November was not only a stellar month for commons stocks, but preferreds and baby bonds fully participated in the rally.

The average $25/share issue closed the month at $21.27–which is up from 10/27/23 by $1.10/share – a gain of 5.5%. While many of us that had a large allocation to treasury issues and CDs couldn’t fully participate in the rally certainly the gains we garnered were pretty spectacular—2-3% in a month is nothing to sneeze at.

Can December be as good as November? I highly doubt it – but honestly if interest rate fall by another 50 basis points it could happen. It sounds silly but if you would have asked 100 investors if we would have seen the drop in rates we have seen recently 99% of them would have said ‘no way’. So who knows–I will be happy with flat rates with a portfolio gain of 3/4% in December.

Yesterday we had personal consumption expenditures (PCE) released and the inflation numbers shown were right on forecast – no surprises to speak of as we head toward another FOMC meeting on 12/12 and 12/13. While I am all about getting all the data in I think we can call December another ‘no hike’ month, but with continued warnings that ‘we stand ready to hike rates if necessary’.

For today I doubt I will do anything–as always my ‘dry powder’ is limited–my December maturities in CDs don’t occur until 12/15/2023. I did generate some dry powder yesterday by nailing down some profits with the selling of the Hennessy Advisors 4.875% baby bonds (HNNAZ), although I still hold some shares. So I am looking to buy, but have not pinned anything down.

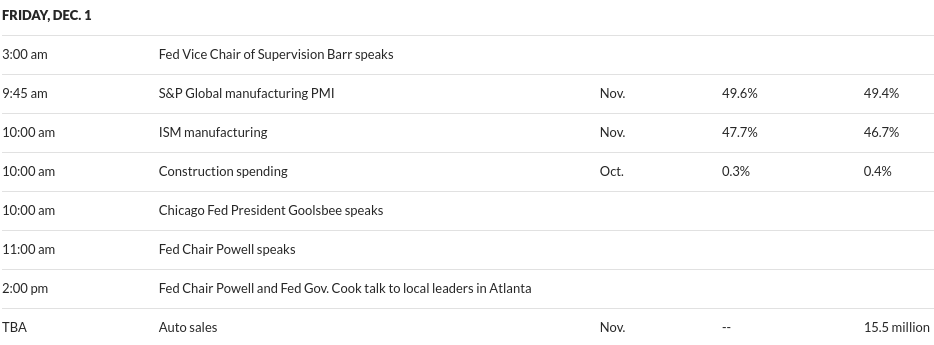

Interest rates are up a few basis points this morning–equities are off a little (the S&P500), but none of the moves are meaningful and certainly mean nothing for the balance of the day. We do have some minor economic news and Fed Chair Powell speaking today.

I’m up 8.6% this year and was up 3.8% last year. 23 month return calculated from 1/1/22 is 12.3%. While many have done better this year, eking out a gain last year was great. I can live with a 6% annual return over the past couple years considering the still negative market return and the historic rise in interest rates, Excluding cds and bonds, my largest holdings are AIC, ATH-E, CHSCL , CKNQP, ET-C & D, All-B, TRINL, OXLCM & P, SCCB & C, XFLT-A and EP-C.

CKNQP floats 1/1/25 @ 3mo libor plus 3.744%. Cobank will likely call the issue and at the current $96.49 price I’d buy more if I wasn’t overloaded. I hope they don’t pull an “MS-E.”

Not a bad yr, even with quite a few dogs, managed to be up 9.3% so far this year – surprisingly. Still around 50% dry powder ( making interest over 5%), mostly waiting, but a couple nibbles in last week or two.

Very excellent Fary – you have lots of dry powder and the challenge now is to find a home for it, but we continue to have nice money market rates while you find your target.

Oops the name should be Gary. Typo

I also dumped a boatload of the PRIF-K I bought 10 days ago for $19.70 at avg of 20.58 today. Not a bad annualized return and I wanted to roll into something more stable.

My preferreds income account is up 15.7% for the year with more than 1/3 of that coming in November. I worked awfully hard this year to moderate losses in order to get to this point which I knew would come eventually. Hopefully, there will be much more if rates ease more.

Now it’s time to finish off tax loss harvesting. to cut out some of my Uncle’s cut. I wouldn’t be unhappy if there was a pull back from EOY tax selling.

Great job Theo – hanging in there has its rewards.

Theo,

Likewise up nicely this year…BUT.

Still mghtily in the hole from most things bought in 2021 and before.

Issues like AHL/E AXS/E BFS/E ENO EPR/G GRBK/A KTBA NCZ/A TDS/V WFC/L

Anyone else out there still down more than 15% on these and similar if you bought back in the good/bad old days when they were close to par?

This month felt good, but we need many more months like it. May be wishful thinking…

But I continue to hold, and main thing is they continue to pay.

Adrian, yes I am more of a buy and hold type of guy, and in the same investment camp as you. I do have some that I have bought several years ago and am down 15%-30% in those investments (not adjusted for the years of dividends/interest though which helps ease the pain). KTBA, UEPEP, AXS-E, PSB-P, NSARO, CRLKP, CNLPL. The time in the market is what is most important to me as the annual income is getting close to 2 annual salaries.

I have 12 years to go to retirement, and will have 2 pensions, SS, and will have the forced RMDs. They can go up/down along with a few hundred other investments, and for the most part I dont care, as I dont use any of the income. I do like to play with about 30% to make some fun out of it, which does juice the returns. Last Nov/Dec, last Spring, were some great times to throw money at the large downturns of the fixed investment area.

Nice – you can retire now, it seems! I am retiring from NASA on Jan 12th. I just turned 64, have a pension, SS and investment income and will bring in more (by about 20%) than I have now while working and I live very comfortably now as a GS-15. My pension and SS will easily pay my bills but, won’t outlive me. But, my savings will and, I won’t need to touch my principle, in fact, it should grow nicely as I’ll only be sifting off some of the income on those accounts for “playtime”, travel and a nice bottle of wine or three every year. Then my daughters can fight over it when I exit stage right!

Looking forward to retiring and maybe doing some freelance work in local history research and staying as far away from “rocket science” as I can (at least for awhile).

Adrian, I should have mentioned that I worked even harder last year to end up down 1% for the 2022 (I short preferreds during the downdrafts). So my current 15.7% is about 8% per for 23 months. Not spectacular but I can live with it given that my net cost is much lower than par. Given that I’m retired, I appreciate the better than the bank additional income plus, I need a hobby!

Picked up a Truist (TFC) 2.5% coupon bond maturing 8/1/24 with a 5.85% YTM/YTW – CUSIP 05531FBH5. I am figuring this is similar to an 8-month CD making about 5.8% (though granted, no FDIC protection).

If that appeals to you yaz, you ought to look at the Tim favorite, RMPL- It’s due 10/31/24 and at 24.87 has a YTM of about 6.80%. I suspect it’d be considered even less risk than Truist though not rated. With more current yield to boot, I’d suspect it would officially be lower duration too..

Will look at it – I have a lot of dry powder still as all kinds of stuff matured last night, and coming up for 12/15 and 12/31. It sounds like my kind of investment. The Truist bond is pretty small potatoes for me just trying to keep the cash load working. I did roll into some treasuries with a big chunk too.

Wow, what a nice year end rally. Everything is green and sentiment is bullish, and markets are probably near a couple year high for some indexes. I have sold about 30% and rotating back into pinned to par investments such as WFC-R, MS-E, … I need to increase my quarterly estimate to uncle sam again. I was not expecting this rally and surge. It was sad to see the large amounts I had invested in energy, gas, utility go. Ex. Was cool to get my hands finally on DUKB for example, but like many of them they took a ride on the elevator up and fast.

Mr. Conservative – sorry you can’t garner sympathy for making too much money–lol.

Don’t want to jinx my luck, but one account is up roughly 7% counting received income and withdrawals for the year. Feels like I have a part time job though. for how much time I put into it.

NICE! You made me check – I’m close to 9% with three diff accts at 8.4%, 9.5% and 10.7% – The largest one by far is the 8.4%. Looking a LOT better than last year when I was down something like 10-12%

yazzer you ever go to the casino and when you win your wife reaches over your shoulder and takes some of the winnings and puts them in her pocket?

Hahaha – no. Gave up on wives after two of them. I am still very good friends with each of them however. Makes it great for the kids and grandkids. Current GF is not about getting married – just about companionship, drinking good wine and an occasional trip out of town. She hasn’t reached into my pockets yet but there’s still time and she’s 17 years my junior so she may outlive me!

Just got most everything situated for 2024 (but still have a good amount o maturities coming in Dec) and I am right at an effective yield overall of 6.50% A lot different than last year as well! Happy Holidays!

Yaz friend of mine told me last week about a sale. Only about 280 cases made of a Petite Syrah by Warren Winiarski the original owner of Stag’s Leap Winery. When he sold Stag’s Leap he kept 2 acres his cab won the 1976 Paris wine tasting. Needs a little air time.

oh my! My GF and I just got back from a two week trip to CA (I live in southeastern MD) – Napa, Sonoma, then south to Monterey and Big Sur and the Santa Lucia Highlands. A wine lover’s dream. Plus we got to go whale watching which I had never done before. I love the Stags Leap petite sirah! I have a couple good decanters for said aeration!. BTW, I have a pug here at home with me and her name is Zinny Pug Sommelier. Zinny stands for Zinfandel…hahaha.

I usually gravitate towards the pinot noirs cuz I love cherries! But chards and a good cab are always in my cellar along with some syrahs and zins…when I retire in 41 days, I’ve got some good Ridge Monte Bello cabs from 2006 and 2010, some Kosta Browne and Kistler pinots, a couple French burgundies from 2008 and even a bottle of 1977 Boal madeira (the year I graduated HS). It will be an epic party!

Yaz, you hit all the good spots. If you like Pinot then next year plan a trip to Oregon. Best secret I can tell you is look for festivals if you don’t mind the crowds. The wineries get together and one ticket will usually get you access to dozens for just the price you would pay for tasting at 3. Oregon still is not on the map yet except for some well known wineries. It’s so slow there in the winter months a lot of smaller wineries close their tasting rooms. Best time is March when they open back up and the crowds are scarce. Southern Oregon where Harry & David is, the Pear orchards are getting ripped out and planted to grapes.

Here, Ridge Lytton Springs makes good Zin about 2-1/2 miles outside of town. Mazzocco just down the road makes good zin and has summer music on the lawn, bring your own picnic and I like the prices better. I like Cab’s and NZ SB.

Oh now you got me started, should be over in the sandbox.

We are now considered “Wine Country” here on the California Central Coast. From Paso Robles 40 miles north of me to Santa Ynez about 40 miles south of me ( I am in Arroyo Grande) lots of wineries. Seems a lot of my running races are at wineries these days. Last one was just a half marathon race at Cali Paso winery in Paso Robles, overall winning man and woman won their weight in bottles of wine.

I also know the Central Coast very well. For many years I would fly from N.C. to attend the Central Coast Wine Classic down at Pismo/Shell Beach. It was ALWAYS an affair to remember. Archie McClaren was the founder. I knew him well. He was a great advocate for the region and was on KCBX.

Unfortunately, Archie passed away a while back but the memories remain.

Yazzer, ha, same boat here. Not getting married again and GF of 17 years now lives with me. And yes, when she retires in 3 years, she will definitely be reaching into my pocket, that is certain. But she knows she cant go reaching with both hands as the pocket isnt that big to begin with!

Will not mention your Napa trip as all that will do is cause her to try to get me to spend more money as she really wants to go there. She is just going to have to wait for Napa as we already are going to Tahoe in January to ski. That is enough $ spent for time being!

I saw your 6.5% effective yield. I find irony in that as mine is roughly around there too. And it was right around there during zero interest environment too. But I rotated a lot into CDs which anchors it down, and I am fine with that. I have had a great year up a smidge over 19%. A large part of that was first 4 months of the year and Uncle Sam will be claiming a fair bit of this as I was a STCG trading machine this year. While I am very pleased with results, actually was more satisfied with last year 2022 returns of 7%. As that was a landmine year for a person who is always 100% invested in income issues and no common stocks.

Next year is going to be handicapped taking the full brunt of so many CDs and such. And its going to get a tiny bit worse as I am committing myself to buying 20K more of those 1.3% fixed IBonds, ha.

Grid: Up 7% in 2022 and 19% this year. Those are stellar returns for an income account, given the difficulties of the past two years. I doubt that anyone is surprised by your superb performance.

Theo, last year I cheated a lot and got away with it. I gambled that some issues like BKEPP and CNIGP were going to eventually get called (and stay solvent of course, ha). I had thousands of shares of CNIGP for example. And I was buying any chance I got with these as the gamble paid off. I was buying most of the CNIGP in the $26-$28 range for quite a while knowing if NY PSC approved the buyout I would get $29.70 if memory serves. They did finally after a year or so. If they hadnt I was stuck considerably overpaying for a $20.75 par 4% yield that would have matured in 2026.

BKEPP I dumped even more into that one. I knew the scoundrels were taking that thing under and I just traded and clipped a few coupons until it was done. Also bought floaters and call anchored. Any time I tried my hand at a fixed perpetual I like anybody else got my hand slapped, so I just quit trying.

This year it was mostly made first 4 months and last 6 weeks constantly trading. All issues of same relative quality and same sector ilk will rise and fall in tandem over time. They just dont do it daily and that is where trading gains occur to arb out the differences or exploiting volume dumps or buys.

Just knowing the proper arial interest rate direction is the key. I preferred getting income in the ZIRP environment because you didnt have to worry about interest rate direction. It wasnt going any where, ha.

Rolled some of the outsized funds that matured overnight back in treasuries (June maturity for 5.32% YTM/YTW). Eyes on some preferreds and corporates too. No hurry but doing the DD.

Quite a wild ride yesterday, I think it was Bear or Maine who said to expect some swings in share prices with end of month and they were right. Now what do these mutual funds and ETF’s do now that they moved prices on stocks and preferred right at end of the day? will we see sales today to lock in those temporary profits?

Charles–a little give back would not be unusual–I am fine with that as long as it is minor–no reason to expect more than that.

I sold some shares of SCE preferred yesterday, be glad to buy back at a lower cost.

I wouldn’t mind a pull back in the market even if the accounts gave back all the gains for the year. At my age it’s more important the income keeps coming in. I still have about a 1/3rd of my wife’s account in money market funds will low ball bids sitting out there. she’s happy. Same with my Schwab account about a third in cash. I added to the Fido account this week as it was about 90% invested.

So far celebrating Xmas early.

Have to agree with Charles. Plus I can add one more negative to this upswing. It’s going to raise my RMD for next year. As I get older, quantity and quality of my income stream become more important than the bottom line. The bottom line is a concern only for my heirs.

Jersey mostly trying to find the right price for the income and safety and I take a little higher risk to get a blended yield. Most of my selling was to lower my overall cost or if I had a full position I would do some flipping. The other sells which were not really a sell was holdings that got called.

Good example of one that I was flipping around a core position was the NYCB-U actually wish I had kept more but 1% to 3% maybe 5%max I feel comfortable with. Holding about 61 positions and about half I don’t even think about.

Jerseyvinny,

Sounds like time for you to start spending their inheritance! Enjoy it while you can.

I have been telling my kids for their whole lives that my life goal is to have the last check I write bounce.

I guess I don’t really mean it, but I hope it has helped motivate them to be more self reliant.

I thought that too, Tim, and it started the day that way. However, by the EOD, everything had held up and even added to yesterday’s winnings. Interesting week, for sure.