I see MarketWatch has a headline of “Panic Selling Reached in the Stock Market”. Markets are off less than 2%–not sure any of us that were invested on Black Monday, 1987 would call the current fall a panic.

I am watching preferreds and baby bonds closely–and actually the average price is up 2 cents since yesterday. There are wiggles – plus and minus 1% in some issues, but that is true everyday.

What I am specifically watching for is the ‘baby getting thrown out with the bath water’–so far the baby is safe. Obviously this could change–but we need a real panic–multiple days to make that happen in a big way.

For the newer investors–take a deep breath–go get a coffee and resist doing anything crazy such as going to all cash–this too shall pass.

Common stocks are slipping by about 1% today as the corona virus takes it’s toll. I think VinL hit the nail on the head in some comments that it is really about uncertainty in China as their information may well be less than transparent and of course stock markets hate uncertainty.

The 10 year treasury has slipped again and is now trading at 1.53%. With uncertainty in the markets yields are likely to slip some as folks like to move to a safer position–or at least what they think are safer positions.

We note today that the U.S. airlines are starting to announce suspensions of service to China with Delta leading the way–others will follow I am sure. We’ll see how far these various disruptions go–and then try to discern whether there will be GDP effects.

I am not seeing any real disruptions in the preferred and baby bond markets. There have been quite a few ex-dividend issues yesterday and today (35 issues more or less), but they have not put much of a damper on prices–on average.

One item I have noted that in recent weeks it is becoming more difficult to try to successfully do a dividend capture. While the ‘capture’ part is easy enough the security exit part is getting much more difficult. My personal idea on a dividend capture is to buy the issue around 2 weeks prior to the ex-dividend date and then hold through the date and look to exit within a couple weeks with a net 1% gain. For instance I bought the B Riley 6.75% baby bond (RILYO) earlier in the month to capture the 42 cent interest payment. Shares went ex dividend on 1/14–and I received the interest payment today. I am now looking for a bounce back in share price but thus far nothing–nothing at all. The bottom line is that I am up by a number of cents–but far from the net 25 cents I am looking to garner. Whether this is simply an issue of being B Riley or one of buying the wrong issue (they have 6 baby bonds outstanding)–or simply not entering soon enough I have no idea–but one gets used to ‘easy pickings’ so when I have to wait to exit I get ‘antsy’. Oh well I will just hold the issue for now.

January has actually been a decent month overall. I always have a modest goal of 7%/annually–and really would be most happy if I could get to 6% this year. Depending how markets close today January should be a gain of around .6-.7%, which would be plenty acceptable to me—I am sure others have done better (and some worse), but as we all know we all have different needs and styles when it comes to investing–not necessarily anything right or wrong–just what works for us.

Last night and early today I thought “it looks like a down day” in stocks (based on futures and early trading)–I think all of this was related to the corona virus, although maybe it was a delayed reaction to the FOMC not giving common stock traders and investors anything new to trade on at their meeting yesterday. Whatever the reason I guess the clowns decided it was time to drive prices up at the end of the day and we closed up by .3 or .4%.

On the other hand the 10 year treasury wasn’t buying into the stock move as it closed almost 4 basis points lower–again. Whether the corona virus reduces growth globally or not is a total crap shoot at this point in time. No one can claim to know the answer to this at this point in time–honestly we have huge numbers of flu cases each year and literally thousands of death (37,000 estimated in the U.S. last year) from the flu–I could go on and on, but it is just silly. Not that we shouldn’t take the corona virus seriously, but a little common sense would be helpful.

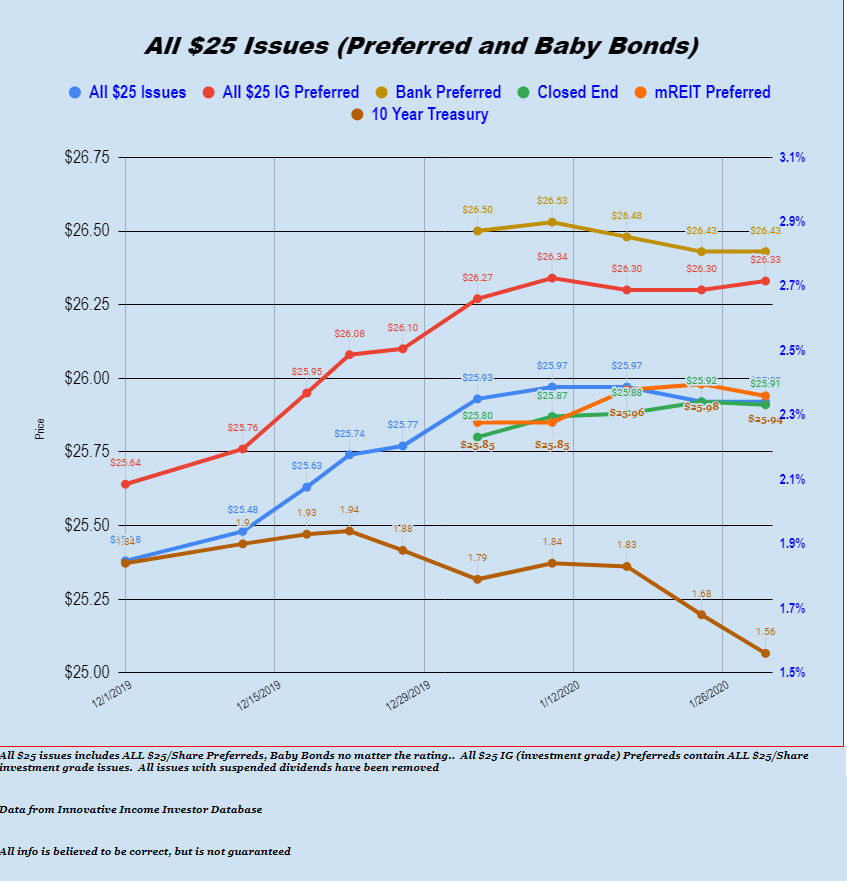

Anyway, let’s take a look at how preferred and baby bonds have done for the week thus far.

You can see from the chart below that it has been really quiet–prices seldom moving, on average, more than a couple pennies week to week.

The grand total movement of the $25/share preferreds and baby bonds tracked here (661 issues) has moved exactly ZERO since last Friday. mREIT preferreds are off 4 cents and investment grade preferreds are up 3 cents since that time.

Note that the 10 year treasury is almost 30 basis points lower than 12/1/2019. This is what makes income securities interesting. It isn’t always true that higher rates drive prices lower while lower rates drive prices higher. That is a big–maybe–sometimes–it depends. More than pure interest rate movements go into pricing these securities–as the chart above shows prices moving sharply higher while rates were a bit higher and are totally flat while rates are tumbling.

Obviously there have been ex dividend dates this week and that always sways the number a penny or two–but all in all this is extremely ‘Goldilocks”–and for some of us we like it quiet. On the other hand there are more active preferred stock traders like Martin G. who would like the see more movement so they can take advantage of the volatility.

One thing that is almost certain–as soon as all of us get lulled to sleep an ‘event’ will occur which will wake us up quick. We shall see what the weeks ahead bring.

We still have a little confusion on posting of comments on the website.

Any commentor can start a new thread on any page/post by going all the way to the bottom of the page. Sometimes that is a long way down (i.e. Sand Box Page, Reader Alerts etc) but if you are on a laptop or deck top computer (that rules out Gridbird) you can hit your ‘end’ key and it will take you to the bottom of the page.

To Summarize–It is NOT necessary to alway just do a ‘reply’–by going to the end of the page you can have your post show up on the top of the comment section.

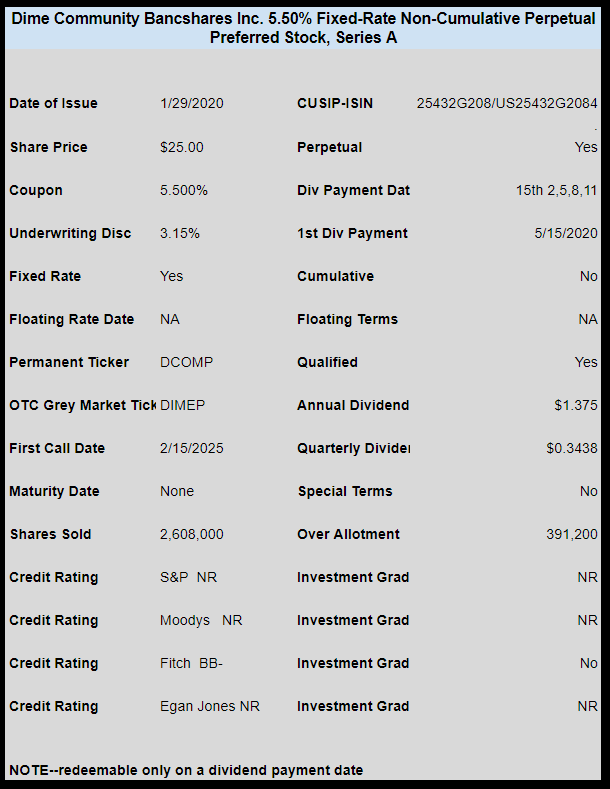

The coupon is 5.50% and the expected rating by Fitch is BB- (speculative), but regardless investors are jumping all over this new issue from Dime Community Bancshares (DCOM) as it opened for trading around $25.40–and now is at $25.45.

This just goes to show how hungry investors are for yield–and these smaller banks have traded pretty decent in the last year.

I think this issue may trade similar to the new Triton International 6.875% issue (TRTN-D) where yield hungry investors bought it up on day 1 as it opened the 1st day on the OTC Grey Market at $25.28 (on 1/17), and is now trading at $25.38–lots of initial excitement and then a more muted response.

For myself personally I have no interest in jumping into this initial fray on the OTC Grey Market at these prices. Only at a much lower price would I have any interest at all–even with plenty of cash in our accounts this coupon simply seems to meager for a small banking company–although the issue will do fine as long as the economy remains decent.

Dime Community Bancshares (DCOM) has priced their previously announced preferred shares.

When I saw this coupon I thought I must be having a bad dream–actually I said “holy shxx”. 5.5% on a small community banker with a junky BB- Fitch rating. Well I guess the market will speak and since buyers seem to be hungry I’m sure the issue will be trading at $25 right away. ON THE OTHER HAND if buyers would reject the issue and trade it down a buck maybe I would have interest.

The issue is non cumulative and pays dividends on the normal quarterly schedule with an early optional redemption available in 2025. Shares are redeemable only on a dividend payment date.

Shares will trade OTC Grey Market immediately under temporary tick DIMEP.

Brooklyn based community banker Dime Community Bancshares (DCOM) will be selling a new issue of non-cumulative perpetual preferred shares. The issue will NOT be investment grade.

DCOM is a relatively small banking company with total assets of just $6.3 billion so this offering will be interesting relative to pricing.

DCOM has posted a presentation on the company which can be read by interested potential investors–it is here.

This issue should trade on the OTC grey market, but no ticker has yet been announced yet.

I have added a new topic in the right hand side menu for “Sock Drawer” discussion.

The intent it to include items that all of us consider “sock drawer” holdings.

My definition of “sock drawer” is those issues I own that I consider extremely safe and that don’t have to be watched too closely. Normally they would have more modest coupons, but you can sleep well at night (relative to safety)–you know the income stream is extremely safe, althought the share price may move around quite a bit.

Others may have their own definition–in fact I know they do–that is fine

For instance, I have held the Tricontinental 5.00% preferred (TY- or TY-P) issue for years and years. Tricontinental is a closed end fund managed by Columbia Threadneedle. TY was formed in 1929 and this small amount of preferred stock is the only leverage the fund uses–2.2% leverage. Because it is a CEF they must maintain a 200% asset coverage on the preferred stock–the last time I calculated the coverage it was over 4000%. This is a $50/share issue and last traded at $54.66. The issue is callable anytime at $55/share. Shares were issued in 1963.

You can use the link in the right hand menu to access this section–it is here.

NOTE–the COF-P 6.00% issue was callable 9/1/2017 and almost certainly will be called. It was trading around $25.60–now at $25.37. The issue is only redeemable on a dividend payment date.