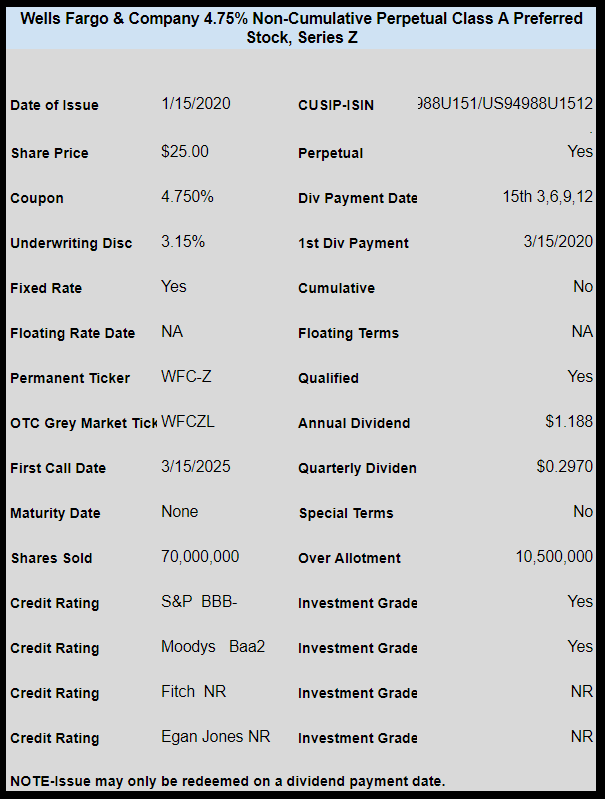

Wells Fargo & Co (WFC) has priced the previously announced new preferred stock.

The company will sell 70 million shares with a coupon of 4.75%. There will be 10.5 million shares available for over allotment.

The issue will be investment grade, non-cumulative and qualified.

The issue will trade immediately on the OTC Grey market.

The pricing term sheet can be read here.