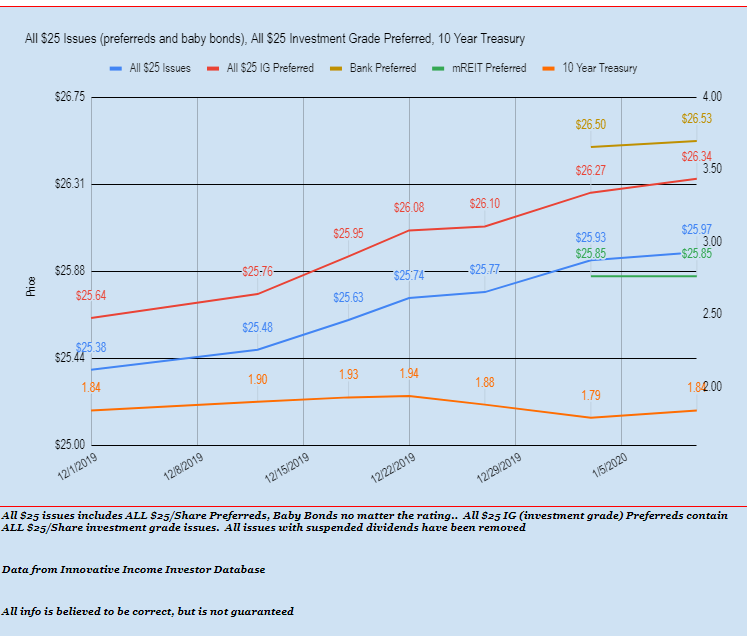

NOTE–I INVEST FOR THE LONG TERM WITH 60-70% OF AVAILABLE FUNDS–MORE IF I COULD FIND ACCEPTABLE RISK/REWARD. BELOW IS SOMETHING I DO ONLY FROM TIME TO TIME AND IT CERTAINLY IS NOT SOMETHING I ENCOURAGE FOLKS TO DO.

Tomorrow has the potential to be a good shopping day for those looking for potential ‘flip’ candidates.

Tomorrow (1/14) we will have 47 preferreds and baby bonds going ex-dividend–this to add to the 11 we had go ex today–a total of 58 issues today and tomorrow.

Folks that are looking to ‘flip’ (buy and hold for a short period–for me less than a month with hopes of a 1-2% gain) an investor MAY find it beneficial to buy on the ex-dividend date or within a couple of days as some issues tend to bounce back quickly from the “mark down” applied to share prices by the exchange to recognize that the shares are trading ex-dividend (without dividend).

The way this works is you had to own shares TODAY to receive the dividend/interest payment in the future–buying it tomorrow (the ex date) is too late for the current payment. The exchange that the shares are trading on will ‘mark down’ the shares by approximately the amount of the dividend–thus if the shares closed today at $26, but goes ex tomorrow for 50 cents the share price should open around $25.50 Tuesday.

Of course, in real life, the shares may be marked down by the ex amount, but never trade at that price. Shares could immediately move higher–or occasionally they will continue to fall further.

Some folks may ask “why go to all the trouble”–“why not just own it on the ex-dividend date and capture the dividend”? Certainly we have many investors on this website that do just that–they “buy and hold” for long term–and in fact that is what I mostly do–have a base of positions that I have held for years. Unfortunately because of low interest rates and high prices we have too much cash on hand.

Because of having too much cash on hand and no long term prospects to buy at this moment I resort to doing some ‘flipping’–many times of issues I don’t want to hold long term–in fact some I want to hold maybe a month at the max. Normally this is because the issue I am flipping is a lower quality issue that I am comfortable holding for years, but think I can squeeze 1-2% out of in a month or less.

So right now I am studying the list of issues going ex tomorrow and seeing which may have potential for bouncing back quick–most of the time determined by looking at the chart and secondly by determining how much in favor a sector has been lately. Once I pick a target issue I will watch it and when it looks stable in price I will make a buy–my intention is to hold until a 1-2% profit is realized–hopefully I will be out in less than 1 month.

Additionally I have an interest in shares that are in the early call period and trading at $25 plus accrued. For instance a favorite of mine is from insurer WR Berkley (WRB) and is a 5.625% subordinated note (WRB-B). The baby bonds have been callable since 5/18 and it is likely they will be called soon (or maybe not). WRB sold baby bonds at a 5.10% coupon recently so we know it would be advantageous to call the WRB-B. This issue has been a favorite of mine, but is currently at $25.80–and the dividend is only 35 cents so I sold my shares a while back at a nice gain. It is possible that the shares will be marked down by 35 cents tomorrow, but continue to fall since it should be obvious to everyone (at least anyone paying attention) that they are risking 45 cents by holding longer. If the shares were to continue to fall I might have an interest–but not until $25.05 or so.

Now it is too late to do what I call a “capture and flip”, but essentially it is capturing the dividend/interest and then waiting for upward movement in the share price and letting it go. You might notice that many issues start to move sharply higher 1-2 weeks before ex date as folks clamor in to capture the dividend. Then the issue is marked down by the ex amount and on ex dividend date immediately begins to move higher again. This can provide delicious gains when it works out–as much as 2-3% in a month.

Now FORGET EVERYTHING ABOVE!! These are extraordinary times–flipping, capture and capture and flip have been like “shooting ducks on a pond”. While we watch common stocks go up and up and I complain–honestly flipping etc has never been so easy. THIS WILL NOT LAST FOREVER! At some point I will have 2-3 flips in process and something will go wrong with interest rates etc and I will lose money on the flip. There are no guarantees in life–nor investing, but until it no longer works I will be doing some of it.

HERE IS THE MASTER LIST WITH EX-DIVIDEND DATES.