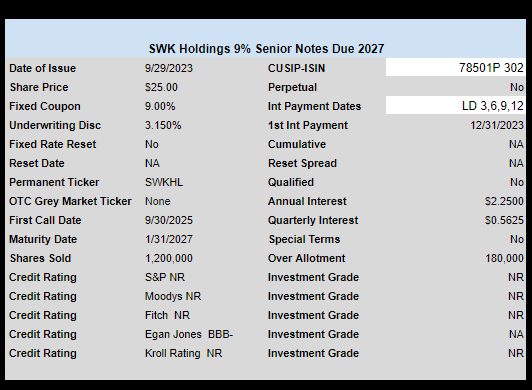

SWK Holdings Corporation (SWKH) has priced a new issue of $25 senior notes.

SWKH is a specialty finance company and must maintain a 150% coverage ratio on these securities.

The notes have the normal terms–quarterly interest payments, a optional call starting 9/30/2025 and a maturity on 1/31/2027.

The notes will trade on NASDAQ under ticker SWKHL–we probably won’t see them trade until sometime next week–watch your broker website for the start of trading.

The pricing term sheet is here.

Thanks to Peppino for catching this one.

Most Baby Bonds are micro-cap in capitalization, with the inherent risk of being pulled down to market/economic issues. Most are not rated with income and balance statements subject to market volatility. Breath deeply when buying!

I know absolutely nothing about this company. Does the company deal with assets that can possibly lose 35-40% of their value suddenly? Perhaps they use leverage in some way or their borrowers are risky? What is the catch to earning a 9% yield? And yes I realize they have to pay more now days but that seems high.

I shall do some reading after I post this but per the norm folks here often have great insights.

I am probably not the only one who thought it was the stanley black and decker at first glance. SWK.

fc—yes do some good due diligence. I saw they had 4 billion in accumulated losses and I quit reading—has to be more to this story.

I did a quick search and came up with a microcap stock current value of 197 million. They just received a 40 million dollar line of credit they haven’t used yet and now floating this note for 30 million. They’re in the business of financing bio tech start ups I think. Over 1/2 of those ventures fail.

DYODD

The 9% coupon got my eye. Not familiar with the firm, but it looks like they

are a $200M market cap firm that operates in 2 segments: specialty finance and pharma.

I briefly skimmed website, 10Q, Prospectus and 10K. Got far enough to get to a no.

The firm has been around for a while since the 90s and at a cursory glance several of the portfolio loans/royalty deals have been round for 10 years plus and so they appear well seasoned.

What I don’t like about it (at first glance) is that in addition to the BDC style life sciences focused lending/royalty operations it also manages a pharma business. The pharma business is burning cash as they pour it into R&D there is also a G&A expense which must be driven by the pharma business – pharma is G&A intensive due to the compliance burden caused by regulations.

This explains the use of funds language in the prospectus. It looks like they do plan to use these funds to fund R&D in the pharma business in addition to investments in the BDC business.

This could very well be a great investment and the 9% coupon does catch notice. However, this is a $200M firm with two wildly different (IMO) business lines – BDC style loan/royalty deals with in the life science space and a pharma business. These funds are going to be used to fund both of these business segments.

I might be interested in the 9% notes or the common stock if this was a pure BDC firm, but for a $200M market cap firm I want to see laser like focus: pick one business. For me it’s a pass for this reason.