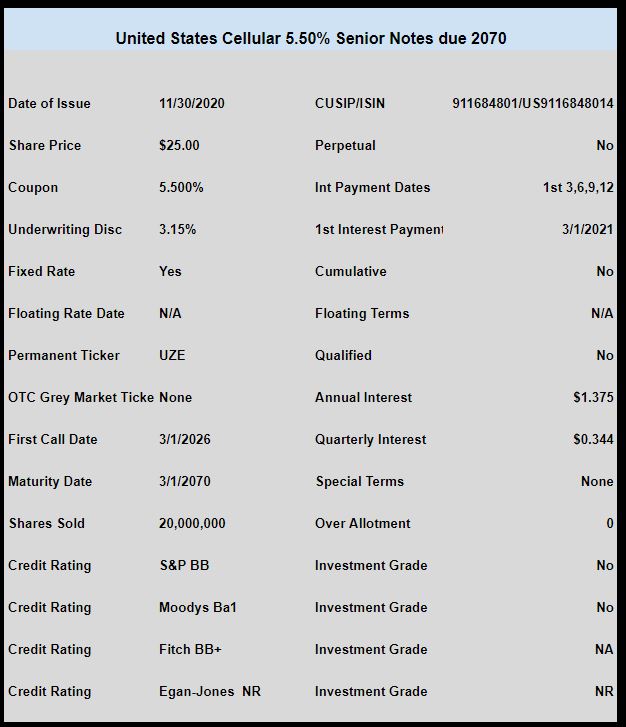

The new senior notes from United States Cellular (USM) have been priced with a coupon of 5.50%. I had personally hoped for a 5.75% simply because these fit in my current wheelhouse pretty good (just a tick or two under investment grade) so I always hope for the best.

The company is no AT&T, but the financials have been reasonable–here is the 10Q from the quarter ending 9/30/2020. Revenues are relatively flat year-over-year, while net income was up nicely. USM has been a no growth company for many years and I don’t expect that to change–on the other hand the balance sheet is strong, which is an important factor when I am perusing the financials.

The issue will not trade on the OTC grey market, but for those who can’t wait for exchange trading you will need to call your brokers bond desk.

Cellular telecom United States Cellular Corp (USM) will be offering a new $25/share baby bond.

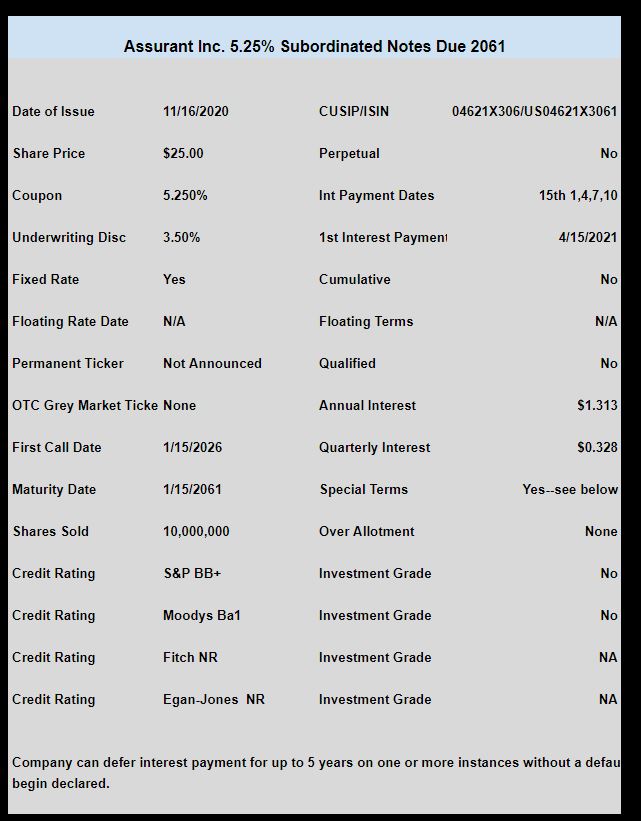

The issue will likely be rated BB by Standard and Poor’s and Ba1 by Moody’s.

The company currently has 4 baby bond issues outstanding with coupons ranging from 6.25% to 7.25%. You can see the issues here. The company ‘may’ use the proceeds from the new issue for debt repayment. It would not surprise me a bit to see the company call one of the 7.25% issues.

Once again we will have markets dominated by news of vaccines for Covid 19–we are getting very close to approval and the start of vaccinations. Once again there is no reason to believe markets will turn lower as virtually ‘all news is good news’.

The S&P500 traded as high as 3644 last week before closing the week at 3638. The index was up over 2% on the holiday shortened week.

The 10 year treasury traded in a range of .846% to .89% before closing near the low for the week.

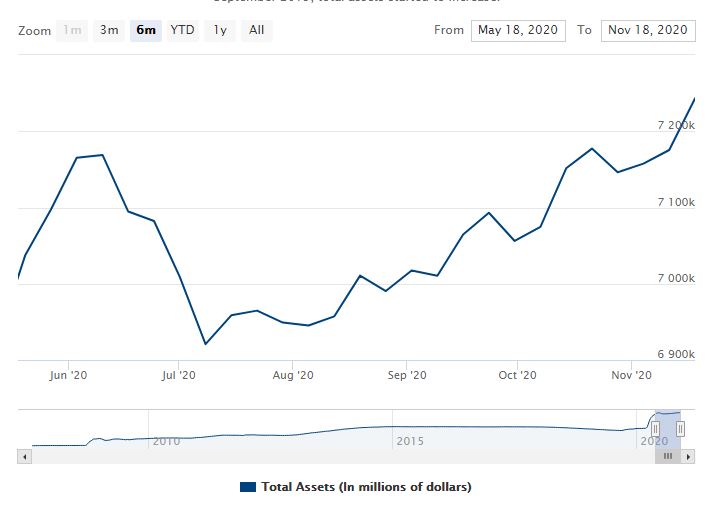

The Fed Reserve balance sheet has not been updated with the Thanksgiving holiday interrupting the normal schedule–I would expect that the balance will be updated at noon today.

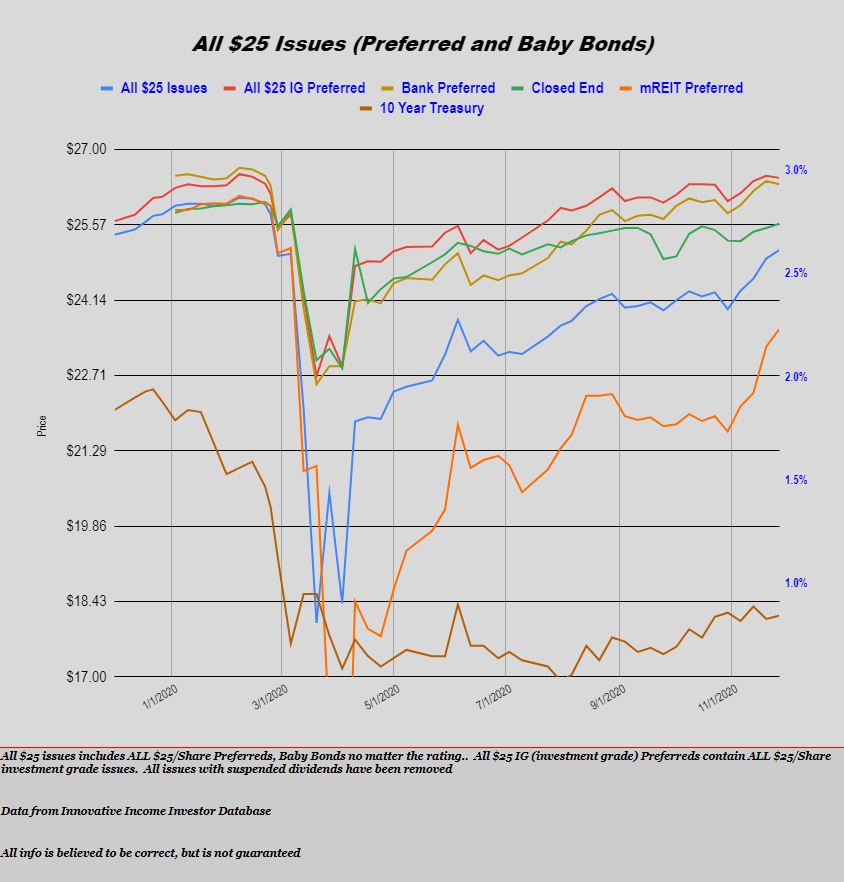

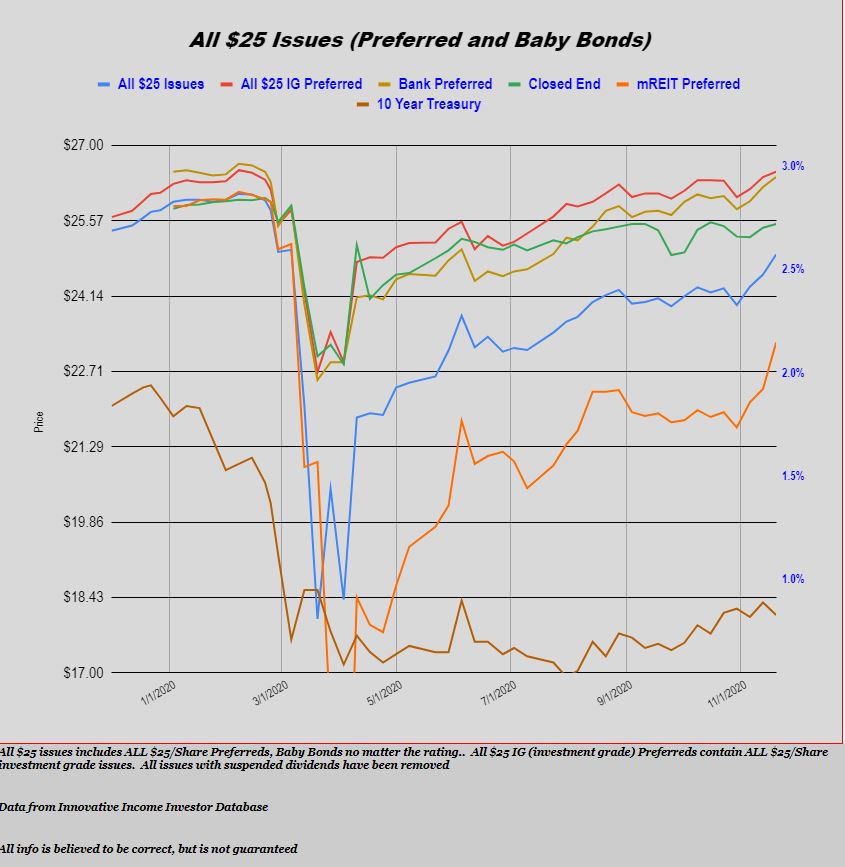

Last week the average $25/share baby bond and preferred stock moved higher by 16 cents. We continue to see investment grade issues lag junk issues–investment grade issues were down by 4 cents/share while mREIT preferreds moved higher 33 cents/share. We have seen the junk move higher for a few weeks as investors shy away from those issues with prices dramatically above $25 with low (or negative) yields to worst.

As one might expect there was absolutely no action in the new issue marketplace as the Thanksgiving holiday interrupted any potential new issue.

Each day common stocks go higher and higher–where it stops no one knows–really NO ONE.

I can find all sorts of fundamental data that would show that the never ending climb higher in equities is silly–but really who cares about fundamental data? We all know that we have a new type of investor in the market–they are young and wealthy–they think totally different.

For years one believes they have cracked the code to earning a nice 6-7% annual return–but the rules change and I am back to being as dumb as I was 25 years ago. If I was really smart I would be up 25% this year instead of hoping I can reach 5% If I was really smart I would hold nothing but speculative equities that have no earnings, but they have sexy names. Oh well not to be–I feel good about staying the course of working to get that 5% (or maybe 6-7%) year after year through conservative investing.

In the Monday Morning Kickoff this week I wrote “I wouldn’t bet on a stock market tumble now”. In spite of the silliness in stocks 2 key indicators point to higher prices.

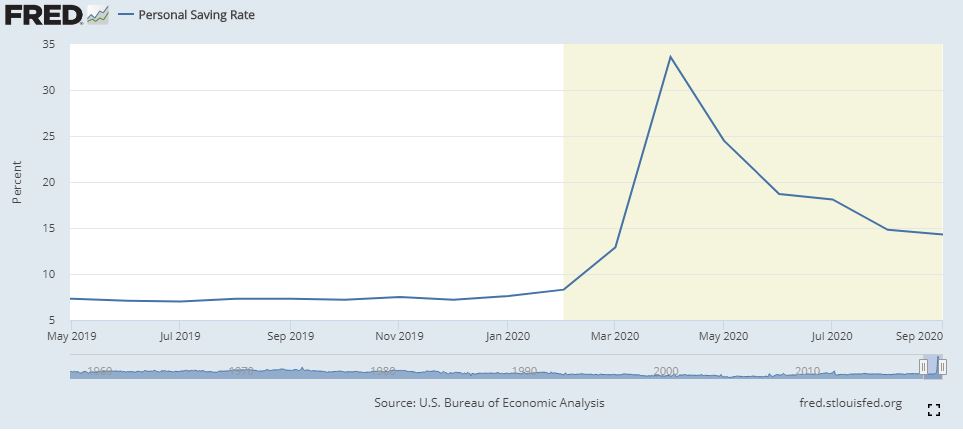

I have taken to watching the Fed Balance Sheet as well as the Personal Savings Rate (let’s call it PSR).

The Fed Balance Sheet is going higher and higher–now at record levels. While the balance sheet took a dip in June it is now rising steadily as the FED buys all the excess assets that they can sop up. Now whether I agree or not with the FED policy it matters not–as long as the assets are moving higher they are manipulating markets to where they want them–interest rates and thus equities.

Now I being to look at the Personal Savings Rate–the definition being personal income less outlays for expenses and taxes.

You can see that the normalized level on this chart is around 7%, but in March it started to sprint higher with helicopter money flowing freely–peaking out at 33.6% in April–wow. Now the drift lower begins and now we are at 14.3%–still a huge increase from the norm. To say that the consumer is well ‘funded’ right now would be a huge understatement.

So the question is simply will markets continue higher with the FED manipulating interest rates and with the consumer having more cash than they know what to do with? Will the party continue until consumers get back to the normal savings rate? Or will it continue until that ‘black swan’ shows up one day?

Kicking off another week with some trepidation as states around the U.S. go into various forms of ‘lockdowns’. In Minnesota bars and restaurants and fitness centers will again take the brunt of the economic damage as all of them have been ordered to shut down for 4 weeks–and who knows whether it will be 4 weeks, 8 weeks or more.

The various shut downs and economic damage will be battling with the vaccine news for headlines–I wouldn’t bet on a tumble in stock markets now – a surprise stimulus package could send markets steeply higher–along with interest rates.

Last week the S&P500 traded in a range of 3544 to 3629–closing the week at 3558 which is a loss on the week of near 1%.

The 10 year treasury drifted off .82% to .92% before closing the week right near the .83% level—it looks like the 1% level won’t be breached this month.

The Federal Reserve balance sheet took a giant sized jump moving higher by $68 billion. The balance sheet has again reached the largest balance ever–big surprise.

Last week the average $25/share preferred stock and baby bonds rose by 1.5%-a pretty large jump. The mREIT preferreds lead price higher with a jump of near 4%. Banks were up just 1/2% with investment grade being up around 3/4%. Obvious folks are moving into the lower quality issues because those are the few issues that are trading below $25.

Last week we had 4 new income issues price.

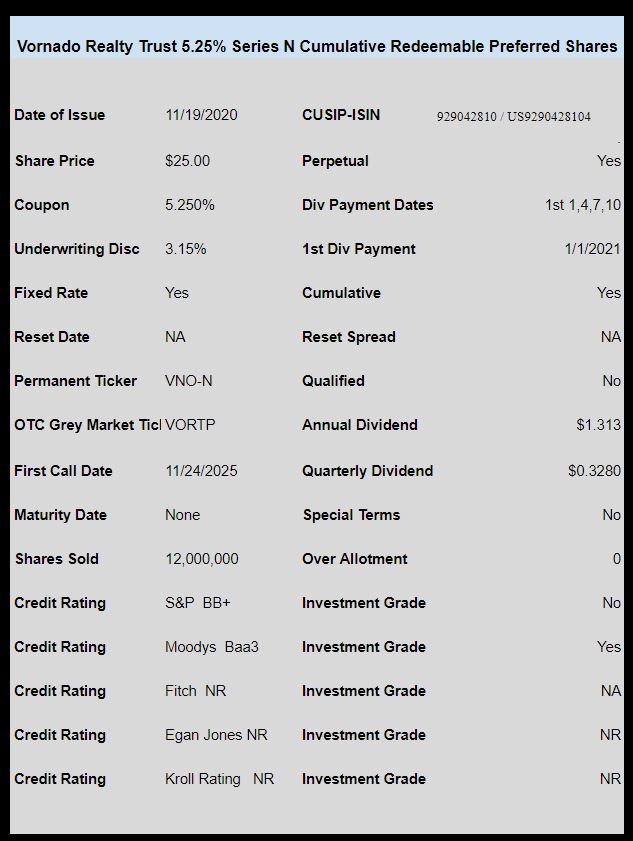

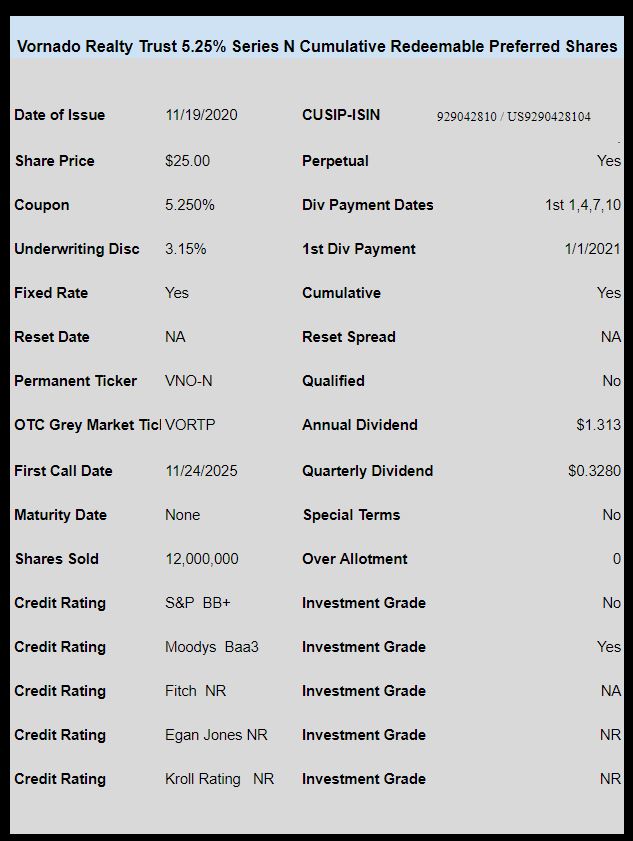

REIT Vornado Realty Trust (VNO) priced a 5.25% perpetual preferred issue. The issue is trading on the OTC grey market under ticker VORTP and closed on Friday at $25.10.

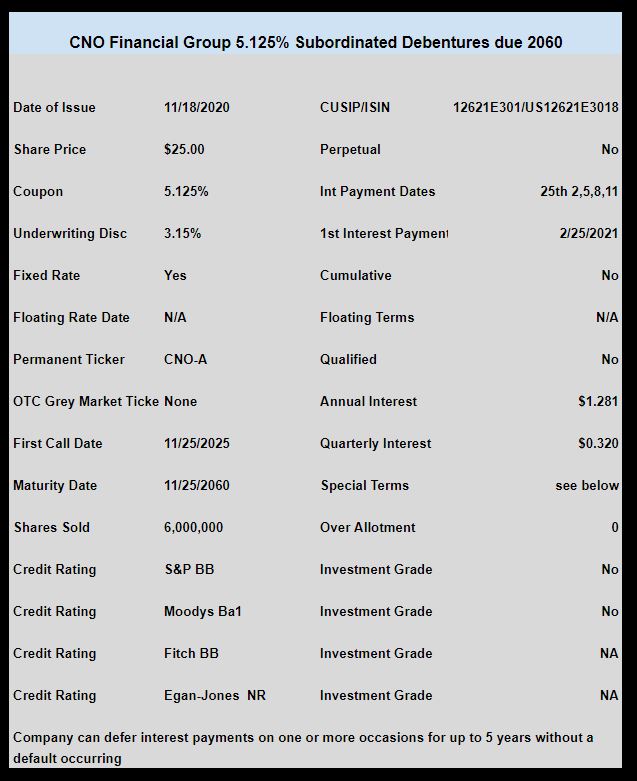

Insurance company CNO Financial Group (CNO) priced a issue of baby bonds with a coupon of 5.125%. I have not seen trading take place in this issue as of Friday–would guess it will trade this week.

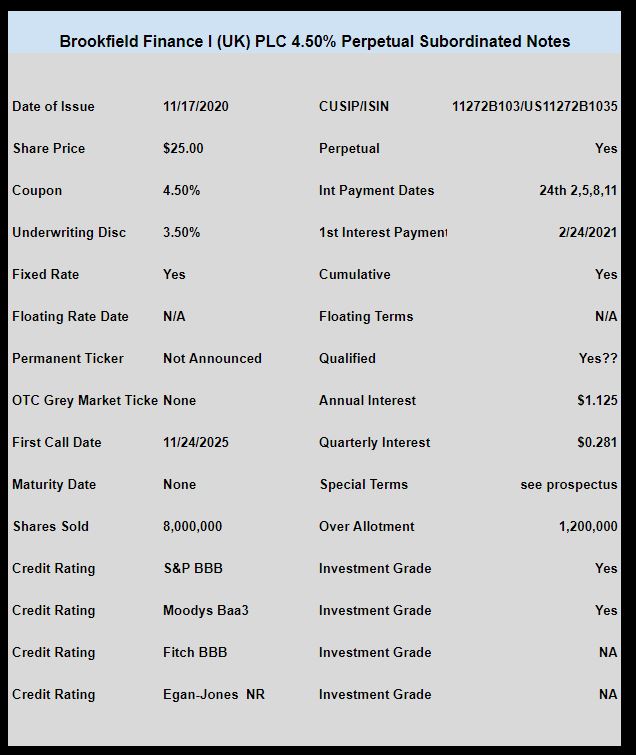

Brookfield Finance I (a division of Brookfield Asset Management) priced an investment grade issue of baby bonds with a coupon of 4.50%. No trading has taken place in the issue.

Insurance company Assurant (AIZ) priced a new issue of baby bonds with a coupon of 5.25%. This issue is below investment grade. The issue has not traded as of yet as far as I can tell. Expect trading this week.

As noted by mcg below the OTC ticker has been announced as VORTP.

Vornado Realty Trust (VNO) has priced the previously announced new perpetual preferred stock.

The coupon is 5.25%.

The issue is cumulative, but non-qualified for preferential tax treatment.

The issue is split investment grade–being BB+ per S&P (a notch below investment grade) and Baa3 per Moody’s.

NOTE–this issue is large enough to call the VNO-K 5.70% issue, but the company has reiterated that the proceeds will be used for ‘general corporate purposes’. Just the same one never knows.

The issue will trade today on the OTC grey market, but the temporary ticker has not been announced.

Office REIT Vornado Realty Trust (VNO) will be selling a new issue of $25 preferred stock.

The terms of the issue are typical–cumulative, optionally redeemable in about 5 years and non qualified.

The company has 3 other issues outstanding, 2 of which are currently redeemable with coupons of 5.7% and 5.40%. The company has NOT signaled an intention to call these, but one can never tell. Neither issue has much, if any call risk built into the price.

I believe this issue will be split investment grade–Baa3 by Moodys and BB+ from S&P.

Insurer CNO Financial (CNO) has finally priced the previously announced new issue of baby bonds.

The issue will carry a coupon of 5.125%. The issue is rated below investment grade by Standard and Poor’s at BB and Moody’s at Ba1. Fitch rates it at BB as well.

There will be no OTC trading so if you need to have it prior to exchange trading you will need to contact your brokers bond desk and use the CUSIP to potentially purchase.

Brookfield Finance I (UK) PLC, a Brookfield Asset Management (BAM) company has sold a new issue of $25 subordinated notes. These notes are fully and unconditionally guaranteed, on a subordinated basis, by giant asset manager Brookfield Asset Management Inc.

These notes will be listed on the NYSE and will pay quarterly interest payments.

NOTE–this is not a typical baby bond–in fact from my review of the prospectus it is more akin to a cumulative perpetual preferred than a bond. There is no maturity date, but the optional redemption begins in 2025

I believe the interest payments will be treated as dividends–and likely qualified for income tax purposes, but this is not a certainty.

The company may defer interest payments without being in default.

If you are interested please read the pricing term sheet and the preliminary prospectus, but which are lengthy documents. Some of the folks have been discussing this issue on the Reader Alert Page so one might look there for additional details.

The Gabelli Healthcare and Wellness Trust (GRX) has announced they will be calling the only preferred they have outstanding.

The 5.875% GRX-B shares will be redeemed on 12/24/2020 for $25 plus 35.9 cents of dividends accrued.

The various Gabelli funds have been redeeming issues by selling shares in the trust–versus doing a ‘re-fi’ with a new preferred. Essentially they are selling shares at high prices–shrinking the size of the trust and reducing leverage–seems like a smart move.

The shares which had traded as high as $27 or so in October are now trading at $25.33–falling about 55 cents from yesterdays close.