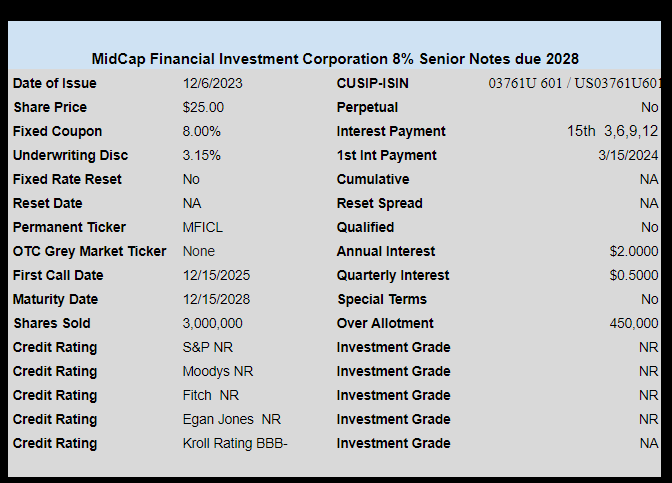

BDC Midcap Financial Investment (MFIC) (formerly Apollo Investment) has priced their new baby bond issue. The issue prices at 8% for 3 million shares plus an over allotment of 450,000 shares (bonds).

Kroll rates the issue BBB-

Look for this issue to trade on the NASDAQ in the next week or so.

Common stocks can’t decide what to do – go up because interest rates are falling or go down because the economy may finally be softening and heading to recession.

The 10 year treasury is trading with a yield of 4.11%. Employment is softening–per ADP anyway. Makes me more curious on what we will see Friday with the ‘official’ numbers from the BLS.

As I figured I am doing nothing at all. I did look at the Bridgewater Bancshares 5.875% perpetual (BWBBP) issue and pondered for a moment taking some profits–but no. I bought it for the over 9% current yield so just as well keep holding–plus I have no better idea at this moment. I guess for now I will just sit back and exercise some patience and do nothing.

The lowly ADP employment report is released in about 30 minutes. Months ago that report would be met with a shrug–numbers were no good (so they said) and only the ‘government’ numbers were ‘official’–even I agreed with this point of view. Now we anxiously await the numbers.

Now we are stretching – looking for every little glimmer of economic slowing – but in such a way as to maneuver a soft landing. Who knows if this is possible–no one knows of course. On the surface one could see a soft landing–but I don’t see it if interest rates do what I think they will do. Falling rates into mid to late in 2024–then heading higher as global investors demand higher rewards for holding U.S. debt. U.S. debt will undergo ratings cuts from all the major ratings agencies by then late 2024–if not sooner.

Back to ADP–the forecast (guesses) is for 128,000 new jobs being created in November. 113,000 were claimed to have been created in October. Slower is better I guess–goldilocks is 110,000–not too hot, not too cold.

The 10 year treasury is trading around 4.2% right now which is up a few basis points from yesterdays close. We have seen darned little movement in income issues this week- tiny bit higher or tiny bit lower. Equities are flattish awaiting news.

Probably doing nothing today – have some dry powder from sale of Hennessy Advisors 4.875% baby bonds, but will have much more on 12/15 when maturities hit on some CDs. Guess I will have to get off the fence once I have more dry powder–no longer can use the excuse of not having dry powder.

Wow–the softening job openings report has really hammered interest rates lower – the 10 year Treasury now off by 11 basis points.

Obviously the folks trading bonds are are thinking like I have been thinking–it’s all about jobs, jobs, jobs.

The Job Openings and Labor Turnover report just came out this morning and job openings fell to the lowest level since March, 2021. Job openings are still plentiful with 1.34 jobs available for each unemployed person out there–just the same it is all about the direction and the direction is softening.

No doubt that the FOMC will leave rates unchanged next week.

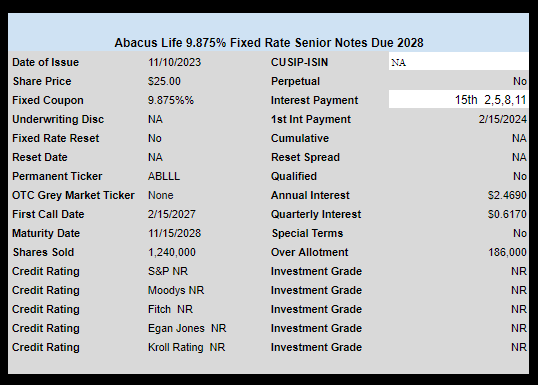

Specialty asset manager Abacus Life (ABL) has sold a new issue of high yield baby bonds. This issue was overlooked by me, but 2whiteroses pointed it out. Officially these shares were sold on 11/10/2023, but only registered a few days ago.

The issue has a coupon of 9.875%. It is unrated.

The issue is currently trading under ticker ABLLL and the last price was $24.26.

This is not your typical insurance company – actually they ‘provide liquidity to life insurance policy owners’ – i.e. they buy life insurance policies from folks at a discount (as I understand it from a quick skim) Very interesting.

Any time we get strong runs up-or even down it is totally normal to have a day or 2 of backing and filling. Yesterday we had a tiny amount of giveback in preferreds and baby bonds as prices fell by a nickel or a dime. After the run up we have had in prices the last 5 weeks I am more than happy to have falls of only nickels and dimes.

While common stocks fell yesterday and look pretty soft this morning I think it is a struggle going on—is the economy going to continue strong going forward and thus these high equity prices are justified—or are we going to finally see the recession that everyone has continued to predict and thus equity prices are too high? The S&P500 is not all that far away from all time highs–is this justified if we are on the edge of recession?

Today the 10 year treasury is trading at 4.23% which is 5 basis points lower than yesterdays close. With employment numbers this week we could see interest rates move sharply–up or down-who knows? Tomorrow we have the ADP employment report–job creation report. While ADP ‘got no respect’ from investors last year, we are now seeing more respect for their numbers-folks are thinking maybe their data is pretty damned good. Forecasts for ADP job creation is for 128,000 new jobs in November–Octobers number was 113,000. Friday we have the ‘official’ report on employment with forecast for 190,000 new jobs (versus 150,000 last month).

Yesterday I did nothing at all investment wise–I have a little cash from some sales last week so part of my decision is on allocation given my personal belief that interest rates will drift lower until debt issuance by the Treasury forces rates higher later in the year (2024). I am thinking in need to add more short duration term preferreds or baby bonds – if interest rates move as I think they will the share price of short duration issues will not move much – a steep rise in rates late in 2024 will slaughter perpetuals.