Anyone interested in the CTO Realty 6.375% perpetual preferred (CTO-A) it is now trading at $20.12 for a current yield of just shy of 8%. The company sold another 1.5 million shares of this issue last night (with another 225,000 available for overallotment) at $20/share.

This is a follow on issuance — originally the issue was sold in June, 2021.

Thanks to Grid for posting the Pricing Term Sheet this morning--it is here.

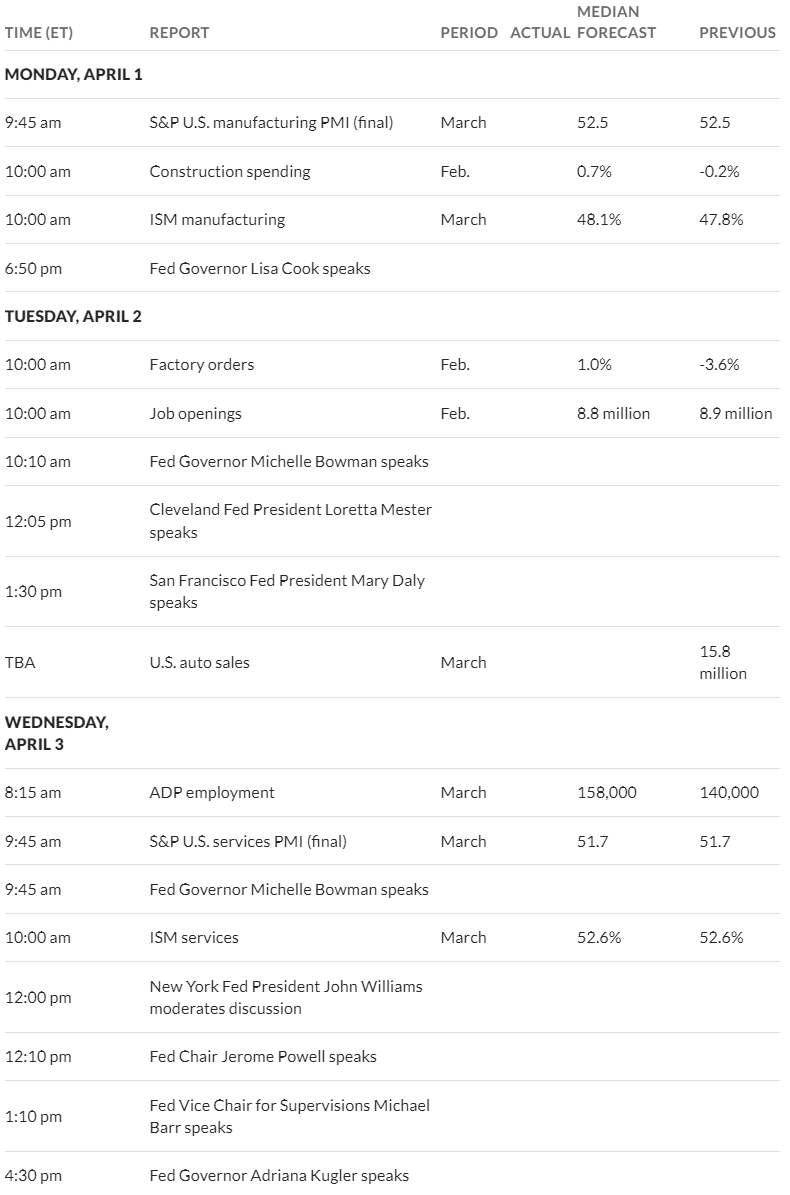

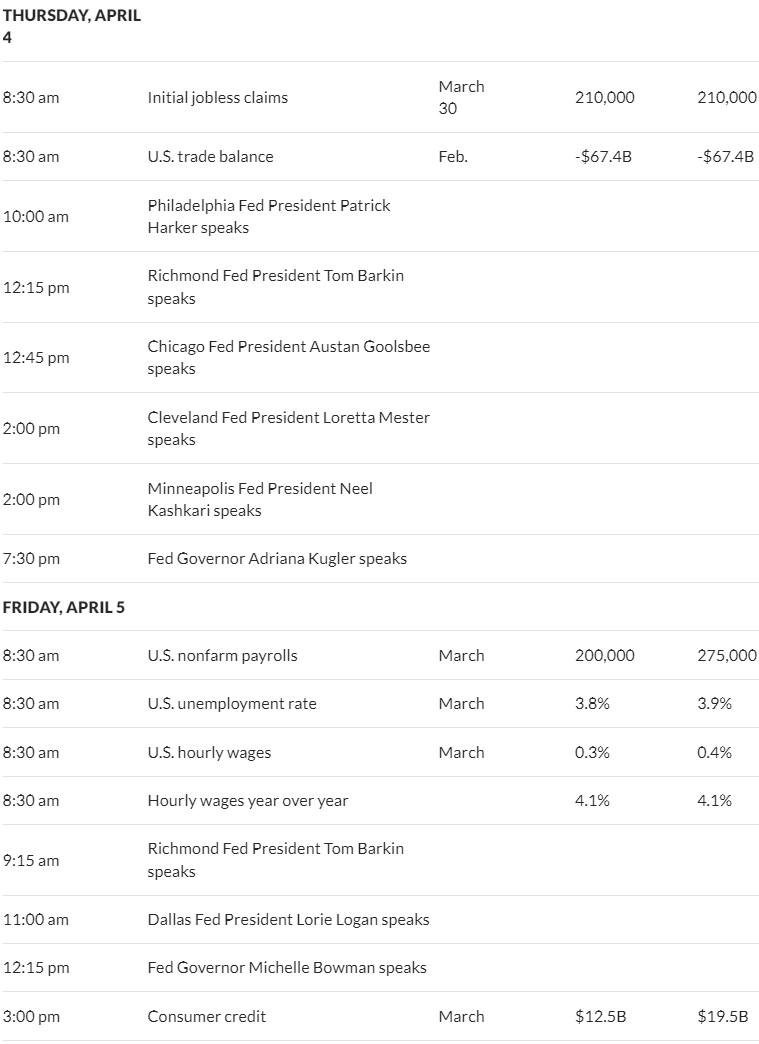

Markets are not just about inflation–an equal influence on the economy is jobs and there have been few (if any) signals that we are seeing any job softness. Once again we got a jobs number yesterday that did NOT indicate softness when ADP reported their March number for new jobs created when they reported 184,000 new jobs created against a forecast of 155,000. Additionally the company reported a higher revised February number. New jobless claims for the last week will be reported in 90 minutes and the forecast of 213,000 is likely to be higher than reality–the forecast has been too high most weeks this year–we’ll see.

Tomorrow we have the ‘official’ government report for March–forecast is for 200,000 new jobs which is not a blockbuster number, but it certainly doesn’t indicate a failing economy.

I have been watching oil prices–how can one help it as we have to buy fuel for our vehicles. West Texas intermediate has been trading in the mid $80’s for the last few weeks–this is 15% higher over the course of the last year an up 18% YTD. These prices bleed into the economy-over time and you can be certain that the negative affect on overall inflation is going hurt at a time when folks are pretty sick of paying higher prices, although not sick enough to quit buying inflated products apparently.

Everything points to higher rates for longer–what is longer? Who knows for certain, but if inflation remains elevated (above 2%) and employment remains fairly strong why the heck would the Fed lower rates? Honestly interest rates are NOT high–on a historical basis. Folks want free stuff–including free money–but as an investor I want to be paid for others to use my money. For years they wanted my money and didn’t want to pay me for the use–now I am getting paid a fair rate and it makes me very happy.

The 10 year treasury is at 4.37% after popping to 4.40% yesterday on strong employment–tomorrow we will see if rates are shoved higher or lower with the March employment numbers–it is a very important number.

Real Estate Investment Trust CTO Realty Growth (CTO) has announced they will sell 3 million additional shares of their currently outstanding 6.375% perpetual preferred (CTO-A) which closed today at $20.62/share for a current yield of 7.73%–shares are tumbling after market now at $20.06. This issue originally was for 3 million shares. All terms of the new shares will be the same as the original shares.

I was surprised and pleased that the jump in interest rates did very little damage to our investment accounts–although account balances are distorted by the fairly large influx of interest payments on CDs (balances rise with interest payments while they fall back a bit with share price losses). The large allocation to CDs certainly kept the damage minimal–so the question is whether rates are done moving higher or not. Obviously no one knows — I question whether we have seen a peak in rates–will markets tire of financing the deficit spending of the U.S.?

Yesterday I was hunting ‘bargains’ (we all define bargains differently) and found a few possibilities which I might buy today. I am mainly watching the short maturity term preferreds and baby bonds—as most of us know issues that mature in a couple years generally don’t move much in share price—many times they trade at $25 plus accrued dividends or interest. I will list those bargains I buy – they are thinly traded so I may not be able to get them at my price–we’ll see. The list of term preferred and short maturity baby bonds is here.

Right now interest rates are about flat with yesterdays close with the 10 year treasury at 4.37%. We will have employment numbers for the next 3 days and these should set the tone for interest rate movements. I have stated it is my belief that the Fed really wants to see soft employment for a number of months as a reason to lower Fed Funds–and generally employment has held up well. Yesterday we had JOLTs (job openings and labor turnover) announced and with 8.8 million job openings there is no reason to believe that employment numbers should falter yet–we’ll see.

Equities are real quiet now after a couple rough days–awaiting news. Let’s get going!!

Yesterday interest rates popped closing at 4.32% and this morning the 10 year treasury yield is continuing to rise – now at 4.37%. The S&P500 fell .2% yesterday and this morning the futures are down about 1/2%.

Really there is no apparent definitive reason for interest rates spiking–yes we can all speculate many different reasons, but in the end there are more sellers than buyers (at a given interest rate level) and buyers are demanding a higher yield (lower price). Maybe the economy is too strong–maybe the treasury is issuing more supply than folks are willing to buy (we know they are)–and on and on. In the end we have higher rates.

Yesterday we didn’t see much damage to income issues to speak of, but today we could start to see falling prices and higher rates start to become more apparent to investors. We always need to remember that a big downdraft in common shares WILL drag income issues lower–the only question is how much damage is done.

I will be watching for damage in income issues with short term maturities–i.e. term preferreds and baby bonds. These issues are unlikely to be hurt much as they near maturity–but if they are sent lower they would be good buys as their yields to maturity rise. Given the uncertainty I won’t target perpetual shares as much because capital losses could be severe if rates continue higher.

Well let’s see if we see a bounce in common shares mid day or if prices continue lower. It should be an interesting day – so many factors are present and it has been a long time since we have seen a big S&P500 tumble–maybe the time is here for a fall.

I just took a nibble on the newer Carlyle Credit Income Fund 8.75% term preferred stock—CCIA. This issue was floated 10/18/23. I have been watching the issue and it has been trading above $25 since issued and now is trading at $25.40. A bonus (at least to me) is that the issue is a monthly payer–I always prefer money in my pocket instead of waiting 3 months for a payment.

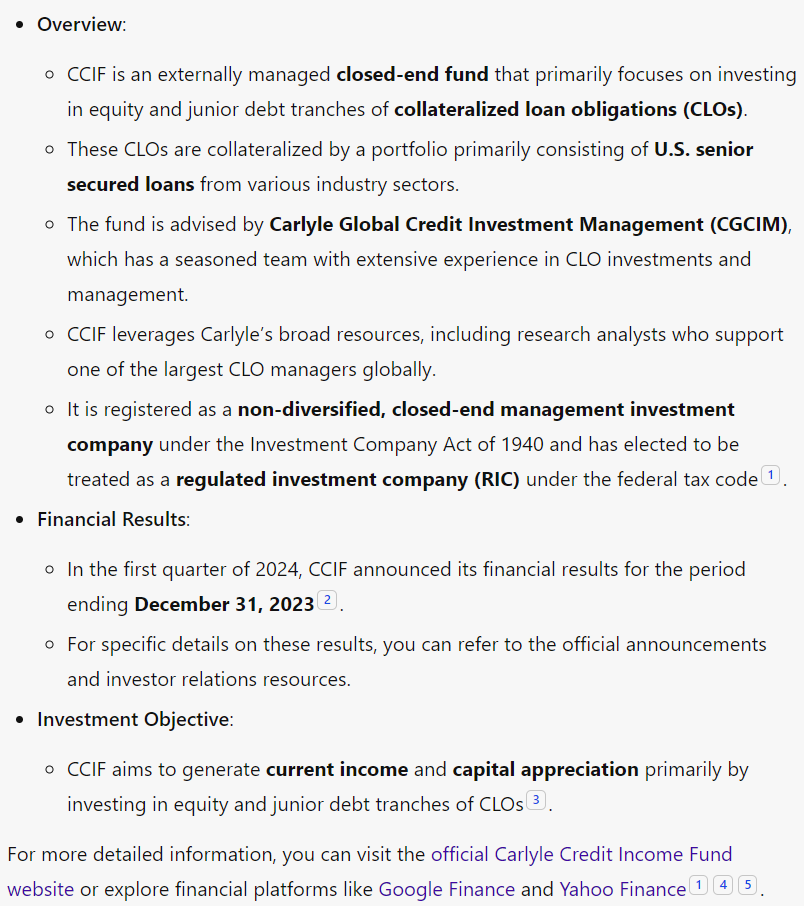

CCIF is a newer fund (actually a rebrand of another fund) and is relatively small–around $100 million and Eagle Point Credit (ECC) owns a large position in the common shares.

CCIF is an owner of CLO (collateralized loan obligations) – so comparable to the Eagle Point Credit (ECC) issues and the Oxford Lane (OXLC) issues. I bought the Carlyle issue because it is a 8.75% coupon and has a relatively short maturity which is in 2028. This nibble helps to balance the last purchase I made which was the Spire 5.9% perpetual preferred (SR-A) which is a quality utility issue.

Below is an AI generated recap of the Carlyle Credit Income Fund.

Time get back to work after the 3 day weekend. Equity markets are up this morning—a reaction from what is being perceived as a dovish personal consumption expenditures (PCE) number on Friday. I took the number as a neutral number, but it doesn’t matter what I think.

The S&P500 moved higher last week by a small amount—just .38%, but after the large gain the previous week a little digestion is to be expected.

The 10 year treasury didn’t do much of anything–closing down just 1 basis point from the previous Friday at 4.21%. Right now the 10 year is at a yield of 4.21%–very, very quiet. With the supposedly dovish PCE number on Friday I thought we would see rates down some this morning. This week we have the biggest economic number being released on Friday with the employment number for March on Friday. For the coming week we also have bunches and bunches of Fed yakkers–not that they should move far away from the chairs ‘line’ which is inflation is too high and we need to see more progress toward the 2% goal.

The Fed balance sheet fell by $30 billion last week–now at $7.84 trillion.

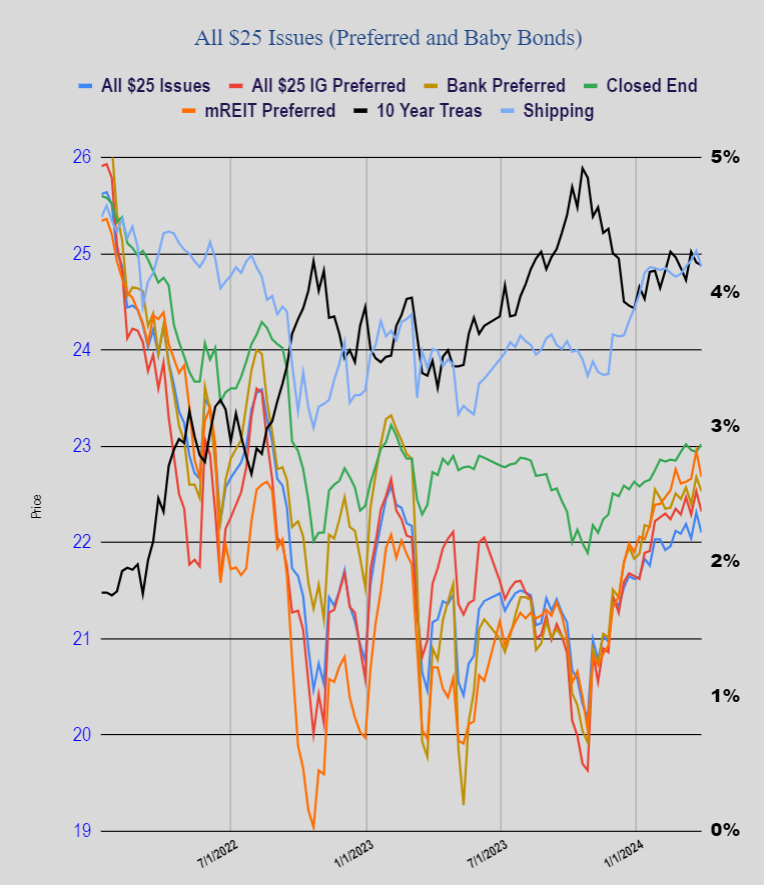

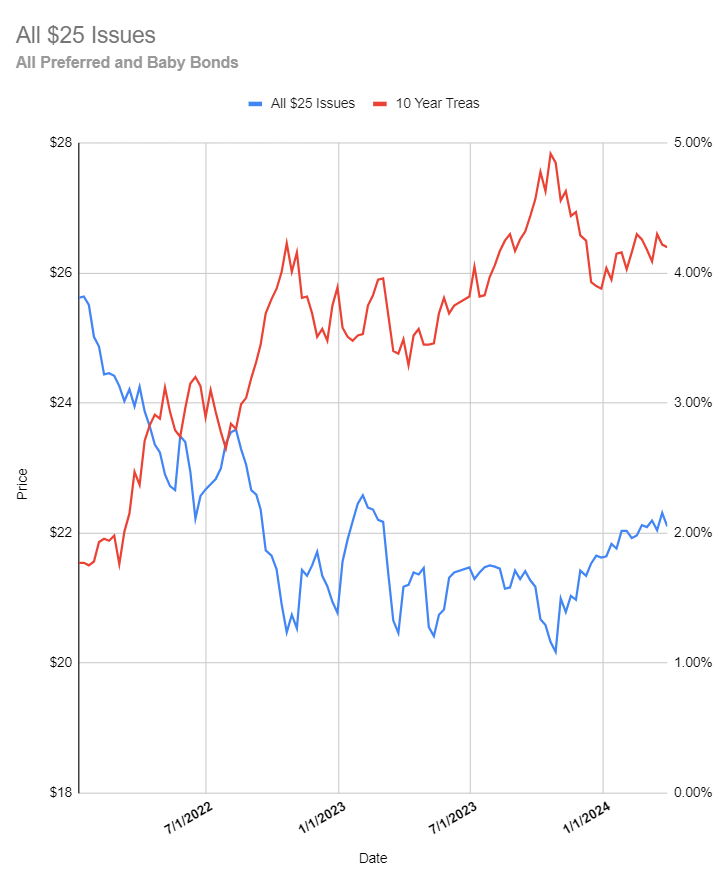

Last week in spite of little movement in the 10 year treasury we saw losses in $25/share preferreds and baby bonds with the average share price moving lower by 21 cents – closing at $22.10. Investment grade issues moved 21 cents lower, bankers down by 15 cents, mREIT issues were 27 cents lower and shipping issues were down 17 cents.

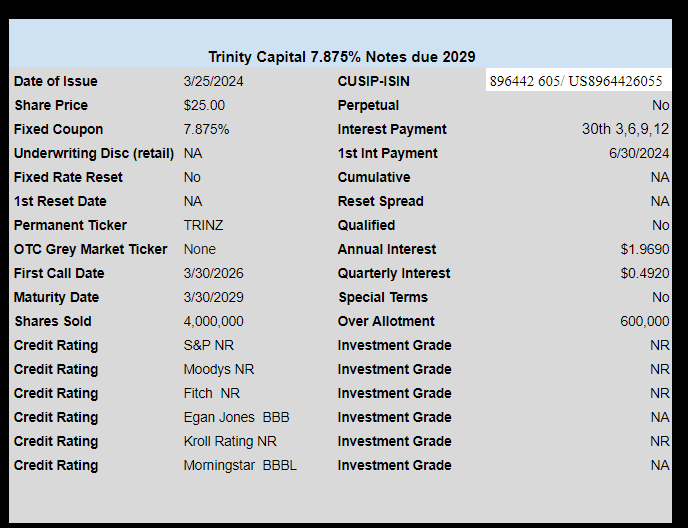

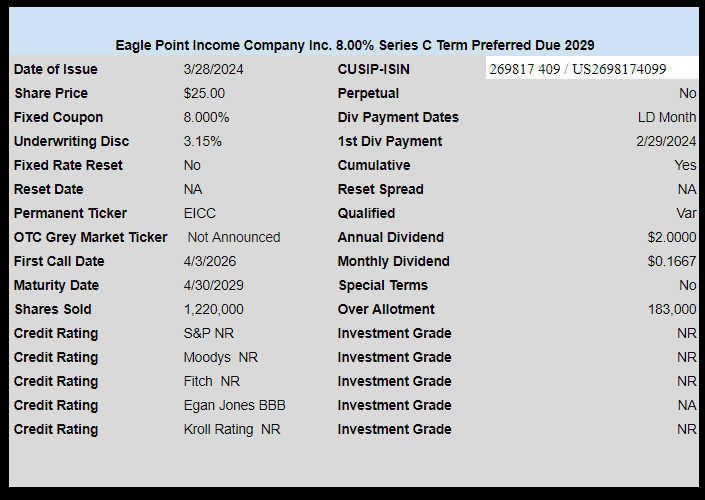

Last week we had 2 new issues priced. CLO owner Eagle Point Income (EIC) priced a nice 8% monthly pay term preferred issue, while BDC Trinity Capital (TRIN) priced a new baby bond with a coupon of 7.865%. High yield issues keep coming and most of the recent issues are trading solidly. These issues are not trading as of yet.

Today we have no equity trading, but we do have treasuries which will be trading until 1 p.m. (central) so we will see what treasury markets think of the PCE numbers. Markets have been expecting the core component to be up 2.8% year over year with the headline number index at .4%–up from .3% last month.

I don’t think the direction of the Fed relative to the Fed Funds rates will be swayed by this single number–they are on hold for now. But the length of time before we see a fed funds rate cut could be altered.

We could get a big reaction in the treasury market to the PCE. The 10 year treasury closed at 4.21% on Thursday we’ll watch for reactions.

We have just gotten the release on the PCE. The headline number is .3% versus expected of .4%. The core price index is 2.8% right on forecast. Incomes are a little above forecast while spending is way above forecast–running up the credit card debt I guess.

Seems fairy neutral overall–we’ll watch interest rates through the day and see where they head.