I took some time this weekend to create a new “Laundry List” of my holdings–now in spreadsheet format with notes.

As I have mentioned too many times we all invest differently and have so many different needs, resources etc. etc. etc. so my list is just meant for information purposes–nothing more.

My brain always goes back to ‘suitability’ – none of us knows what is ‘suitable’ for any given investor. This stems from my year with Dean Witter Reynolds (bought by Morgan Stanley) way back in 1994 or 1995 when I had a disagreement with management you might say–I wanted to sell ‘suitable’ investments and they wanted me to push the higher commission products–we all know how that ended (I don’t screw people – there is not enough money in the world for that to happen).

When I first thought about how to pay for the not inconsequential overhead costs of running a 5000 page website I was kind of skeptical about supporting the cost with ‘donations’. Certainly some websites operate on donations, but we are fairly specialized here on Innovation Income Investor which means that our appeal is more limited than a website with broadly based security coverage.

I was wrong about doubting the generosity of people supporting our website. Kind of like some of my interest rate predictions folks have proven me wrong. Since December 2022 (when the donation page was launched) we have had donations of all sorts – from just a few dollars to $100’s of dollars and everyone of them is appreciated. We even have some folks who send a check every month to our P.O. Box. Some of the ‘paper checks’ we receive in the mail even have nice notes in them – I really appreciate that we have folks that do not participate in commenting etc., but who are newer to preferreds and baby bonds and who find value in the comments that all our ‘experts’ (not me) post.

The donations received come in very handy–in fact December is when the tech folks start sending the bills for basic operations for 2024–$1,400 which is just to keep operating online. Everyone wants a little ‘taste’ nowadays–I even have to pay for the ‘like/dislike’ button (not much fortunately). A couple weeks ago I received a note from my tech folks for their ‘retainer sale’–so I will invest some money there since security issues are kind of an ongoing thing and believe me no one does anything for less than a couple hours of billable time–when I call them I know that $200-$500 is gone in a flash. I currently pay $115/hour for the tech support.

Just to let everyone know I do not even know who gives what in support of the website. My wife takes care of that stuff and of course everyone comments on the website with ‘screen names’ so we have ‘screen names’, ‘real names’, ’email addresses’, etc. – there is no one here trying to match donations with ‘screen names’.

So THANK YOU TO ALL–to donors, commentors and even lurkers. The most important part of the website is YOU–without you all it wouldn’t be worth the effort operating this website. After 17 years of publishing this (or predecessor sites) kind words and comments make it all worthwhile!!

I had initiated my initial position on Wednesday @ $23.47 and added this new position @ $23.67–still at about a 8% yield to maturity (mandatory redemption) on 1/31/2026. My plan is to hold to maturity.

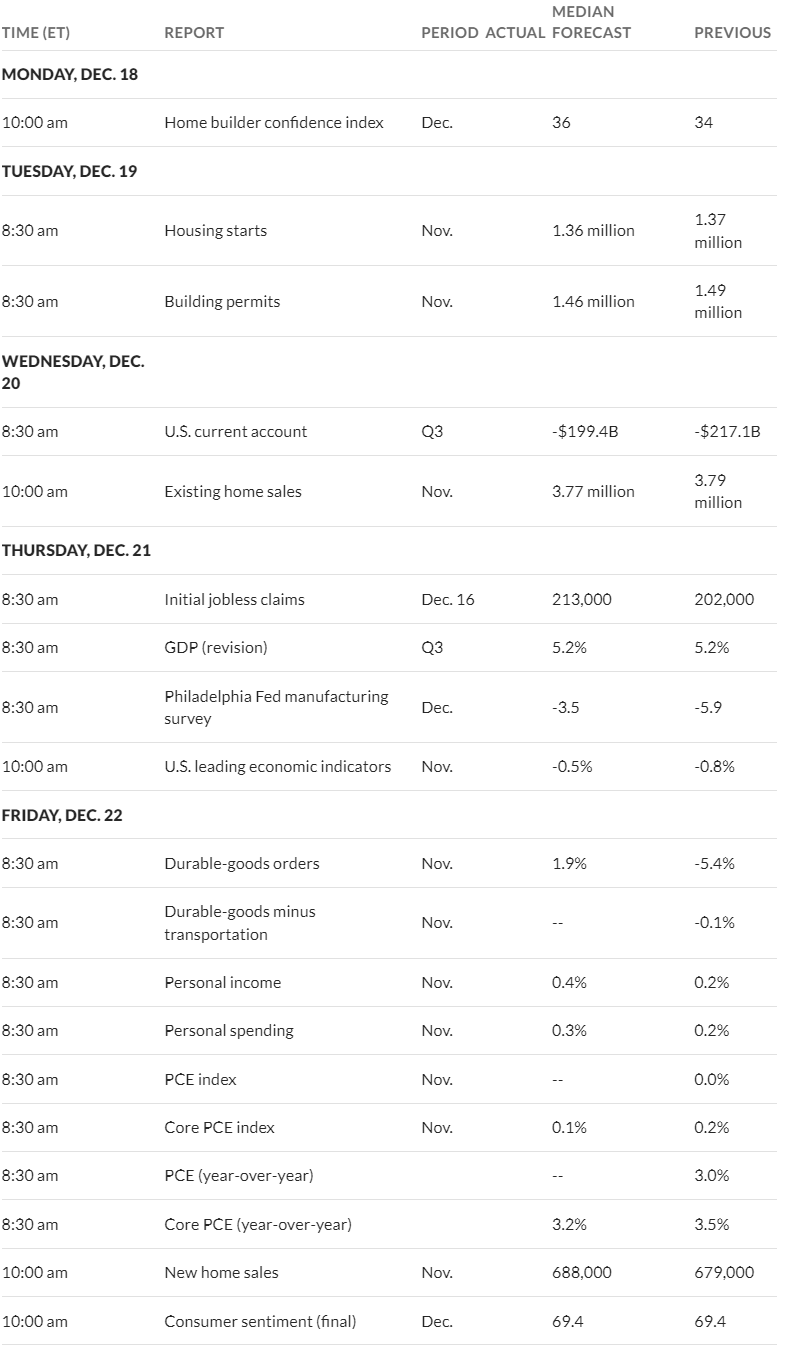

There is no doubt that this week will be ‘interesting’–everyone has to define interesting for themselves. Does it mean nothing at all happens all week as we head into the long weekend? Does it mean that interest rates plunge even further. Do investor decide we are going to have a ‘hard landing’ instead of soft? I have no real clue, although it could be quiet all week–even with the personal consumption expenditures (PCE) numbers being released on Friday–who knows?

Last week the S&P500 moved up again–up by 2.5%–powerful. The range was 4593 to 4738—finally closing at 4719. These are powerful gains–the type that make me want to be a common stock investor–I always want to be a common buyer at the highs–no thank you I’ll stick to my knitting.

Interest rates, as measured by the 10 year treasury, moved sharply lower. The 10 year closed the week at 3.93%–the range on the week 3.88% to 4.29%. This was an epic move lower. This morning the note is trading at 3.91%–fairly steady. News this week for the most part is normally not market moving (except PCE on Friday)–but one can’t predict what part of ‘news’ creates as outsized move. A lot of housing news is on tap this week so I guess we ccould call this ‘housing week’.

The Federal Reserve balance sheet grew by $2 billion last week–a departure from the normal drop–after the $59 billion drop the previous week a small drop (or in the case gain) is pretty normal. Regardless the balance sheet is down $1.3 trillion from the peak–still massive at $7.7 trillion, but a good start preparing for the time the Fed is forced to go to quantitative easing (QE)–hoping that is a long time in the future.

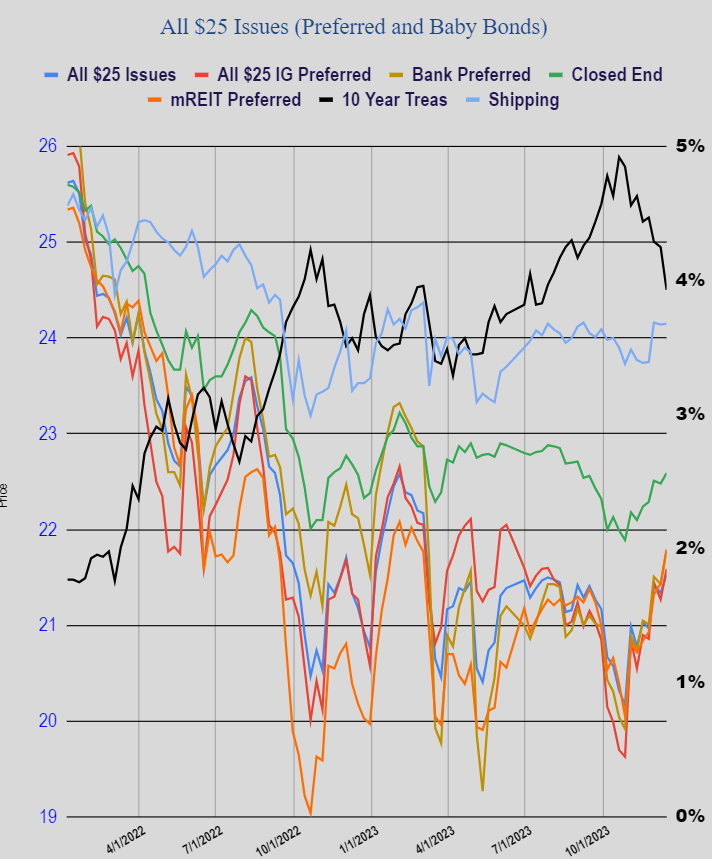

The average $25/share preferred stock and baby bond moved higher–but gains couldn’t match common shares. The average share moved higher by 23 cents–nothing to sneeze at for sure. Investment grade moved 23 cents higher, banking preferred were higher by 36 cents. mREIT preferreds moved up by 35 cents, CEF preferred were 10 cents higher and ocean shippers up by 1 measly penny. Obvious interest rate sensitive issues were the biggest winners on week.

Last week we had no new issues priced. Some (including me) are awaiting trading on the Midcap Financial 8% baby bond (MFICL). I see they registered the shares last Wednesday so hopefully we will see trading in the next couple of days.

Last night in Headlines of Interest a link to a CoBank publication on the “Year Ahead”. This 27 pages publication give their forecast for next year – primarily in rural areas of the country.

Lots of dividends and interest hitting accounts this morning along with CD maturities hitting yesterday and throughout the month I am looking to buy. Certainly the low hanging fruit has been picked, but there remains bargains to be had–assuming one believes that interest rates are moving lower for the next 9 months or so. It is likely I will add to some of my current holding, add a mREIT preferred or two, potentially add a taste of an illiquid $50/$100/share issue and maybe even go ahead and invest a little bit back in a 3 month CD –not certain on this one. I want my dry powder put to work within a week, but don’t want to do a bunch of FOMO.

Yesterday was another stellar day for preferreds and baby bonds–gains of 1% or more were very common. Each day this week our portfolios have moved to all time highs–wish I had 100% preferreds (with the benefit of 20/20 hindsight) instead of 50%. We know one can’t time markets perfectly–additionally if we look back a few years we didn’t have tasty CD rates available as an option.

The 10 year treasury is around 3.81% this morning and no real economic news we may see some drifting. Equities are flattish to a little up–at some point this will set back, but there is so much money out there in money market and CDs that we could see an absolute ‘melt up’–maybe we are seeing it already?

Well we got the Jay Powell ‘gift’ yesterday and folks are still arriving at the party. While I loved the .4% gain yesterday I wasn’t expecting another .3% today—can’t complain.

Folks are scouring for bargains–I think there remains a lot of them out them, but you may have to redefine ‘bargains’. For those that are braver than me th mREIT preferreds still show bunches of current yields in the 8-9% area--if rates continue lower these are going higher. Heck I might even get on this move.

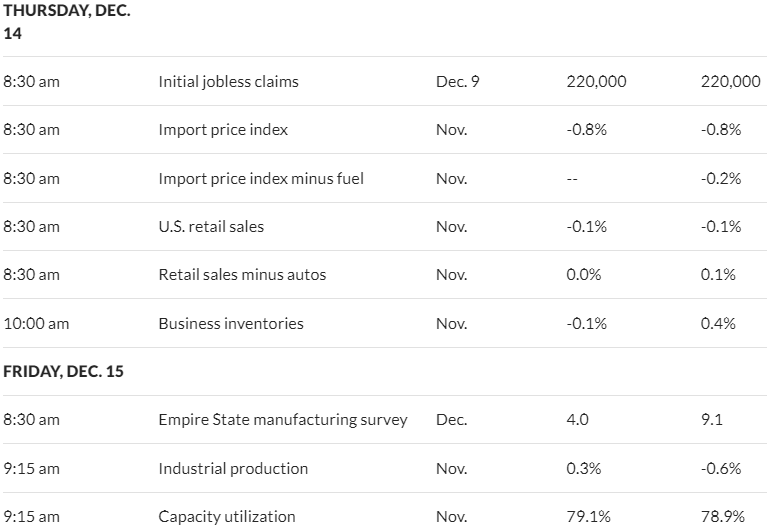

The 10 year treasury is now trading down at 3.91%–even after jobless claims that were less than expected and decent retail sales numbers. Equities are struggling just a bit–but higher. We are at all time highs—crazy—hope a soft landing is coming.

I have to thank Fed Chair Jay Powell for the nice boost in my portfolios yesterday–about .4% up (50% invested in preferreds and baby bonds). On the other hand (I’m talking my book here) I really don’t want lower interest rates so quickly–the largest chunk of our CDs don’t mature until March, 2024 so if the 10 year treasury moves lower too fast – by March a bunch of the income issues move higher will be past us. What a whiner I am – I am only going to realize 5.xx% from my CDs (poor me)- it was only less than 2 years ago that an income investor got ZIP on their cash – just have to accept one can’t time these things perfectly. Portfolios are at record highs–can’t really legitimately complain.

Right now the 10 year treasury is at an amazing 3.94% which is off maybe 25 basis points from the highs yesterday. Powell was obviously much more dovish than most folks thought he would be which set off the party in stocks and bonds. It looks like we will have a minor ‘after party’ this morning. For those that are looking to ‘lock in’ decent CD rates you can get up to 5.35% this morning on eTrade and 5.35% on Fido–these short term (3 months to a year) rates will go away when Fed Funds get cut.

Today we have jobless claims numbers and retail sales. Important to me, but after yesterdays dovish Fed move they seem less consequential–Jay Powell seems on a dovish flight path.