Last week was another decent week for investors of all sorts – including income investors.

The S&P500 moved higher from the previous Friday by about .8%–not a rocket ship, but plenty decent for a week.

The 10 year treasury moved lower in yield – by a bunch – closing down 25 basis points to end at 4.22%. The chatter now is about rate cuts – do they come in the 1st quarter of 2024 or do they hold higher for longer with cuts until the last half of the year? At what point do domestic and global buyers of U.S Treasury debt signal enough is enough?

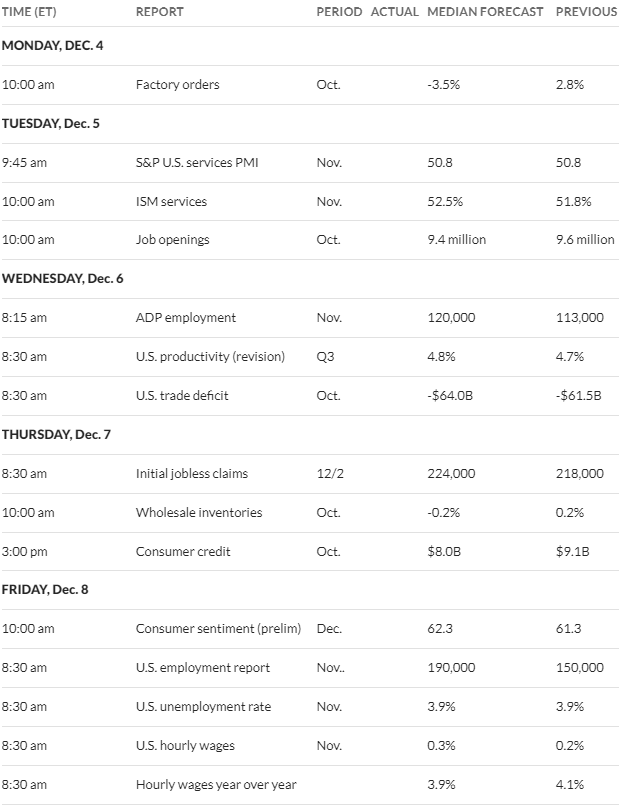

Last week we had the personal consumption expenditures inflation gauge released–and all was as forecast. That was the biggest piece of economic data last week. For this week we have employment numbers for November being released on Friday–certainly the Fed would like to see softening numbers–at least under 200,000 new jobs being created. A move up in the unemployment rate to 4% (from 3.9% last month) would be something the Fed would like-no doubt.

The Federal Reserve balance sheet continued lower with assets down by $14 billion in the last week. We now stand at $7.796 trillion.

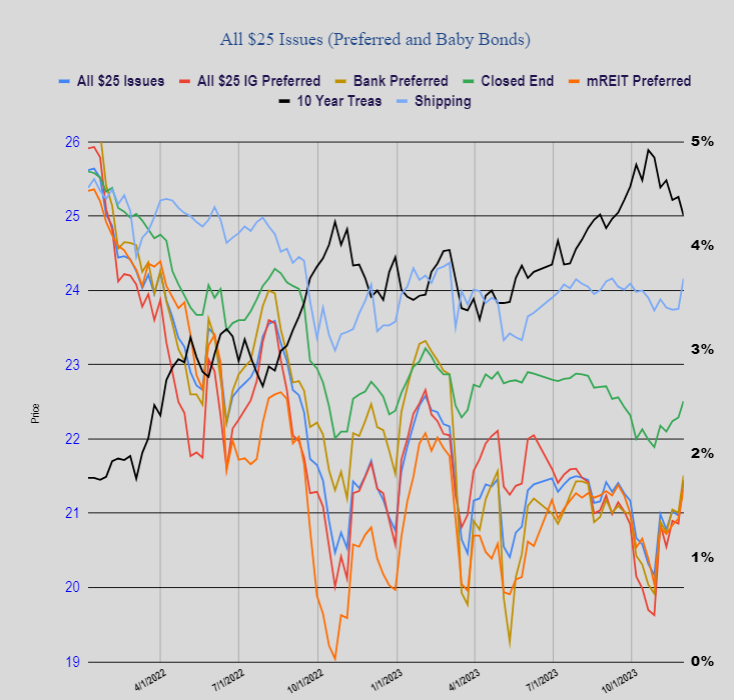

Last week the average $25/share baby bond and preferred stock moved nicely higher last week as by 45 cents. Investment grade moved 59 cents higher, banks higher by 50 cents, CEF preferreds by 22 cents, mREIT preferreds by 39 cents and ocean shipper preferreds were 40 cents higher.

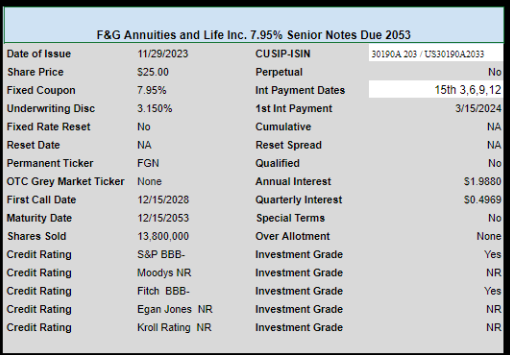

Last week we had 1 new income issue priced. Annuity provider F&G Annuities (FG) priced a new issue of 7.95% baby bonds which are investment grade. I see no trading in the issue yet, but would expect it late this week.