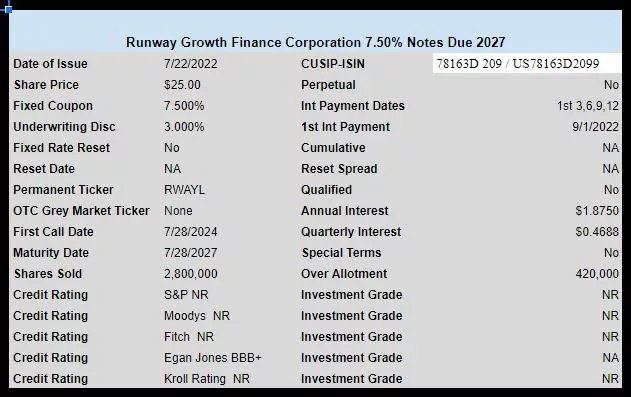

Business development company Runway Growth Finance Corporation (RWAY) has priced the previously announced notes with a coupon of 7.50%.

The issue has an early call date in 2024 with the final maturity in July 2027.

The company is selling 2.8 million shares with another 420,000 available for over allotment.

The permanent ticker will be RWAYL when the issue begins to trade in the next week or so. Being debt the issue will not trade OTC.

The pricing term sheet can be found here.

Bought at 25.00

You did better than me – perils of getting a late start to the day. Bought some RWAYL at 25.10

Tim,

While not comfortable with this issue (I have no idea what they do), I agree with your assessment in a prior post that some small banks are looking reasonable as we gain appreciation that this bear market thus far does not have the parameters of the 2008 GFC.

I picked up a couple hundred CCNEP this week at 7.125% coupon/7% yield/6.28% YTC.

While the HTLFP Heartland issue (Kroll BBB- at time of issuance) at your goal 2% lower ($25.20-$25.25 entry range) has a suitable coupon and yield, the elevated potential for a 7/25 call would leave one with a ~5.66% YTC? If I’m calculating that correctly, it still beats most upper junk ’25 senior debt – and this is a zone I’m looking to fill.

I’m trying to be judicious on entries but my “nibbles” are becoming “bites,” as I have a ton of ’23 & ’24 expiring senior debt along with 18% cash. One of the advantages of short-term senior debt at this time is that you not only have coupon income, but guaranteed cash coming available in the short-term, in case the market actually bottoms a year or two from now (or trends at this level).

Meanwhile the yields on BB’s and PFD’s are juicy. We’ve been traipsing through the desert looking for water – now we have 6-8% in quality holdings. While it’s all relative to inflation, I strongly prefer today’s scenario. I’ve got a GS bond I purchased on July 25 2017 that matures next month that has a YTM of 2.698! And I was happy to get it. That’s how it was in the good ole days.

As always thank you for your hard work.

I’ve got some good news for you, Fredson – YTC 7/25/25 on HTLFP purchased today at 25.25 would be around 6.70%, not 5.56%… Assuming QOL is accurate, qualified dividend with +6.675 over 5 year Treas for a reset looks pretty nice….would reset today at 9.52%. That seemingly gives you a good cushion for price stability on a perpetual if that’s a good thing to you… Will have to look into this one…..

2WR, you need to ignore the landscaping work outside today and do some stock research instead in the cold AC. Your too old for this type of heat! Last couple weeks have been very good trading wise. I even bought some of your old friend TVE at its lows yesterday, probably wont hold it long though…When is your forever misstress love CUBI going to announce our floating preferred divi?

Ha! Tell that to the weeds in our gardens… They don’t listen to me and tend to talk back when I ignore them…… And the problem with my doing stock research is you have to have confidence to act on what you discover. I tend to be my own worst enemy on that front…

TVE, huh? Wow, I’d never think you’d have that on your radar screen even for trading purposes. I keep watching both TVE and TVC occasionally thinking about how there must be a way to think of them as a completely riskless way of arb-ing away my existing 2 1/4% mortgage in a set it and forget it way without actually paying it off, but then I never do it… But as flip candidates, I wouldn’t think they’d be that great even in your instant flippability mind… In my personal set it and forgot about it universe, I still own GJO that I’ve owned since 2016, even though I know it’s held up so well over the years that it was trading way out of line high vs better yields available elsewhere and also having flipped from trading far cheaper than its underlying Wal-mart bond to far higher.. When you sit around with high percentages of cash on hand as I do most of the time, it does cloud your mind when you think about selling… That’s why I like story situations that allow for one decision strategies that hopefully lead to decent returns. I’m too mentally lazy to want to be obligated to generate as many right trade decisions as you make so successfully…. When you’re good at what you do as you are, no question yours is the better performing strategy but it’s too proactive for me these days… Now if you’ll excuse me, my weeds are calling..

Arb that mortgage away. That TVA dam is in your state. You can literally drive to it and “closely monitor your investment”, ha. It went up 20 cents already in one day at my purchase of $22.18, its close to the “small ball sell” point already….Make sure Mrs. 2WR hoses you down every 10 min so you dont overheat!

Drive to it???? Heck Sara Palin and I can see it from my back yard! Yup, Watts Bar Dam is within site from my perch on the River… And just so you don’t think I never do it, I played TINY ball yesterday as opposed to your small ball using called bond INSW-A. On Thursday somebody decided to bid more than what I believe I’ll get in total when called on Aug 5. So he got mine at 25.26 average and then I bot them all back at 25.17. Yup, I SCORED for all of 9¢, but that means in one week I made what I expected to be able make in a month and got to re-up to do it again for nearly the same price and probably better annualized yield than I got last week.. To me I consider these called bond situations essentially riskless with yields no less than 3 times what I’d get in money markets so it’s a way to do essentially something positive while while wielding my rake and garden knife outside..

2whiteroses – Yep, I miscalculated off the listed YTW. My bad. Thanks.

It puzzles me to see well-managed small banks, who survive by thriftiness, putting out 7.00% coupons. Even more with a reset like this. Obviously there are many inputs, one of which on this issue may have been the post-Mar 2020 issuance (6/19/20).

Fredson–yes around 5.70% today at $25.72 close. The reset certainly will trigger a call in 3 years—of course who knows for absolute certainty.

I am resisting larger ‘bites’ but I too feel the pull to get the money to work.