Once again the S&P500 rose–as it does most every week, as money sloshes all around the globe. The index rose 1.4% last week.

The 10 year treasury continued to drift lower even as inflation gauges run hot and various other economic measures, such as retail sales, boom. The 10 year started last week at 1.68% and ended the week at 1.57%. The fall in rates occurred as investors are buying the line from the Fed that economic gauges are ‘transitory’.

The Fed balance sheet rose by a huge $85 billion last week–now at about $7.8 trillion.

The average $25/share preferred stock and baby bond rose by 8 cents last week. Modest gains were found across the board. Investment grade issues rose 6 cents with banks and mREIT issues rising 3 cents.

Last week we had 2 new income issues announced.

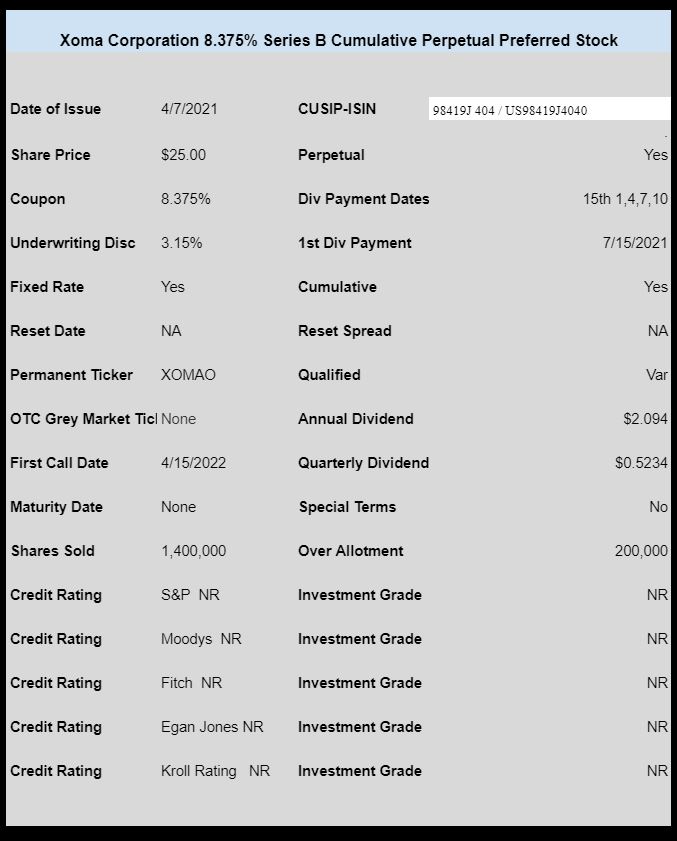

XOMA Corporation announced a new issue of high yield preferred. The issue is trading now on the NASDAQ under ticker XOMAO and closed last week at $24.77.

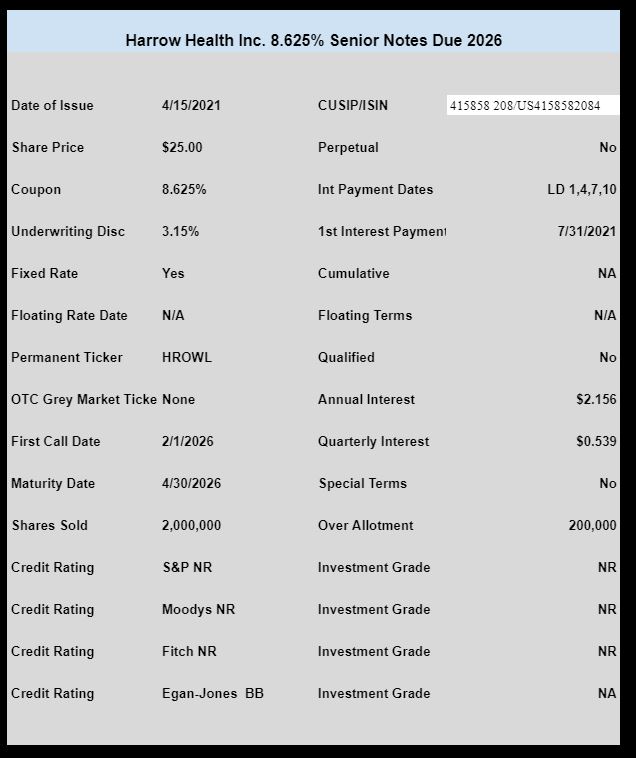

Little eye health company Harrow Health (HROW) sold a new issue of high yield baby bonds with a maturity date in 2026. The issue has not yet traded, but likely will in the next week or 10 days.

Perhaps it IS relevant to hear a contrary voice. I know our behavior has been conditioned to just stay nice. I hope this is appropriate for a site like this as it is focused on maintenance of income.

I just did a look at Canadian IG 5 resets that are due in 2021. The American market is no better. Looks like there are going to be a lot of instruments available to the public disappear onto private ledgers this year. Keep scratching around for flips and divy capture, but it never lasts long as a wealth maintaining INVESTMENT strategy.

At the beginning on my process here at III, I blogged about laddering and neutral risk control and now see that these tools of purpose are warped into a negative state of the active and accepted degradation by current policy. THIS is WORSE than stagflation with LOWER income and rising prices, as well as no social networks except a couple of payola checks being the policy. At least the bond rates went UP in a market fashion mechanism in the 70’s. As far as I can see, The American Market has died.

Be careful, very careful here. People tend to think tomorrow will look like the recent past. No predictions as to when the wheels fall off, but this makes NO sense to me…but I’ve only been IN forty years. This has happened in this country before, perhaps too far back for memory, but not beyond the prudent study of effects elicited on the common man.

You are correct and this wonderful web page has been very silent.

In the U.S., the regulations imposed onto the financial markets were much worse than for individual investors than for institutions.

Let us say, a $100 million junk bond is floated. If it is sold to the public , the SEC regulations cost 1% per year to adhere to. If that is sold to private investors, there is little cost to adherence because this a private transaction to “sophisticated” investors. The 144 rule.

So most bonds are sold privately now because it is cheaper. The public CANNOT buy these. This only leaves very high risk securities to the public, like prison bonds or companies that are losing money. The regs have hurt individuals much more, as institutions, probably with lower profit margins can still participate in all markets while the individual investors are cut out from large swaths of securities.

CFO’s will always go with their cheapest options currently, even though down the road, if trouble occurs with the “private” securities , liquidity in the private market is generally poor and bid/ask spreads can be anywhere from 3-10%. There have been lawsuits with private pensions that wanted to sell some securities and bid/ ask spread was up to 10%, wiping all their profits on the security.

So if one wishes decent income , one has to go into very illiquid securities or dividend stocks which generally are at the mercy of volatile public . Preferreds are not much different.

Nothing wrong with this post Joe

Joel—There is a very decent possibility that the GOP will take control of one of the houses of Congress in 2022. If only because that is the historical norm for off-Presidential elections. If that happens, the current spending spree will probably stop until the Presidential election in 2024. IMHO, the problem lies not with either political party, but with the Fed.

As long as the Fed maintains the position that current inflation is temporary, nothing is going to change with their policy. Their twin goals are full employment and 2% inflation. They interpret inflation differently than you and I do. Otherwise government costs based on inflation (social security for example) would skyrocket. Unless the political party in power (either one) reins in the Fed, we will continue pushing the enormous financial problems down the road. Eventually, some crisis will trigger a financial meltdown. That could be tomorrow or five or ten years from now. All we, as small private investors, can do is re-act as best we can when the sh** hits the fan. We can’t stay in cash forever–at least I can’t.

Speaking of paying dividends again, has anyone heard anything about PG&E resuming dividends on their preferred shares? Still patiently waiting. It has appreciated nicely since I purchased it but resumption of dividends would be nice.

Hey, PB.. The official answer from PCG is… They dont know…That is what they put in last SEC financial filing this year. Bankruptcy judge cleared it as unimpaired, but someone told me they are being restricted until their tree cutting mandate is met to satisfaction of a separate judge from a different ruling. I have not researched that to see for myself though.

Its going to be several more years until a common is restored so it could drag out a while.

Don’t know if anyone out there had a chance to listen to the interview of Stephanie Pomboy this morning on Maria’s show but I found it extremely interesting. Hard for me to reconstruct it but she spoke about inflation definitely coming with all this massive printing of money . And when all this stimulus money comes to an end and inflation continues to rise higher and higher she sees a pretty hard selloff coming in our future. I have always considered her a pretty smart gal.

Yup. Saw the interview.

She made a lot of good connections with all this stimulus. And noted with all the good economic numbers the 10 year T still went down.

I have never seen her positive about the economy even before covid. She can pretty much depress a bride on her wedding day. However, she has been beating the drum on inflation and debt for a while now.

I dont recall what inflation number she referenced in this interview but when it hits 3%, 75% of the time we have a financial crisis.

Pickle, The beauty of it all is the Feds definition of inflation…Its not mine…If prices go up 4% a year for a couple years that is inflation. But if prices up 50% at once and stabilize there, that is not inflation.

Gridbird, that’s nonsense. You are purposely inflating the Fed willing to allow say a 3-4% one-time price rise off of last year’s low base with 50% price rise. Pretty immature argument.

Karma, take a cool drink of water and relax as you are completely missing the point. I will explain my point in a clearer manner and skip the obvious hyperbole for you….The common man views inflation as prices going up. Whether it be yearly or in one shot. The Fed doesnt. If there is a one time spike in price (you pick the number if it helps you) and then it sits at that price going forward that is not considered inflation.

Take a concrete example. The lumber spike. If its price increase sticks going forward with no additional price increases they do not view that as inflation. That is viewed as a transitory one off event. The common man would view that as inflation and would refer to it as such. That was the only point being made.

Gridbird, your argument is far from accurate. The point about transitory price spikes (or drops) in isolated parts of the economy is that you can’t attempt to control them with monetary policy. The jump in lumber is clearly going to contribute some to inflation numbers, but the point is the Fed can’t target lumber prices; it targets the overall price level. And even if the Fed could target lumber prices, it wouldn’t want to! There is every reason to believe that lumber prices will come back down since there are COVID-related supply shortages causing the rise in price. Is your view that the Fed should raise rates a bunch and try to crush the overall economy due to a few supply-constrained materials?

As for the common man, he has no understanding of inflation whatsoever. He thinks we have runaway inflation because gas is $3 a gallon; forgetting it was $4 in Summer 2008 (adjust for your local pricing). He also would guess that inflation has averaged 6-10% per year over the last 20 years, which could only be true if the U.S. was in a perpetual depression. So, yeah, I’m going to take exactly nothing of what the common man thinks about inflation into my worldview.

Karma, your thinking too hard on my post. You arent countering my points, because I wasnt making those points. I never said Fed should do anything. I was just saying the Feds view of inflation is different from what common man thinks it is. Nothing more. In fact your post confirms you agree with me on that.

Gridbird, but you imply the Fed’s view is inferior. As flawed as it might be, the common man’s view is so much worse.

Tough audience, Grid. You are going to have to go buy a PhD so you can have more deep, meaningful posts. 😉

Private, I would definitely have to buy it… That is certainly cheaper than a brain transplant to be able to earn it sitting in the classroom. 🙂

Grid, the certificate that you buy would also have to give you power to read and convert what others are writing into what they are really trying to say. And… every commentator has their own language 🙂

By the way, did he look like Al Bundy? Go Polk High Panthers!!

KC. I was just pondering the “common man.”

– Do we offend others by saying it in 3rd person? Meaning the rest of the world is common, but not I?

– Am i the common man?

– Financially speaking, does the common man refer to 99% of folks, and not the upper 1%? I still have another 1.4 mil to go according to the Night Frank Wealth Report.

– I was power washing my deck and retaining walls over the weekend, and flinging dead mice into the trash from some traps I had put down.

– Is the common woman included in the common man count?

I do however listen to what the common man investor is thinking because of the herd mentality among other things. If they think inflation is going up, I want to be ready for when they start selling their investments. And right now, the talking heads are telling the common investors what to think about inflation 🙂

Mr. C, is there any difference between a “common man” and “Joe 6 pack”? I ponder that because today I accepted there is a mortality to my life and went to lawyers office to get my will and such all set up. I told him I need a “Joe 6 pack” will set up with a beneficiary deed attached to it. He knew exactly what I needed and is getting it all set up now. After I paid the bill first of course. I wanted to do it now before inflation jacks up my costs, ha.

Just looked up what determines the 1% and I am solidly in the 99%.

There was this one year where I might have been in the 1%.

But, money can’t buy happiness.

“Just the other day my wife met me at the door in a sexy negligee,

Unfortunately, she was just coming home.”

“I told my wife the truth. I told her I was seeing a psychiatrist. Then she told me the truth: that she was seeing a psychiatrist, two plumbers, and a bartender.”

RIP Rodney.

I tried moving to Lake Wobegon a while back, but you have to be above average.

Canada, too, I think.

There was nobody better than Rodney. He gave bad taste class.

Yup.

Totally nuts.

Almost makes you think that they have lost control and they know it but dont think that we know they know it.

Coming soon: 4% is the new targeted 2% inflation goal. So there is still no inflation.

So according to PickleNick, she is always wrong but never in doubt. Wow, where do I sign up for more of her advice!

P.S. Eventually you guys will learn that nobody knows nothin’. Proceed accordingly.

Yeah, if you have been an equity / capital gain investor over the last 4 years and listened to her you would have left a lot of money on the table.

Her concern about debt is based on rising rates but they are not rising.

I don’t recall her making any investing suggestions other than gold.

Multiple point of view are good but maybe she is on just to fill some airtime between commercials.

That’s the successful formula for economic predictions. Keep saying the same thing and eventually you’ll have something to brag about when you are correct.

Tim—Hersha Hospitality has started paying dividends again, just received on April 15. Bought this at $9.00 on May 20,2020.

Thanks Jeff

It has you are right, but it’s been dropping every day. Shoulda sold a few weeks ago after the ex-date.