We all know that the ‘reward’ from preferred stocks and baby bonds is all about the level of ‘risk’ one wants to take. If you want a safe 4% you buy perpetual preferreds from Public Storage (PSA). If you want to earn 6-9% you move up the risk ladder.

This weekend I finally had the chance to do some reading–some research (due diligence). My choice for the day was checking out some of the recent financial reports and presentations from the commercial mortgage REITs—moving up the risk ladder. Obviously I only look at the company’s that have outstanding preferred stock and baby bond issues.

The commercial mortgage REITs have a plethora of perpetual preferreds and baby bonds outstanding-and from what I can see (or actually already knew) these issues are some of the most ‘hated’ in the marketplace.

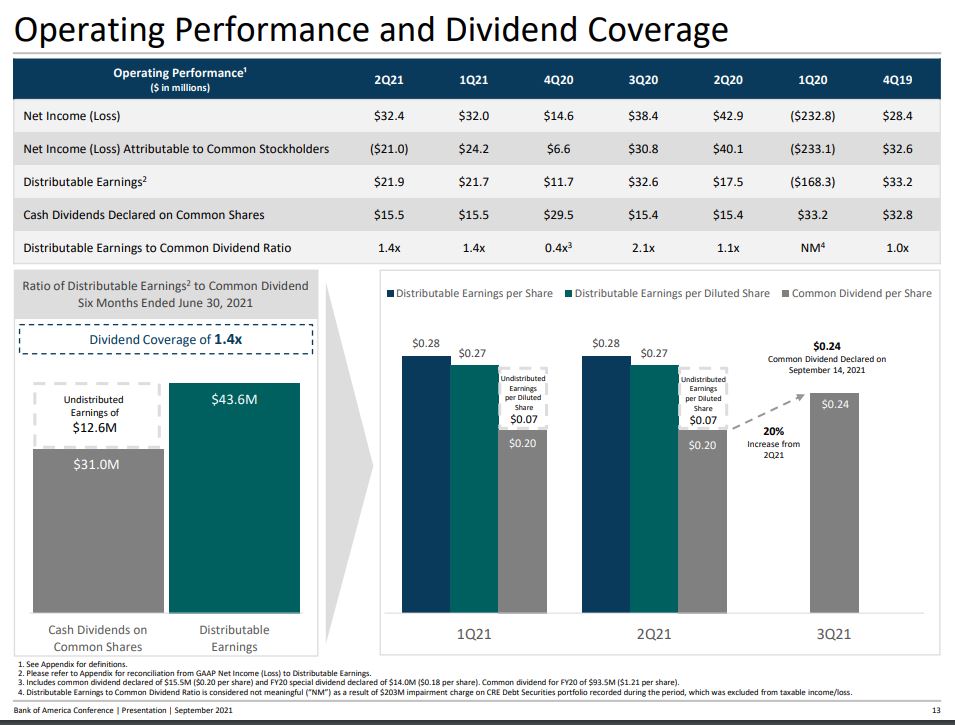

After my review I think I confirmed (at least to myself) that Ready Capital Corporation (RC) is solidly one of the best commercial mREITs out there–although the company now is more broadly diversified as they have substantial participation in the residential mortgage marketplace with the acquisition of Anworth Mortgage last March.

RC has grown their assets in the last year by $3.5 billion in the last year with the Anworth acquisition and with heavy participation in the PPP loan program during the pandemic. All in all the company is doing extremely well.

The company’s 3rd quarter presentation from 9/9/2021 is here.

Ready Capital has 1 perpetual preferred, 1 convertible preferred, 2 senior note issues and 1 convertible note issue outstanding-they can be seen here. Folks with a little tolerance for added risk should check these issues out–caution that many of these issues trade too high to be bought at this time.

Arbor Realty Trust (ABR) is a $9 billion commercial mortgage REIT focused on mainly agency (Fannie Mae and Freddie Mac) multifamily lending.

ABR is very well managed and during the pandemic minimized losses with only a modest amount of credit losses during the 1st quarter of the pandemic. Unlike many residential and commercial mortgage REITS that suspended preferred stock dividends for a short period of time ABR never missed a beat.

With solid financial performance and low interest rates ABR was able to ‘refi’ their high yield preferreds with 2 newer issues with coupons of 6.25% and 6.375% – all of which can be seen here. With these 2 issues trading at $25.42 and $25.55/share respectively and optional redemptions not starting until 2026 these issues provide a pretty solid opportunity.

While ABR doesn’t do pretty presentations for us you can see there lastest 10Q (quarterly report) here.

TPG Real Estate Finance (TRTX) is another commercial mREIT which currently has respectable financials. Unfortunately during the pandemic the company, which is most concentrated in the office loan segment, took a fairly giant level of write downs during the 1st quarter of 2020. You can see a fair level of consistency in the last numerous quarters, with the exception of the ugly writedown quarter in Q1, 2020 below.

The company issued a perpetual preferred on 6/7/2021–TRTX-C, a 6.25% which has traded poorly since a week or two after issuance. The issue closed at $24.33 last Friday (it had gone ex-dividend for 46 cents on 9/17/2021) so the current yield is 6.42%.

TRTX has just released a fresh Investor Presentation which can be read here.

Lastly I took a look at ACRES Commercial Realty (ACR). Previously this was Resource Capital and then it became Exantus, before finally becoming ACRES Commercial Realty (ACR) in February, 2021.

ACR suspended their preferred stock dividend in March, 2020 and these cumulative dividends were finally reinstated in September, 2020.

Just after the start of the pandemic the company received margin calls from their repurchase counterparties (debt is financing by short term repurchase agreements and when asset values fall sharply the counterparty may demand more collateral). The net result of this near death experience for the company was realization of huge losses.

In early August, 2020 the previous management of the company was terminated and ACRES Commercial took over management and simultaneously MassMutual Life Insurance and Oaktree Capital provided capital to ACRES to help shore up company finances.

In May, 2021 the company was able sell a new issue of perpetual preferred stock with a coupon of 7.875%. This issue joins the 8.625% fixed-to-floating rate issue which was already outstanding. Both of these issues can be seen here.

The company has posted their most recent investor presentation here.

With new management the company seems to be turning the company around and assuming some stability in the commercial market it appears the company will survive.

Remember it is all about the risk/reward and these 4 commercial mortgage REITs give investors a selection of baby bonds and perpetual preferred stock issues with coupons from 6.25% to 8.625% reflecting the various risks of the companys.

DISCLOSURE–I own issues from all 4 of the commercial mortgage REITs shown above–holdings are limited to smaller positions in each company.

Tim,

Thank you for taking the time to provide us with research on the mReits. I did place a small limit order on one of the companies listed. 🙂

Own most of them.

thanks –

Loading up on RC-E for the dividend capture Wednesday.

ACR is high risk that’s why ACR-C pays a high dividend. At par not above par so no reason I would consider their lower paying issue with no floor.

I’m with you, Tim, on ACR and RC issues, but as per my usual bent, with focus on the shorter or perceived shorter maturities… I own RCA and ACR-C. What’s interesting about ACR-C is I can’t think of another fixed to floating rate issue that only floats in one direction – UP… ACR-C can adjust UP from it’s present 8.625% but it can’t float to a lower rate…. That makes a call in ’24 highly likely. RCA has a ’23 maturity and is essentially non callable but it is convertible, but not unless RC hits 18.75, so we have a ways to go before that comes into play.

Yes you can think of another that can only float up, 2WR. You own another already…The late great WTREP.

Has is been called yet GB?

Not the late great until it is.

Or it’s late great because it’s not great any more

Its the late great because its not named WTREP anymore. Kind of like Prince was when he changed his name and had no name for awhile. But, personally, Martin, I still think its great. A 7% minimum floor that can only float north with solid credit, is great by me. As long as that divi pays, the brokerage can show its worth a negative amount of money. I like to trade, but I dont have to trade everything, lol.

Ahhhhh, but the difference, Grid, is that WTREP was designed that way right from its issuance and that’s what I was referring to… WTREP can only go up from here because it had a floor and it’s reached it now. It did float down from its original 8.50% coupon… Of course I had to look that up again on WTREP just to make sure, but that’s what I meant about ACR-C – one that could only float up right from its original pricing… It’s kind of weird why they put that in to the original docs, isn’t it. It certainly isn’t an example of companies always skewing the options in their own favor… That one seems to be solely investor friendly.

Considering how close Exantas Capital came to closing their doors for good back March/April 2020, such a feature may have been included specifically to lure investors who might otherwise pass them by. It worked on me anyway…its one of the few perpetual preferred shares that I own.

ACR-C was issued well before covid. 2014 or 2015 i think

I believe you’re mistaken about that…the old XAN-C was renamed ACR-C back in February 2021. Quantum Online may have more information.