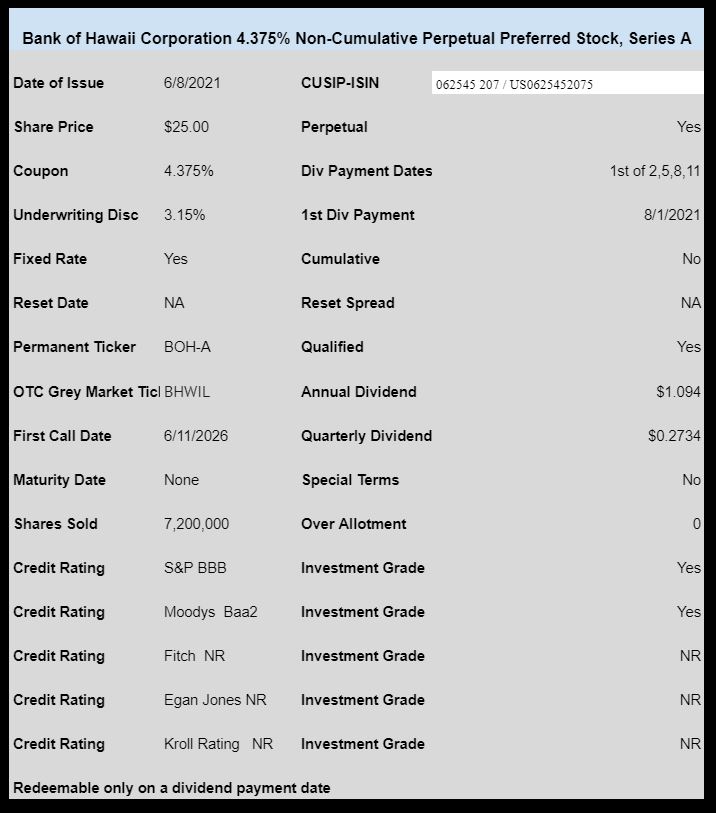

Bank of Hawaii Corporation (BOH) has priced their new non-cumulative preferred stock.

The coupon is 4.375%–the issue is qualified and investment grade.

The new issue will trade under the temporary OTC grey market ticker BHWIL immediately, before moving to the NYSE in the next week or so.

The pricing term sheet can be read here.

Bought a thousand and will hope for 26 and a flip. A case of Brunello as I see it. Not a long term hold for me.

I was able to pick up some of this @ the IPO.

Late yesterday I was digging into the bank’s financials and came away impressed.

Very good capitalization ratios and the dividend history including 2007-2008-2009 is par excellent.

As a long term holder of preferreds mainly for income I look at my preferreds as partnerships with the issuer. This one should be a good one. For the long term. If rates go up and the price of this one goes under par, I will buy more.

RB

I would be cautious about that. You are closer to being a creditor than an equity holder. They will be happy to call it if rates drop to 3 but you are in for life if rates rise. It is whatever is in the company’s best interest, not yours.

If you want to be a partner, consider buying the common.

BHWIL sure did open strong!

I don’t want to start an argument but would like to say when I see these decent quality companies being able to issue these very low coupons it will be extremely interesting to see where that $25 preferred is trading in say 2 or 3 years well before the call date. I’m thinking there are tons of very “naive investors” that are going to get a shock to their system.

I felt the same way when they were issuing 5+% issues. I’m willing to buy to flip when the relative value seems good. This issue is trickier so I’m just going to pass.

No argument here. I’m a long term buy and holder and I’ve been using 5% as my lower limit more or less. In the low fours heck I could just buy Verizon stock for that income with minimal capital risk.