Well last week was plenty wild and proved that equity markets can move down, but it also showed that the ‘dip buyers’ continue to do what they do – buy dips.

The S&P500 was up about a 1/2% last week which leaves the index about 2% off of record highs. It is absolutely no surprise that the dip buyers continue to come into the market–liquidity remains massive with about $5 trillion in money market accounts.

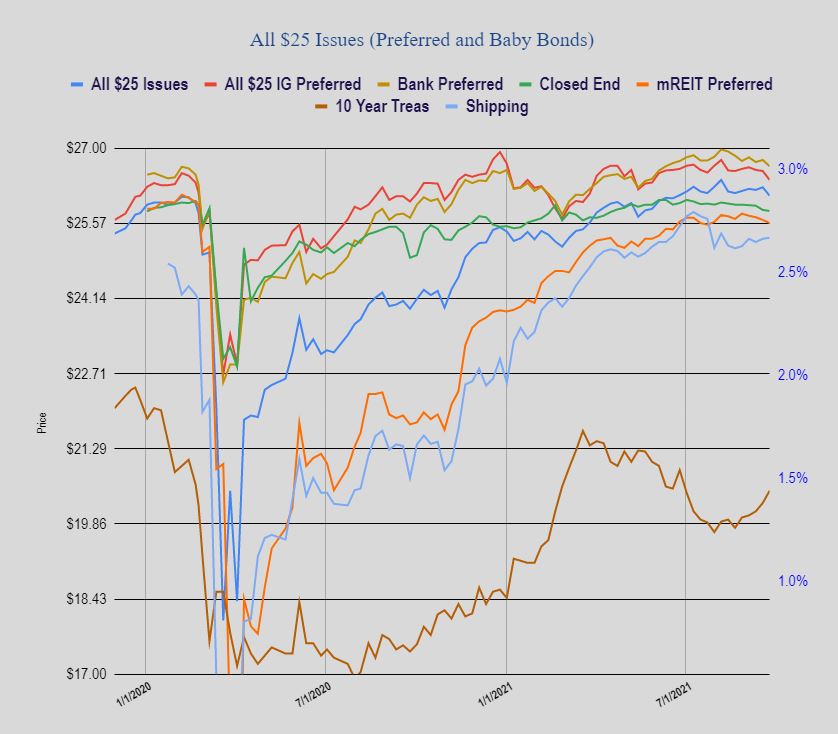

Interest rates finally began to move higher with the 10 year treasury closing the week at 1.46% which was 9 basis points higher than the previous Friday, but 16 basis points higher than the low on the week. Having a firmer taper start date in November does bring some certainty to the markets, although we all know that economic conditions can change quickly.

The Federal reserve balance sheet grew by $41 billion last week–no surprise. Each new week is a new record high balance sheet–now at $8.5 trillion.

The average $25 preferred stock and baby bond fell by 16 cents last week. While the average fall was just 16 cents I saw individual issues falling much more(50 cents to $1)–in particular those issues that were way overvalued in the $27-$29/share area. Investment grade fell by 17 cents, banks fell by 12 cents, CEF preferreds by 2 cents.

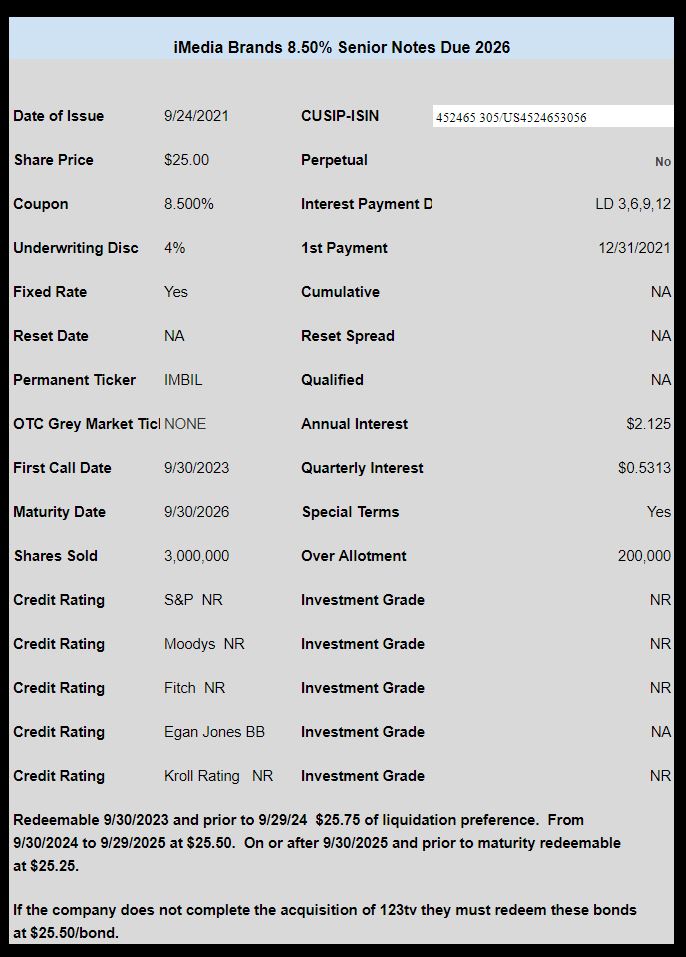

Last week we had just 1 new issue price and that was a 8.50% baby bond issue from interactive TV (shopping) owner iMedia Brands (IMBI). The issue will trade under ticker IMBIL when it begins to trade on NASDAQ–probably in the next few days.

We continue to await new issues from Eagle Point Income Fund (EIC), Priority Income Fund (untraded) and Sotherly Hotels (SOHO) all of which have registered new issues, but as of yet have not priced the issue.