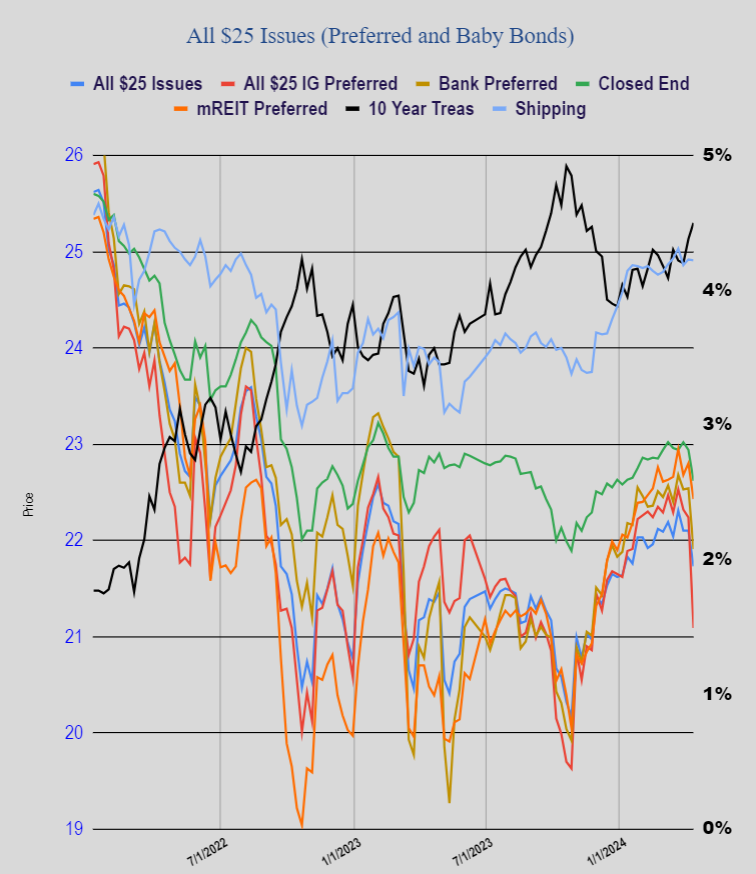

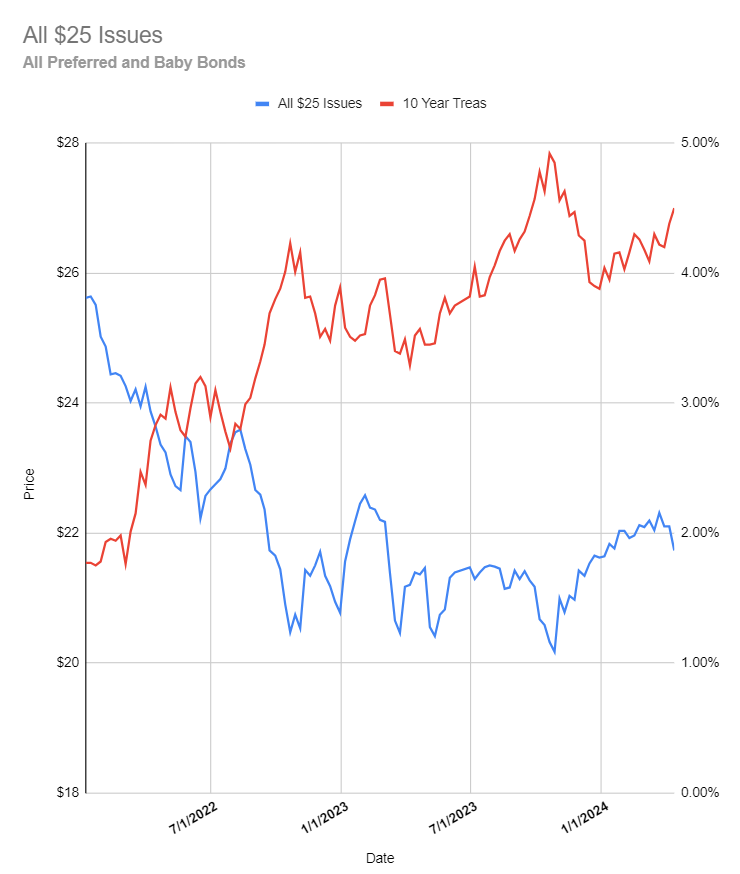

So we have had almost 2 months where interest rates have been trending higher—the last time we had the 10 year treasury under 4% was back on 2/2/2024—from there it has been a constant push higher. During that time frame economic news has not been friendly to rates as jobs have held up well, retail sales have grown at a rate above expectations and inflation numbers have held at or even above expectations.

The Fed continues to hint at rate cuts—which in my opinion was a major mistake. It makes no sense to promise (or near promise) rate cuts without seeing the ‘data’—last I knew they claimed to be ‘data dependent’ which obviously they can’t be if they are promising rate cuts somewhere in the months ahead.

As always we, as investors, have to use our thinking–what am I seeing and what logical conclusion does my thinking lead me to relative to investing?

So now, I see no reason for the Fed to cut rates–the data taken as a whole does not warrant a cut. This morning we got a housing starts number that came in soft–down 14% month over month which translates into a shortfall of over 200,000 units. While this is a soft number it moves a lot from month to month and 1 month doesn’t make a trend.

We have seen quality, low coupon, perpetual preferreds, and very long-dated maturity (out 30 or 40 years) baby bonds move sharply lower as rates have shot higher. Does one buy? It seems logical to me that with competitive rates in the money markets, CDs, and short maturity treasuries at 5% or higher that it makes little sense to be a buyer–but on the other hand if one is an investor looking for solid income (less concerned with capital levels) maybe it is a good time to buy–at least some nibbling. So everyone is different–every single one of us.

I am looking only at positions I currently hold for any possible small nibbles—as shown on my laundry list of holdings. I am looking for safety today–so will possibly take a nibble or two on a CEF preferred. I would consider a term preferred at the right price–although I am loaded pretty heavily with term preferred already. We’ll see what the day holds (or maybe a week)–not desperate to do anything–but would take a nibble on a perceived bargain.