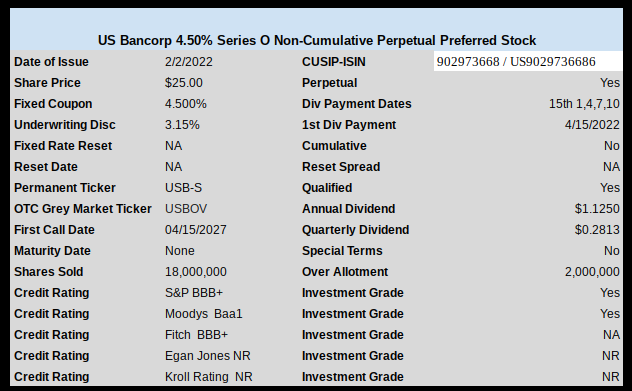

US Bancorp (USB) has priced their recently announced new perpetual preferred stock issue.

The issue prices with coupon of 4.50% for 18 million shares (with another 2 million available for over allotment). The issue is investment grade.

The issue is redeemable starting 4/15/2027.

This issue will trade immediately under OTC ticker USBOV.

The pricing term sheet can be found here.

Just curious why there is nothing here or Quantum Online in the way of Prospectus or Summary Prospectus on the BoA 4.75% new preferred…BACPRS/ BACLX?

Bought shares at $24.80 yesterday based on what’s on the BofA Investor Relations page – Preferred Shares. There also seems to be a lower coupon RR series there.

Richard: try https://www.sec.gov/Archives/edgar/data/0000070858/000119312522020169/d278452dfwp.htm

We, are buying 4.50% return …A-B rated,,at less then $23.00 that is 8% return at calling date….Georges….

Georges – What issue are you talking about? I don’t see where this issue has traded anywhere near $23 as of yet. And assuming we’re now in a rising interest rate environment, why do you feel that the yield to call is a particularly relevant number? What would be the issuer’s economic reason for calling in this environment? Most likely part of their incentive in isssuing (assuming you’re talking about BAC) is to lock in what they believe will ultimately turn out to be cheap long term borrowing costs.

BOA is predicting 7 interest rate hikes this year, 4 more next year. Buying anything under 6% coupon now that isn’t term seems like the road to capital erosion.

not that I disagree but have you ever noticed how once practically any trend surfaces on Wall St. how there’s always a publicity race as to who can make the most outlandish predictions to the extreme???? So they up the anti to 7 until someone else says 8 so they can get the attention of the talking heads… It happens all the time – Yes I’ve been planning for higher interest rates for way too long, so I’m certainly not one to disagree with the direction, but 7 rises this year??? I can’t help but think of the famous Paul Samuelson quote,

“The stock market has predicted nine out of the last five recessions.”

I agree with you, 2WR. i was shocked at that, plus another major bank also predicted 11 hikes in 2 years (brain fog, i can’t remember which one). But ya, the hysteria of the moment leads to talking heads trying to top each others predictions. In the case, however, even if they are far off, i still think anything under 6% coupon won’t hold par.

The wall street people always try to outdo eachother on predictions…..but honestly…..the fed is always wrong…I wouldn’t be surprised if they raised every month starting in March.

The Fed is always wrong, but so is Wall Street: https://mobile.twitter.com/ResearchQf/status/1487220454087700480?cxt=HHwWgMC9yfLH1aMpAAAA

Guess what? No one can predict the future with much accuracy.

The prediction that the fed is always wrong sure seems to be accurate a lot….like…..always lol.

It does look like the 6% stuff is holding – at least the stuff I’m looking at.

I do agree that anything under the 4.5% range will result in a loss of capital – at least for the remainder of this year.

However, IMO, if any BOA employee thinks the FED will raise rates 7 times should be shown the door and be shunned as a outcast to society. Basically they are nuts.

Most of the problems causing inflation are structural related.

Just for argument sake, will rising interest rates:

-Increase energy production

-Decrease unemployment an lower wedges

-Stop the deficit spending and devaluation of the dollar

-Increase the supply of semiconductors

Answer: I don’t think so

IMO, the FED has to stop the money printing and raise short terms rates a little just so it has “something” to fight the next recession.

If they were serious about inflation, they would make it a policy to have interest rates above the CPI. Always.

Anyway,

In conclusion, 3 hikes (max)

and all this may create buying opportunities for some IG issues

Fingers crossed.

Stay safe,

Cheers

interesting comment on interest rates and fed,https://www.cfr.org/blog/fed-should-peg-rates-reality-not-its-stale-forecasts

Nice.

Thanks for the link.

That is along what I’m thinking and trying to say.

To take the conversation further, the world has changed, economies have changed, but the federal reserve has not.

i hear you Pickle! BOA says 7 hikes, GS and Deutsche Bank say 5, most others say 4. I don’t think the analysts are nuts, though. But i hope you are right about this possibly creating some buying opportunities for us.

Fingers crossed.

Hey, if we can get something out of this crazy mess, I’ll take it.

Stay safe

cheers

Are there any investors on this forum that are buying low interest rate coupon issues that are investment grade at par value? Just curious who buys low rate coupon issues at par value that are investment grade when inflation is over seven percent. It appears US Bank thinks there is a market for low rate coupon issues in February 2022 after watching all the carnage in January 2022 for low coupon rate issues. Are these preferred stocks etfs who are buying the large supply of low rate coupon investment grade issues at par value issued by US Bank, Bof A. Chase, Wells, etc.

What is the fair yield for IG bank, quality REIT, etc… preferred today? The market seems to be telling us 4.5-4.75% as I type this.

Which may reflect their beliefs that any interest rate rise might not last for any length of time? In a few short years we might again have rates as low as we did just last year. One recession away from a IG 4% selling at par or above. Not sure. Just thinking out loud.

For the record I own some bank preferred/bank trust preferred paying from 4.5 to 6.5%. Nothing below that though when it comes to banks. I have to accept some lower yields for reduced risk. I cannot just buy all high yielding junk. On the other hand I do not need to spend the income yet. So any interest/dividends will simply go to buy higher yielding stuff as time goes on. Fresh cash will buy higher yielding stuff. All the while life goes on and the money is working for me as I sleep.

Follow, This may be a double post, as apparently I am drunk and created a second account under the name “fc” for some unknown reason, lol.

So I wont repeat his thoughts, but no I am not.

That is why I bought BBB+ bank CBKPP at $102.65 the other day. Why get a 4.75% fixed, when I can snag 6% for 3 quarters then get 4.56% plus Libor this fall if not redeemed. It at least protects the backside to some degree.

BTW, US Bank doesnt have to worry about whether the market has any interest in a low coupon issuance. The market makers eat the loss on any IPO misfires.

Not the market makers, Grid, at least not initially… It’s the IPO underwriters, the investment bankers, who eat the losses. That’s one reason why so many issues are priced to be able to trade at an expected initial slight price premium, making the odds for flippers well worth the risks in general (says he who’s not a flipper generally)

Yes, thanks you are 100% right. I dont know why I said market makers. Underwriters send IPOs to the market. Market makers have zero to do with it.

I raised a lot of cash in November when they announced 6.5% inflation. I have started buying back IG quality names that are poking over 5% and at or below par. If I’m wrong, I can live with 5+ pct reduced risk issues. If very wrong, I’ll average down. And if it gets dicey, I’ll short some lower yield issues if I need to hedge.

I would avoid these low yielding preferred issues despite being high grade like the plague. I expect at some point perhaps sooner than we think yields for these types of issues will go back to historical norms of 5%-6% and higher.

Yep, fully agree with you Larry. I suspect that there are still lots of investors out there that truly don’t understand how these things work. Then throw in the “RAVAGES of INFLATION” of say 7%+++ and you have the makings for lots of sad faces on those that buy these low coupons in this environment. And anyone that thinks this inflation is just “transitory” is also delusional. Very Large numbers of workers are demanding much higher wages or they will go elsewhere. Employers are being forced to pay much higher wages and that will not change. I won’t even look at a new issue now under 5.5%. Especially since Iam not a flipper.

This will probably trade at $24 very quickly.

With current low coupon USB preferreds dropping like a rock, would the underwriters consider scrapping this IPO? Or is it already a given that it will trade?