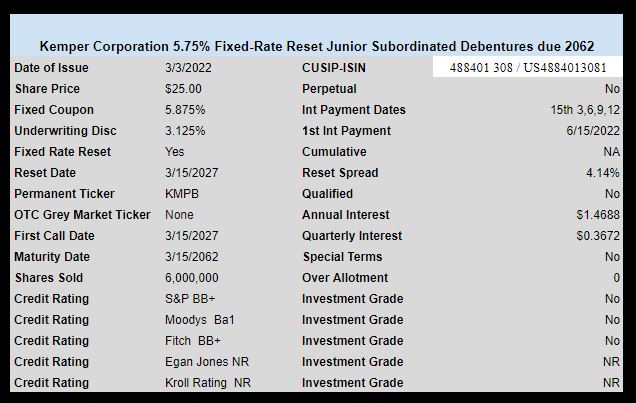

Insurance company Kemper Corporation (KMPR) has priced their previously announced new baby bond.

The issue prices at 5.875%. This is a fixed-rate reset issue so 5.875% will be paid until 3/15/2027 after which the coupon will be reset at the 5 year treasury rate plus a spread of 4.14%. The coupon will be reset every 5 years.

The maturity on this issue is way out in 2062.

There will be no OTC trading on this issue–so it will be a week or so before we see any trading under ticker KMPB.

The pricing term sheet can be found here.

I was quoted 23.85-24.10 YIKES!!! No prisoners!!!

I still own Kemper Bonds that went in default in the 90’s.

Do not buy.

Sorry to hear that Dan. Many of us owned these Kemper bonds that were sadly called about 3 years ago https://www.quantumonline.com/search.cfm?tickersymbol=KMPA*&sopt=symbol

What CUSIP are your bonds? Was there ever a settlement?

The cusip is 550060AA5

Name was Kemper-Lumberman

9.15% due 7-1-26

I believe the institutions got their money out of it but individual holders of the bond got zero. This was a case that I bought this bond through Morgan Stanley. $20,000 face amount. I tried to sell when the Bond reached 85. They would not accept a bid and I had to follow it the whole way down to zero. This was purchased on June 28, 2001.

That was a different Kemper.

Dan, I’m truly sorry to hear that Morgan Scamley failed you. I was on Wall Street for 24+ years after law school and retired about 5 years ago in my 40’s. Let me do some research on the defaulted bond when I get home and I will report back to you. Be well, Azure

http://www.lmcco.com/

NOTE: The “Kemper” trade name was sold to Unitrin, Inc. on June 29, 2010. Unitrin, Inc. is not affiliated with Lumbermens. Unitrin, Inc. has now changed its name to Kemper Corporation. If you have any questions about a Kemper personal auto or homeowners’ policy or claim, please contact Kemper directly at 877-252-7878 or at http://www.kemper.com.

Dan, this is my preliminary finding:

Lumbermens Mutual Casualty Company operates in property and casualty insurance business. The company was founded in 1912 and is based in Lake Zurich, Illinois. As of May 10, 2013, Lumbermens Mutual Casualty Company is in liquidation. CUSIP 550060AA5 9.15% due 7.1.26 are $400MM Subordinated Unsecured Surplus Notes and were offered 6.12.96 @ $99.72 yielding 9.18% and were non-rated. The bonds were junk bonds with little liquidity at their initial offering and at offering I see them as 144A (how did you buy them if they were offered restricted?). Unless, these bonds came off restriction at some point and then Morgan Scamley offered them to you. The bonds traded 3 separate times the last year and all trades were at 0.01 cent or less. Certainly, your broker should have informed you as to the initial risk and as they were losing value until they went into default.

I also found this press release from November 2003:

LONG GROVE, Ill. – Lumbermens Mutual Casualty Company has received a notice from the Director of the Illinois Department of Insurance denying the company’s request to make the December 1, 2003 interest payments on its 8.30 percent surplus notes due December 1, 2037 and its 8.45 percent surplus notes due December 1, 2097 as well as its January 1, 2004 interest payment due on its 9.15 percent surplus notes due July 1, 2026. This may help you https://www.osdchi.com/PDF%20Files/Scanned%20Orders/lumbermens/RevisedSURPLUSNOTESFREQUENTLYASKEDQUESTIONS.pdf

I truly am sorry for your loss, Azure

Thank you for your efforts!

Unfortunately I was an advisor at Morgan Stanley at the time. They allowed the bonds to be offered to retail clients. There was a small notification about the 144 rule which was vague and short however it did not preclude the bond desk from allowing individuals to purchase the bonds. We knew they were somewhat risky, what we didn’t understand was that they could stop taking bids at any time. When the bond started to drop.. got under $.90 on the dollar, we attempted to sell. The bonds continued a decline however they would not accept any bids..I literally watched the bonds melt in price down to zero. Even though, Morgan Stanley showed their value on paper higher than what I was willing to sell for ..I could not file a complaint with regulatory authorities for fear of being fired.. My complaints within the company fell on deaf ears. It was one of the reasons why I left the firm.

Luckily, I only had a few positions in the bond and nobody had more than two or 3% of their portfolio invested in it. The bond should never have been offered to retail advisors or clients. I didn’t understand how the firm could just simply stop accepting offers to sell the positions. My thoughts were that the firm bought the bonds, realized they were going into default, sold them to retail clients, and then refused to accept the bonds back at any price.

No one will ever convince me otherwise. Pure and simple this was the worst thing a firm could do to its clients.

Thank you for your efforts!

Unfortunately I was an advisor at Morgan Scamly at the time. They allow the bonds to be offered to retail clients. There was a notification about the 144 rule, however it did not preclude the bond desk from allowing individuals to purchase the bonds. We knew they were somewhat risky, what we didn’t understand was that they could stop taking bids at any time. When the bond started to drop.. got under $.90 on the dollar, we attempted to sell. The bonds continued a decline however they would not accept any bids..I literally watched the bonds melt in price down to zero. Even though, Morgan Scamley showed their value on paper higher than what I was willing to pay. I could not file a complaint with regulatory authorities for fear of being fired.. My complaints within the company fell on deaf ears. It was one of the reasons why I left the firm.

Luckily, I only had a few positions in the bond and nobody had more than two or 3% of their portfolio invested in it. The bond should never have been offered to retail advisors or clients. I didn’t understand how the firm could just simply stop accepting offers to sell the positions. My thoughts were that the firm bought the bonds, realized they were going into default, sold them to retail clients, and then refused to accept the bonds back at any price.

No one will ever convince me otherwise. Pure and simple this was the worst thing a firm could do to its clients.

Ouch, I truly am sorry for your loss and Morgan Scamly should have been investigated for this fraud by the SEC. Horrid…This is EXACTLY why I went to law school, but that’s a story for another day 🍀

Dan, i’ve been considering using morgan stanley financial advisors for part of my portfolio (not preferreds). in your opinion do u think this is a bad move? curious because you used to work there (and also called it morgan scamly , lol) thaks

All firms have good and (bad) advisors. The integrity of the firm itself does tend to change over time. There were many other, some even more egregious, reasons why I personally would never do business with them again. I’m sure all the major wirehouses and banks have done things that were shameful.

If I were more skillful at writing I could write a book on the underhanded antics of the two major wirehouses I worked for 26 years before I went independent in 2009.

Anybody remember the “ Deam Winter”High Yield Securities Fund and how about the early redemption of JP Mirgan STRATS? So many unfair things done to individual investors.

It’s a 3 billion dollar market cap and has been around for a long time. I have no idea about their viability but there are certainly more opaque, less credit worth names out there. I’ve been running lists based on coupons and there are maybe a few dozen 25 dollar pfds that are better priced. And that’s where I always start / by asking what else could we buy.

One things for sure, the market has changed. 4 months ago this would have been 3X the size and they’d be fighting for allocations in minutes. This one only did 150mm and hung around.

On the common stock of Kemper, it is a strong sell by Schwab, CFRA, and Zacks. Since 2019, common has dropped from around $91 to $51. This company has really been performing badly over the last 2-3 years. Credit rating may be okay but the common is a falling knife.

This with the very long duration isn’t so hot.