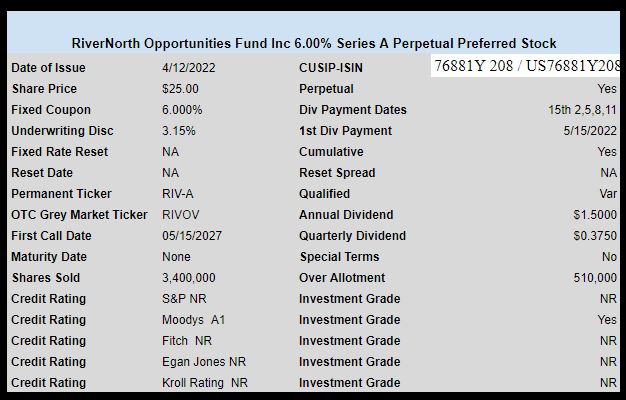

CEF Rivernorth Opportunities Fund (RIV) has priced their previously announced perpetual preferred stock.

The issue prices at 6.00% and is rated A1 by Moodys–investment grade.

The issue is cumulative and perpetual.

This is a solid coupon on an A1 offering, although being perpetual the share price will move with interest rates.

The issue will trade soon on the OTC under ticker RIVOV.

The pricing term sheet can be read here.

If you prefer was right on this one.

I bought 400 shares at Ameritrade last week, no problem. Today I tried to buy

more and got the rule violation message! What gives. I spoke to someone

there and they told me it was added to the list!

Norm

My observation Norman is these issues that trade with temporary tickers are put on that list. Until they get permanent ticker that aligns with company that reports their financials. Its the brainless system they have that shuts a lot of us out of the premarket IPO issues now.

And now they are 23.58.

RIVOP just traded @ 23.80 . . . thinking that flipping new preferred issues is not such a great strategy these days . . .

I did buy some in mid $24s thinking it was a good deal and a flip candidate!

Perhaps it is not just the rates going higher but more the fear of what the Fed Taper could do to the market starting June? Perhaps the big institutional holders are selling their low coupon IG preferred and ignoring 6%+ yield in likes of RIVOP trading below par in the hope using the proceeds to buy ‘better’ stuff as Fed balance sheet starts selling ?

Symbol seems to have changed from RIVOV to RIVOP.

Fidelity cancelled my prior order as RIVOV, shows the quote for RIVOP but refusing allow to place a buy order. Schwab wants $6.95 trade commission for it!

TD wants a commission, too (stating the obvious). I think I’ll wait and see where it trades when/if it gets on a no-fee exchange.

The way things are going, it will most likely be available at a lower price.

JMO

I show it on the grey market thus I cannot even buy it at Ally. Maybe if I call but I am way to lazy. Just wait a few more days and it does seem to be drifting down every so slowly.

Camroc, Im already out with a $20 profit on 200 shares. Maybe I should ask 2WR, to annualize that return for me, ha.

Hey, you pickin’ on me, Grid, old buddy, cuz I’m usually unwilling to do what you’re so successfully doing time and again and again and again?????? haha…..Nice flip! Yeah, I get it. Active trading/flipping ought easily be capable of enhancing returns vs my belt and suspenders kind of lo risk lo return crap….. I also get the irony of how my professional background ought to have me doing exactly your thing right along side you, but I just can’t get there from here anymore………. ha. Maybe I should write a book – “How Not To Maximize Performance in Risk Markets”……..guaranteed not to be a best seller…. Guess what? I own RIV itself, and have for 5 years…. It’s been a modest winner over the long haul and probably would have been even better had I DRIP’d, and probably even better still had I looked to take advantage of extreme highs and/or lows…

Ha, no I was teasing you another way. You have shown in the past to be patient and deliberate enough to tally up annualized returns with buying issues about to be called. I really had no purpose nor did it serve a purpose in me buying this. I was bored I think and just wanted to see if I could buy it. Personally I agree with a few others and think I can get a chance at it lower still. I just took the nickel trade money back and stored it with the quarters of free cash laying around waiting to strike. And for what I really want to sink my teeth into there has to be a lot more sinking going on. But while I wait I buy a few hundred and sell a few hundred each day as a few of these issues do still move around a bit for a burger or two profit.

By the way my I luv CUBI pin has been ordered since I own CUBI-E and will wear daily like you! 🙂

haha… Remember the old southern rock band, Wet Willie? You gotta keep on smilin’ …. lol.. just teasing back…….. but my own personal “I luv CUBI” pin is a bit tarnished this year as I’m a stockholder as well as a CUBI-E holder… Mr. Market never seems to give CUBI and the Sidhu’s any respect for some reason when the trend for banks is down and the common has been decimated far beyond anything rational….. Sidhus’s have been conservative in projections year after year for the time I’ve been involved and yet Mr. Market never believes them… The low end of their projections for this year has always been $4.75 for base earnings and yet it trades at 9 1/2 PE for that number… However, all this has just made me look for the tarnish cleaner not turn in my pin…

Ha! They came out saying 50mm at 6….and it sat there all day. Filled at like 85mm. I liked the deal BUT there is plenty on the books at 6% current yield and steep price erosion. In other words there is a buyers strike. And plenty of damage across most positions. …….Took a strong conviction to hit this one!

And OPP A and B started tanking shortly after this was announced. Last I checked the current yield on them wasn’t even 6.

I see it at 24.90 by 25 today. This will be low 24’s in short order. No much on screens that isn’t down 15-23%

There are a pocket of them but its the usual suspects…Above market yields (which are getting less) with decent quality, high adjustable floaters, and term dated… This is where I have been mostly squatting for past 4-6 months. But some of these (like CEQP- which I own) can only hold out for so long until any further yield upsurge and or scare continue the assault….And for me mostly, its still too early in the game to rotate into the ones that have been taken to the woodshed already.

Yes, that’s the very reason I traded 3/4 of my overloaded CEQP- position last week for CEQP, which announced a 5% distribution raise this quarter. Lost a little income on the front end but now I’m more tax-deferred than ever. Oh, and did I mention the 5% raise? lol

So. Hydrocarbons ain’t goin’ away anytime soon. Energy energy energy is all I see right now. Even the moribund coal industry has come alive like a zombie apocalypse because of the Ukraine and Green debacles.

JMO

Lots of volatility in in RIVOP. Picked some up for $23 this morning, and its back up to $24.72 as I write this. Crazy times.

I did manage to buy some at Schwab when it was RIVOV last week but cannot buy any more! I do have orders out where it shows last trade but no bid/ask!

Which broker were you able to buy RIVOP today?

schwab. Placed the order from schwab.com. couldn’t get it in streetsmart edge.

Wow, congrats on $23. I think it’s very hard to go wrong at that price..

The thing with CEF Preferreds, they aren’t companies, more like a bag of stocks that can be liquidated to cash in an instant.. with safeguards to protect you. Eg 200% asset coverage. No major need to worry about defaults during periods of market stress or idiosyncratic company issues. Truly a sleep at night strategy if you can withstand mark to market vol and rate risk.

Here’s hoping I get a chance at those levels…

This is a bonkers coupon for an A1 rated issue. Only about 70bps tight of PSEC-A lol

Exactly, this will be a gift.

Looking at the comments, some don’t understand the liquidity of the holding or the 200% asset coverage requirement.

On the other hand, PSEC holds a bag of ….

Just eyeballing things, 6% if present rate hike bake ins dont go higher, this is a reasonable issuance price. It has A1 rating but it isnt a “name” issue and there is a small ding there, plus IPO’ing into this market is tough. One can debate the superior quality to the following jr. debt issues but they are names with a history so that helps their cause. CMSD is basically 6% now as it spits out its interest payment in a month. MER-K is 6.2% though past call and a buck above par still. So I personally dont see RIVOV as a steal or a bad buy if one is looking for perpetuals now. Of course if rates revert backward, it definitely could appreciate with the call protection if credit spreads dont blow out.

Ok, I’ll bite. Why won’t MER-k be called anytime soon? And when does it float?

Agree 100% on the name recognition part, that should make this trade about 40 bps wide of gabelli’s.

At the end of the day, I sleep a lot better with a CEF preferred than a single name company preferred unless it’s a company like Berkshire. I think there is a zero chance of riv defaulting, and a much higher chance of BofA or a Ute defaulting, although it’s still in the less than 1% category. My personal background also has experience with CEFs, including being a RIV shareholder ages ago, and I am less knowledgeable about utes, so I’m sure that plays into it.

Maine, Heck I think the question should be why wasnt it called years ago as it has been callable for 11 years. In fact it dropped out of Tier 1 capital if I understand correctly converted in 2018 from a Merrill Lynch issue (owned by BoA) to a BA subordinated debt. It doesnt float until 2066 if my memory serves me, and then at Libor plus something like 1.7%. I wouldnt want to be alive for that, and I doubt I will if I am lucky. This serves me as a nice trading vehicle, and recent drop has got me back in for zillionth time. But it beats me why they never have, although now, I doubt it serves any purpose to with rates what they are now.

I think you answered the question better than I could. Its a choice not a right or wrong issue. And definitely a comfort zone thing. My knowledge on CEF’s borders yours on utes, maybe less, ha.

BofA is too big to fail but they don’t have to default to suspend preferred divs (which are non-cum). All that has to happen is they fail their stress test and regulators tell them to stop preferred divs to strengthen their balance sheet. Unlikely they do that but the decision will be out of BoA’s hands at that point.

True, but remember in this specific case being referenced that is not relevant as MER-K is trust debt. It is deferrable interest and would be repaid unlike their traditional preferreds…Except for BACRP which is a cumulative preferred issued long ago. .

Buy as the coming recession hits a nice low on price, if at all.

Wait – the firm had $336M of assets as of Jan 31 (probably lower now) and is floating $85M (before the green shoe; maybe $95 with it) preferred?? Not saying it’s unsafe but seems a bit aggressive no?

Trading on Schwab

As Timdman mentioned earlier its up at TD. Im not under any illusions buying a perpetual now, but I toed in 200 shares at $24.85 this morning.

Hmmm. TD just cancelled my order. “no market”

Camroc, Are you trying to buy through Think or Swim? That platform is just now loading new IPOs issued from the Reagan administration. Put your order through the regular website. I just put a fake order in to buy more for $24 and it took it, so its still working.

Nope. Regular website order. Took about 3 minutes to cancel it. I’ll try again. I’m using RIVOV

Very odd, that was ticker I used….Are you low balling bid? That may reject it. I saw last trade was $24.85, when I bought so I entered that and it hit about 5 minutes later….I didnt leave the fake $24 bid out but only for a minute then cancelled it.

Screw it. Bought a coal company an hour or so ago. Now up over 11%. I’ll take that instead. 😉

JMO

Grid:

Just have to hope this preferred from the Rivernorth closed-end fund folks performs better than OPP+A and OPP+B, which were issued at lower rates and have course been slammed in 2022.

Didn’t think buying a preferred from a now leveraged CEF “fund of funds” was up your alley? Is this just a short-term trade for you?

For RIV to pay a near 13% distribution yield to its holders, it is forced to buy leveraged CEF funds. So you are essentially adding leverage on top of leverage, but at least RIV’s borrowing costs are now fixed at 6% instead of floating.

My guess is most of the CEFs RIV has holdings in all have floating rate debt. If rates keep rising to previously unthinkable levels, the leveraged CEF sector is going to be a bloodbath with falling NAVs, rising debt costs, and large dividend cuts.

Not sure how this will affect these fixed rate CEF preferreds, but my guess is it won’t be good.

Good luck to all.

Rob, I have around 25 different preferreds and this is the smallest issue I own. So Im not digging in here. OPP-A was issued as a 4.25%. Its getting what it deserves from long end jumping 4X since it was issued. Its still too high in my opinion. I do own another of this sector ilk RMPL-. Own quite a bit of it and have traded it frequently within its narrow range. Been very pleased with it for the 6-8 months I have been in it. Of course its a short rope past call term dated issue.

hey grid I dumped my RMPL- in anticipation of hikes. Then it went back up so you win this round.

Hey Martin, to be honest I see last trade was 25.72 yesterday. I would have been a seller there but been golfing past couple days so I wasnt checking. Actually for me, rates rising and anticipation there of is why I finally started being a player here. These types will stay near par, just because there is no duration risk. Im in several of these hide out spots.

though you were supposed to do business deals on the golf course.

Grid – Understood on your rationale behend RMPL. I’m noticing that some of these longer duration CEF preferreds can get hit hard – even those with higher yields.

Check out 6.75% ECC+D, a preferred from 30% leveraged closed end fund ECC. Just hammered lately and that thing pays a monthly dividend.

Be careful out there.

Rob, I will leave the rest of the levered world for you, lol. Im hanging in there up 2% or a bit more, nothing special. Being out of the bad trend sectors has helped me stay positive and muddle along. If I can return my market coupon yield this year, I will be thrilled. Historically for me that would be pitiful, but we havent been in this type of cycle (high inflation, low yield, with Fed tightening).

My biggest concern for me is CNIGP, as its getting 2 months out from the show down at the OK Corral.

Grid:

Definitely getting tougher to make a buck out there. Personally been doing much more hit-and-run dividend capture in 2022.

Perfect example is RILYM. Got the interest payment today and now are selling most of the shares I bought below $25 in March at $25+. But these opportunities are fewer and far between this year.

I’m at a 35% cash level. Never been anywhere near this number in the past. A very challenging environment every day out there in the income space trenches!

Hey Rob;

I have a little bit more of RILYM than I should, but I am hanging on to it until it matures in Feb 2025. Question, if RILY chose to be rated by S&P or Moody’s, what would be your guess as to the rating it would get ? RILY has a lot of debt, but they take in a ton of money too. Maybe BB- ?

Bill:

I’m only selling some of my RILYM in the hopes of buying it back again below $25. I have 90 days and two important Fed meetings to see if it happens.

S&P rates securities issued by a rock solid bank like First Republic (FRC) at BBB-; that would likely be a very generous rating for highly-leveraged RILY.

I made a boatload on RIV divs, but as the Steve Miller Band might say, I took the money and ran…