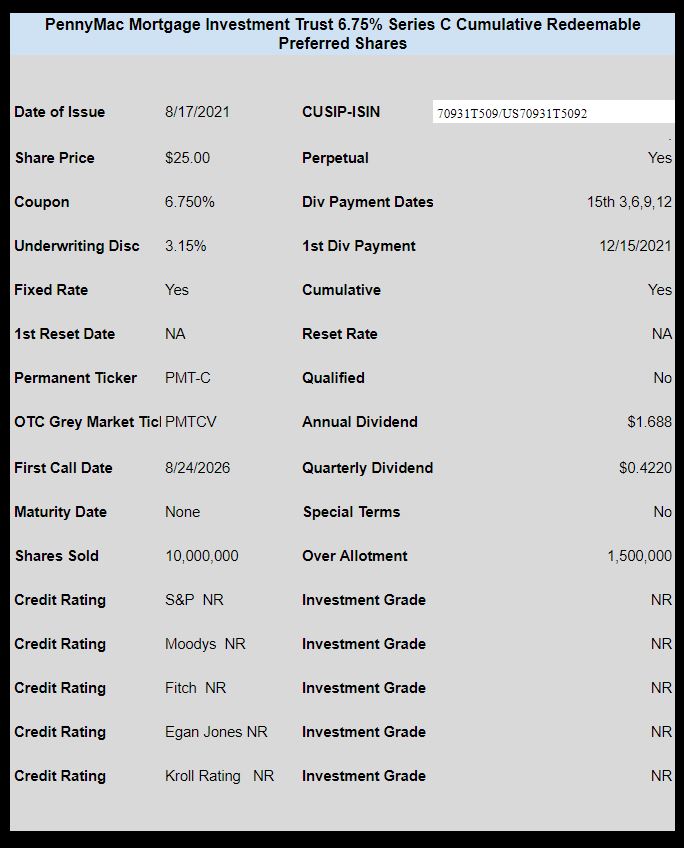

mREIT PennyMac Mortgage Investment Trust (PMT) has priced the previously announced preferred stock issue.

The issue prices at a fixed rate of 6.75% for 10 million shares (plus another 1.5 million for over allotment).

The proceeds will be used for general corporate purposes.

The issue trades immediately under OTC grey market ticker PMTCV, but look for this ticker to change before the week is out.

The pricing term sheet can be found here.

Did anybody buy PMTCV at Fidelity? I did, then it was taken away when the symbol changed. Now listed as a purchase under a weird alphanumeric, no money taken just says (when issued stock). Can anyone explain? The price has gone up 30 cents, did I lose it?

I’ll call the rep tomorrow but I’m assuming somebody here knows more than the phone reps.

Hi, Martin. I bought some. Seems the change to using preliminary “xxxV” labels has caused these changes. I haven’t talked to Fidelity myself, but this has occurred with prior purchases made with the “xxxV” label; in my account they sit up with the bonds, etc. (arranged by CUSIP, not name), for a few days, then find their way to one’s alphabetical list, with accurate purchase price. In the meantime, they don’t show purchase price, even in one’s “history.”

In fact, I subsequently bought some more after label changed to PMTCP, and as of today those shares sit down with my PMTPRA/B, with price, cost basis, etc., while the original PMTCV shares are still up top with only info being # of shares.

Hope that helps.

Thanks, that works as long as I get my original purchase price. I did spend the available funds elsewhere and it’s an IRA not a margin account. Maybe I need to sell something Monday morning so I have the available funds.

Ooooh, that may be another issue you’d need to check on–no idea how they’d handle that.

The new “improved” system of changing pink sheet ticker symbols on new issues is causing chaos at several brokerages. The standard that I think I am seeing is for the brokerage to NOT deduct the purchase amount from your cash balance until the second or third ticker has been assigned. They do this as long as the ticker is labeled “when issued.” I have seen several cases where you thought you had a positive cash balance and then one day when the ticker changes, you have a negative cash balance aka margin debt. And yes, that has occurred in IRA accounts where you are not allowed to have margin, so it is a problem. After I got the first margin call, I started paying closer attention. In theory the brokerage would do a forced liquidation in an IRA account or one without margin in a taxable account.

The solution is for you to keep close track of your cash balance AND deduct any pink sheet buys, even if the brokerage does not.

I bought a previous issue at an IRA Fido account with a xxxV ticker. They didn’t take the cash out and did not reduce my available cash for other trades. As a result, I made other purchases and basically overdrew the account which you legally can NOT do on an IRA. They cancelled half of my xxxV trade, and charged me some sort of $35 fee. I called to question. They had no clue what was going on. It was not worth my time to explain to them so I let it go in the hopes that someone else will educate them in the future. My plan is to not overdraft again.

Now PMTCP until PMT-C

I picked up a few of these from $24.61-$24.64 this morning…

I remember that PMT-A took a shocking (and painful) dive when covid hit. Too risky for me to try again.

Every McReit did.

And why shouldn’t it have? Yields were falling like rocks in feb 2020, some 10 trillion at negative yields. US Treasuries were the highest yielding sovereign. And gnma’s were more then 50 BP over that! Besides….Opec was in price war. Buying ginnies on margin (can be 25-1) was a smart bet! But……………….

Then….people wondered if we’d see 2008-9 mortgage disasters all over again. After all who would pay their mortgage in a pandemic? GNMA’s went from 1.02 to .8- in a weekend. Margin calls around the world. Everything collapsed, with weakest hit hardest.

McReits moved from 26-27 to 5 or lower in 3 days. Add in many desks mandating trading restrictions (for the sake of Best Interest) and it was a very difficult test. So yes buying them takes special conviction!!

I’ve seen this term “McREIT” used before….. How do you define what it means? A quick google search didn’t help much… “retail and restaurant REITs” maybe?

https://www.barrons.com/search?keyword=nly&mod=DNH_S

Annaly is one of the biggest.

It’s an investment fund deemed to be a REIT that invests primarily in mortgages. Be it commercial mortgages, ginnie fannie or freddie macs or anything to ‘do’ with mortgage financing, it fits the bill. I tried to get one firm to describe their mcreit business and they wouldn’t! The things are as opaque as it gets. Analyzing them is next to impossible!

That sounds to me as if mREIT and McREIT are synonymous……

Google it- 6 yrs ago talk of it was about McDonalds spinning off property into a REIT. Lots of articles.

Just wanted to add remember;

In 2 years and 7 months, A shares drop to 5.8% + 3 month LIBOR

In 2 years and 10 months, B shares drop to 5.99% + 3 month LIBOR

This is a large issue. My take is that much of this issue was sold to retail clients by brokers rather than requested and bought by institutional accounts. It is not surprising that this deal broke issue price — there is a lot of loose stock.

As an academic exercise, I would prefer to own this issue below $25 vs. the outstanding issues.

I’m showing last price $24.80 with volume of 192,000 shares.

At first glance, I was going to grab these but now realize they are not retiring any of the 8%ers.

Also the latest ER saw a significant miss on revenue (-78% Y/Y) but book value of the stock held up surprisingly well.

Lastly I read some trader chatter of a possible giant stock shelf offering but I’m not clear if it was just daytraders confused about the preferred. Have to dig into the PMT filings.

The 8.125% one ( if ignoring the float later) has a YTC of 6.11% using the low of today = 26.19 – so maybe the new one is better?