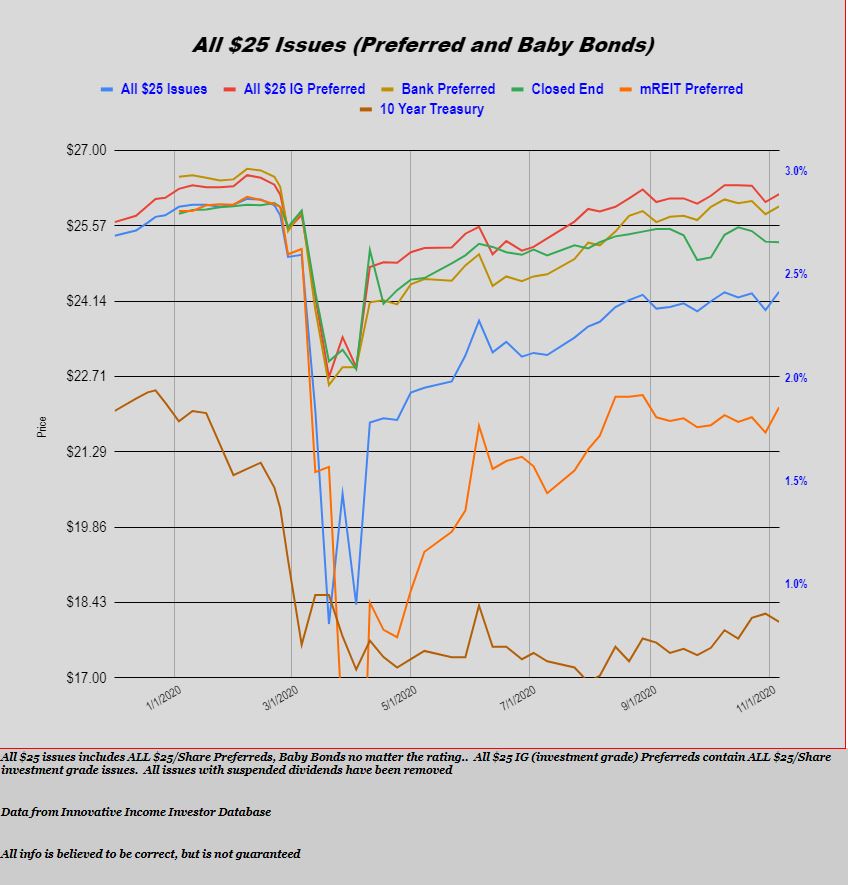

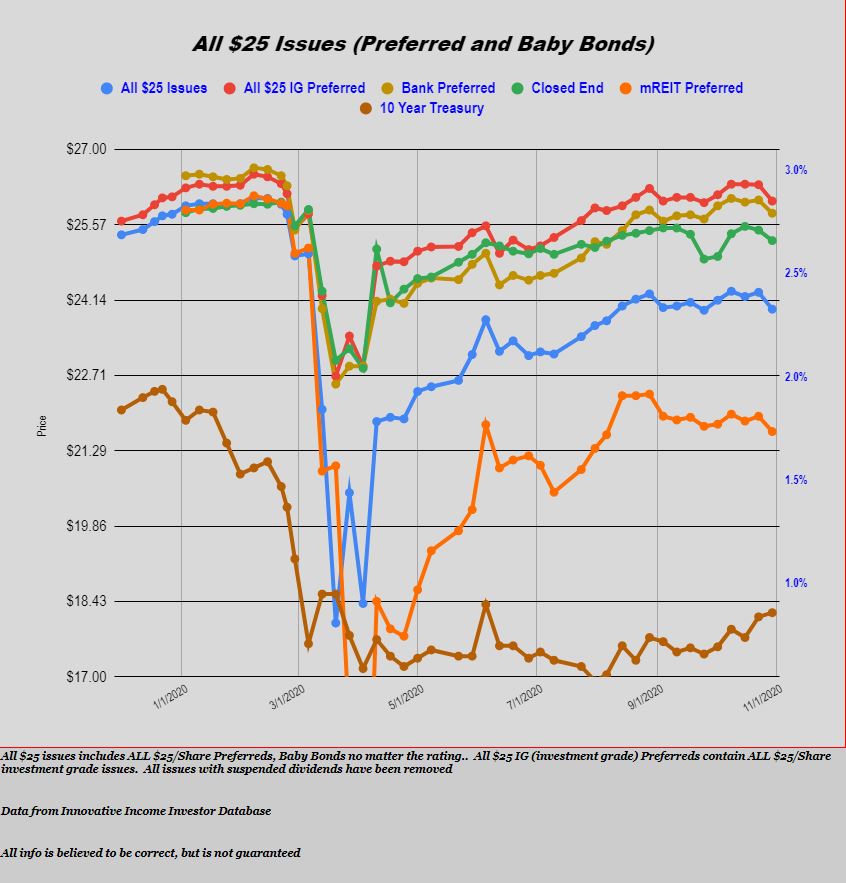

While updating the asset coverage ratios on the CEF preferreds tonight a glaring issue jumped out at me relative to the Gabelli Multimedia Trust (GGT). This CEF has 2 preferred issues outstanding.

On 6/30/2020 the trust had an asset coverage ratio of 200%–this is down from 297% on 12/31/2019. WOW–close call. The fund is required to have a 200% (or more) coverage ratio on the last day of each quarter–if not, they have a 60 day cure period after which they are required to redeem some level of their preferred shares to cure the asset coverage default. Of course we know that if they don’t cure the coverage default they are not allowed to pay dividends to common holders or make common share buybacks–not a position you want to be in when you have a declared level dividend policy of 10%.

But did you know that the fund can force redemption, at $25/share plus accrued dividends, BEFORE the 1st optional redemption date to cure a coverage default? Well they can.

Now in this instance this is bothersome-neither issue of the GGT preferreds have reached the optional redemption period yet. The GGT-E 5.125% issue is trading at $26.04 and the GGT-G 5.125% issue is trading at $26.40–they have traded at this level for a few months–I’m not sure they would have traded here if folks knew they had a potential redemption hanging over their head. Their respective optional redemption dates don’t arrive until 2022 and 2024.

You might say ‘why don’t they buy some shares on the open market?’ This would reduced the size of their portfolio while raising the asset coverage ratio–this may be possible, but up until now their policy is to buy on the open market only under $25/share and earlier in the year they did do a little buying of preferreds down in the $22-$23 area–but it was a minimal number of shares.

Data on the asset coverage ratio can be found here.

The good news is that on 6/30/2020 the net asset value was $6.14 and right now it is $7.15—so trouble was averted–for now. If Mario Gabelli was smart he would start looking to sell common shares soon–get while the getting is good Mario.

Here is my concern for this issue. Markets tumble and don’t spring back OR markets remain level and the 10% dividend eats into assets reducing coverage (over time).

Let’s see what happens here–minimally an educational study.

My source for the forced redemption comes from the original prospectus which can be found on the individual security pages linked above.