Wow – it is just occasionally we get quality issues absolutely hammered, but today is the day. We have quite a few issues down 4%, including baby bonds and preferreds from DTE Energy (DTE) and CMS Energy (CMS)–the saving grace for me is small position sizes for these types of issues.

Additionally we are seeing the same type of losses in some of the community and regional banker issues. CNB Financial (CCNE) preferred (CCNEP) is off almost 5%.

I’m certainly not selling into this fall–but of course I am not buying either. As boring as it is to do nothing for now it is the right thing to do. My portfolios are off .3 or .4% but the world won’t end with those losses–but it certainly hurts.

I guess the best way to look at this pain is that it is preparing us all for future true bargain hunting.

Investors are demanding a higher and higher ‘reward’ for holding U.S. Treasury paper–right now the demand is for 4.74% on the 10 year treasury. All the talking heads on the business channel are flailing away trying to identify why rates are moving higher while the economy has ‘cracks’ in it. Honestly the cracks in the economy have not been deep yet–employment remains extremely strong, although maybe very slightly weaker, but to call employment weak is just silly. Let’s face it – with the amount of new ‘paper’ coming out of treasury why should rates be lower? Huge supply and lack of faith in the U.S. government to control spending–period-enough said.

Yesterday was a slightly painful day for income issues–even with a pretty large allocation to CDs and treasuries in our accounts it has been fairly difficult to gain much ground–lots of interest coming into the accounts, but the modest preferred and baby bond allocations are neutralizing the gains as they tick lower. At this point in time I am looking for CD rates to move higher–but now I am looking at the 6 and 9 month variety–the more time that passes and the higher rates move the more I want to make sure I have some dry powder available to buy at interest rate peaks (as if I can successfully identify that peak).

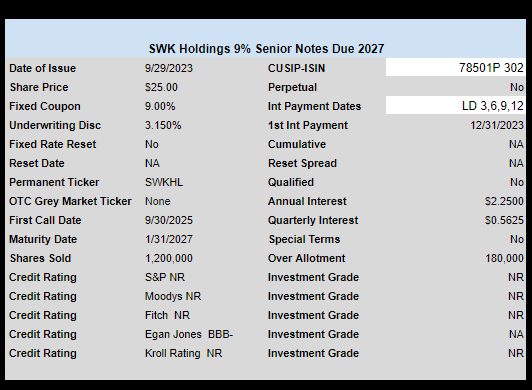

I posted info on a new baby bond from SWK Holdings yesterday–a very interesting company–specialty finance. This company started off as a software company back in the 1990’s–and slowly morphed into a specialty finance company. They own royalties rights in various drugs and make term loans in the health care sector. Very interesting company and if their financial statements are trustworthy their net income is somewhat lucrative. I have no interest at this point in time, but will study it further.

Continue to sit tight and see where we are headed–equities are soft this morning as rates rise–could be a very tough month.

SWK Holdings Corporation (SWKH) has priced a new issue of $25 senior notes.

SWKH is a specialty finance company and must maintain a 150% coverage ratio on these securities.

The notes have the normal terms–quarterly interest payments, a optional call starting 9/30/2025 and a maturity on 1/31/2027.

The notes will trade on NASDAQ under ticker SWKHL–we probably won’t see them trade until sometime next week–watch your broker website for the start of trading.

Well September is over and it was a somewhat difficult month for both stocks and bonds, although for many of us with 50 years of investing experience we have seen many months that were more negative than the 4.9% loss that the S&P500 incurred.

Last week the S&P500 fell by .7%–which interestingly is just 7-8% below a 52 week high. Right now the equity futures are dead flat.

Interest rates are really the big story and they are near a 15 or 16 year highs–the 10 year treasury traded up 14 basis points to 4.57% on the week–which is a pretty large weekly gain, but the close Friday was near 12 basis points below the high of 4.69%.

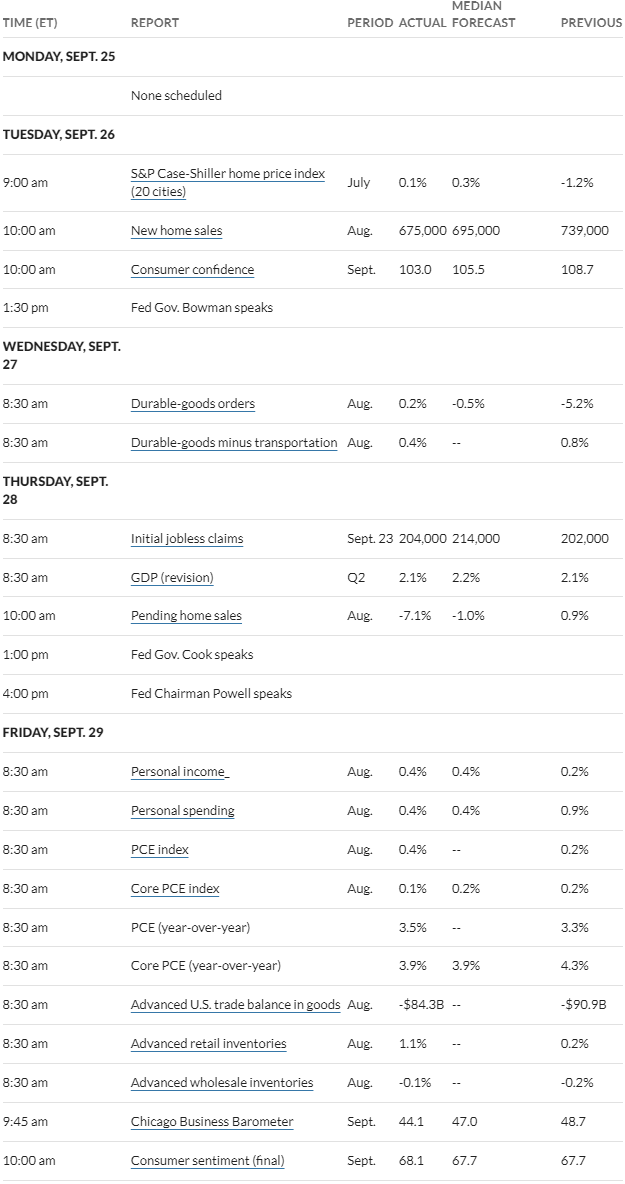

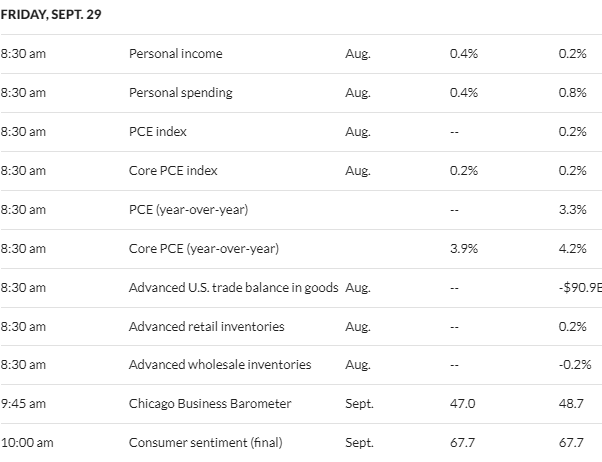

Last week we had a fairly heavy economic calendar with the personal consumption expenditures (PCE), which was released on Friday, being the most important coming in favorable to forecast.

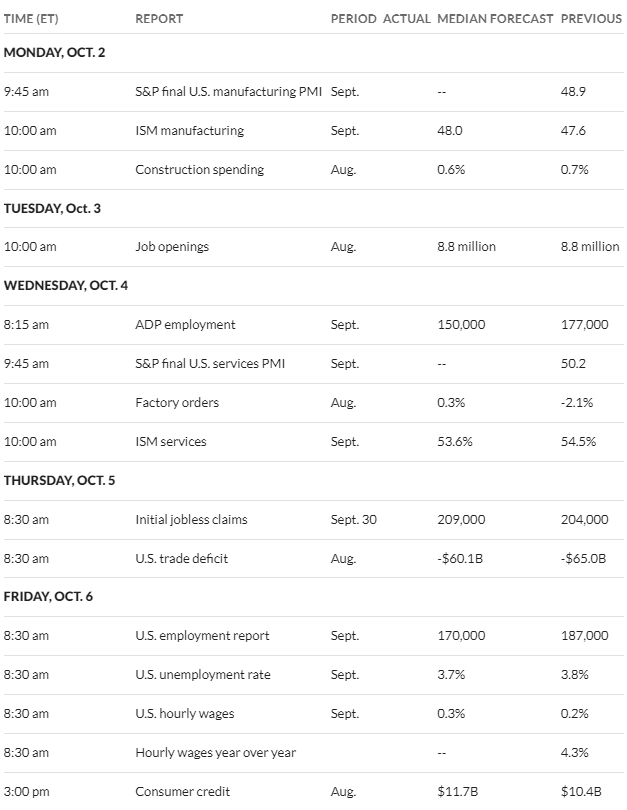

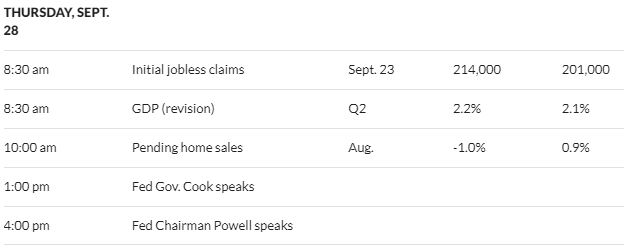

This week is kind of a medium load of economic data–but of course the most important (or at least most closely watched) will be the employment report on Friday. It is difficult to see a meaningful recession if employment remains super strong.

Last week the Federal Reserve balance sheet assets fell by a somewhat normal $22 billion. Finally we will be going below $8 trillion in the next 2 weeks.

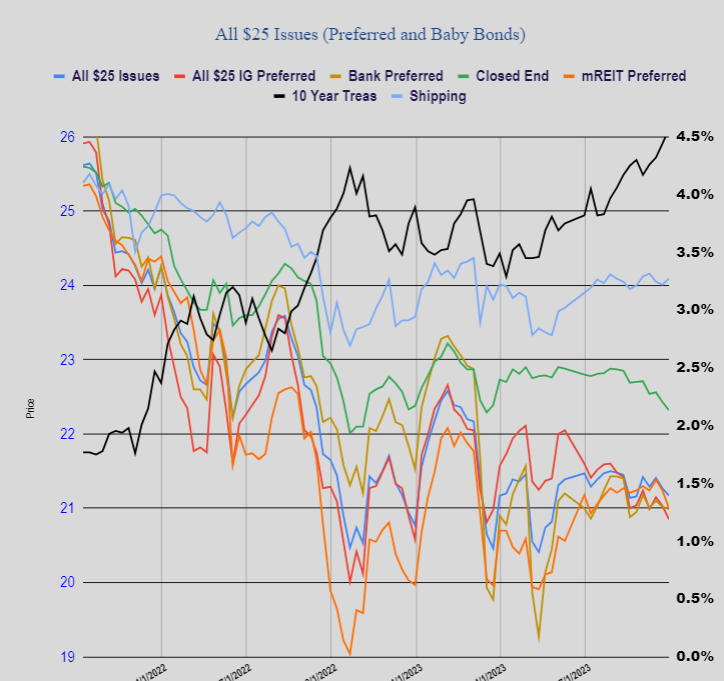

Last week the average preferred fell by 10 cents. The weekly drop was much worse going into Friday, but we saw a decent bounce. Investment grade issues were off 18 cents, banks were off 3 cents, mREIT issues were off 24 cents while shipping issues were up 8 cents.

As is the norm we didn’t have any income issues prices last week.

While I wouldn’t call this week a ‘disaster’–at least in my accounts, there was certainly plenty of pain. I have 3 major brokerage accounts and 2 of them were off 1/4%–but the 3rd has taken about a 1/2% hit. This doesn’t really compare to losses we have seen in the past–of course most of this is due to portfolio composition which has never had such a large weighting to CDs, treasuries etc.

I see that oil prices are up a buck this morning trading right around $93/barrel (WTI). I paid $3.79/gallon yesterday–from a consumer confidence perspective it seems that $4.00 a gallon is about when folks start to really be squeezed (at least the ‘have nots’). Thursday price hit the high $94s per barrel–so maybe we have seen the highs, although I don’t really understand oil price dynamics so who really knows.

So we are 30 minutes from important economic news–personal consumption expenditures (PCE) in particular. While equities are up nicely at the moment and interest rates are down at 4.54% right now we know how quick this can change—30 seconds more or less.

I don’t even have to say it, but I will not be buying or selling anything today- just my gut feel at this moment is that there will be no reason to buy for weeks to come–by then we have new data and maybe it changes my outlook, but right now just watching from the sidelines.

We are very close to the point where most house sales will come to a halt. Yes there will always be some activity because sometimes folks have to move–for jobs etc. But from my close up view in Minnesota, what was already a fairly slow market is slowing further and properties for sales are remaining on the market longer. Prices are high–and coupled with mortgage interest rates that have moved up 20 basis points just this week means the moment of truth is just about upon us.

Today I am working on 2 properties that are sales—both family related (sold by parents to children or grandchildren), so they are special circumstances. Also I have a plate full of orders that are all home equity loans–yes there are a few lenders that require an appraisal for a home equity loan versus just going off the tax assessed value or some similar value. I have no idea what interest rate they are paying–but it would seem those will grind to a halt soon as well.

So my point is that the marketplace may well take care of slowing the economy without a need for incremental Fed Funds rate hikes. If builders in our area aren’t slowing construction they are pretty foolish–it looks like a good year to ‘take the winter off’—we’ll see.

Well we are seeing higher interest rates this morning with the 10 year treasury now at 4.66%–with economic news being released today who knows where it goes to.

Equities are flattish this morning–yesterday equities were down about 1% most of the day before a fairly furious rally the last 90 minutes of the day which brought the S&P500 index to be slightly positive. So we certainly can see some crazy things happen – whether we see more of that today is anyone’s guess.

I was looking at my U-Haul Investors Club accounts yesterday and am pondering whether this vehicle has outlived its usefulness. For the 1st time in many years their securities being offered are not being oversubscribed. Their coupons are obvious inferior (4.75% to 5%) as measured by risk/reward. They are illiquid and uninsured and they have substantial competition from other income issues–whether it be CDs, treasuries or even corporate bonds. Thinking I might begin to build some cash in those accounts and then transfer to my brokerage accounts where I have more alternatives at fairly decent rates.

Well this will be another ‘do nothing’ day for me–just hanging out and watching.