Over the last month or two I have seen it mentioned that some folks believe that the fixed to floating rate issues might work well in a rising rate environment.

No one should forget that the ‘hedge’ against rising rates is based on 3 month Libor–not on long term rates (i.e. the 10 year treasury).

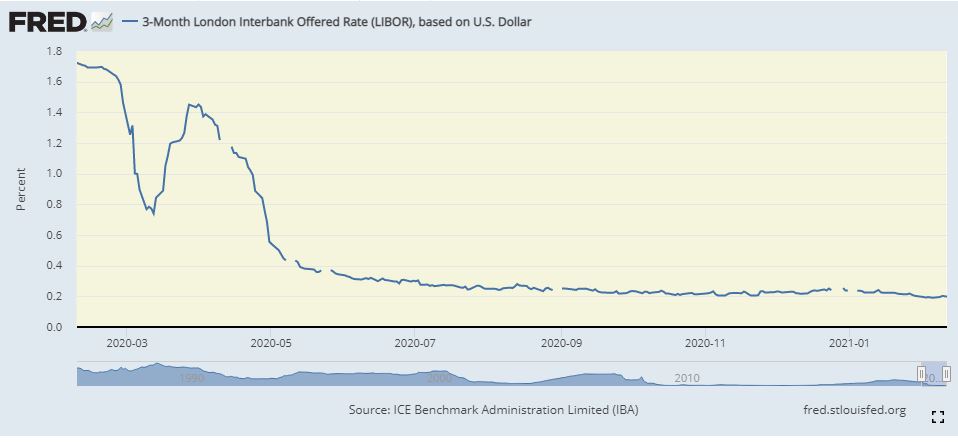

Here is a chart of 3 month Libor going back a year — note that 3 month Libor hasn’t risen–in fact is falling a bit now. Obviously the yield curve has steepened greatly as short rates remain low while long rates surge.

So the point simply is that at this point in time we don’t want to assume that 3 month Libor (or some replacement rate as Libor is going away sometime in the future) is a great help looking out into the future.

The good part is we don’t have many issues flopping over to floating rates anytime soon–just 4 issues in 2021 and 3 of those are Customers Bancorp (CUBI) issues.

You can see all of the floaters and fixed to floating issues here with the ‘potential coupon’

Great thread here at III. I am prone to learning the tools and accurately seeing the trend rather than looking for a lead. Good to be challenged.

The only thing I will add comes from my accurate or not-quite-so accurate understanding:

Seems “sentiment” has been bent by the Fed Propaganda that “(short) rates will be lower, for longer.” It’s going to take one hell of a loaning spree for bank capital to get multiplied into the economy or sit at SOFR/LIBOR and the crap instruments built on that ‘neutral index’. The Fed gets to control Interbank lending ledgers and capital requirements, but not lending. It’s going to take a boom in the economy for banks to leak lending out in a general fashion. Good luck. THAT is why this economy will persist for a long term. During that time things will change like the dollar and global capital demand. We are seeing that now; EXTERNAL, global ledger system friction.

Also, the advice here is good to go for the brokerage that supplies what you need. The bond desk at TD is either a ‘quote and execution on the phone now’ or “we will give you a call back to execute”. I have NEVER gotten a call back OR gotten a fill from their bond tool order system.

Comment: Blockchain Bulletin Board Technology could easily transplant the brokerage/bank itermedidaries now and WILL probably happen at some point.

There is NO reason (except power/control via regulation…haha) for an antiquated, opaque, corruptable and uncompetitive ledger system to persist.

As is so often the case when I’m reading these pages, a giant penny just dropped: If the floating rate for a given issue is defined as a certain base rate (my uninformed term) plus 3-month LIBOR, and if 3-month LIBOR goes negative, that will lower the base rate, correct?

For example, per https://www.sec.gov/Archives/edgar/data/1488813/000095015916000721/customers424b5.htm when CUBI-F starts floating on 15 dec 2021, dividends will be payable “at a floating rate per annum equal to three-month LIBOR … plus a spread of 4.762% per annum.” Which means if 3-month LIBOR goes to, say, -0.1%, the effective coupon would be 4.662%, correct?

Read the relevant prospectus. Some issue put a floor on LIBOR and some put a floor on the whole rate.

But, yes, in many cases one could, in theory, end up with a negative rate. LIBOR +500 isn’t likely to go negative but LIBOR +30 is a distinct possibility.

Tim—thanks for this info. I can’t see 3 month libor going negative anytime soon so it makes sense, at least to me, to look for f2f issues with base yields that look pretty good relative to new issues. As long as you don’t pay a premium (above $25) for higher yield ones which might be called, it’s a good place to invest some money in the short to intermediate term. Am I missing something?

Going out on the yield curve you have 5-, 7-, and 10-year resets. There are plenty of them in the institutional market (buy through IBKR for best pricing) and a handful on the exchange traded markets. Plus all the Canadian 5-year resets.

But almost all are richly priced and YTC is low. So even these won’t be very good hedges in the current market. 446150AT1 is a great example that I bought last May. It ran from 100 to 119 and the YTC is down around 3% as a result.

https://www.sec.gov/Archives/edgar/data/49196/000119312520153202/d937284dfwp.htm

If you’re out for true inflation hedges you need a different approach.

Bob – Is trading in the institutional market limited to big dollar trades?

Institutional trading …….

There are minimum quantities yes but in most issues I look at it’s a small number. I have been able to buy 5 shares at a time ($5k face) almost any time I’ve gone to enter a bid. The minimums are set by the bond dealers not the brokerage and will change with time.

Thanks for the info on this. Right now I’m trading bonds and preferreds on Fidelity and Etrade, getting frustrated along with everybody else with low yields, and would like to broaden my reach. I’ve never been on IBKR, do they require anything special to access the institutional market?

Coaster – If you’re trading bonds with Fidelity or ETrade, you already have access to the institutional market, similar to IBKR. I think to generalize, the “institutional market” is differentiated for the sake of discussion as the market for bonds that have $1000 denominations as opposed to the baby bond market which is most frequently $25 denominatiosns and almost by definition is NOT the institutional market. So you can buy in the institutional market via Fidelity’s Fixed Income Dept or Active Trader Pro platform even though you might not be buying in what might normally be considered institutional amounts, which broadly speaking is usually considered to be a minimum of a 100k “round lot.” As you probably know, you can see the minimum amounts available to buy in each of offerings Fidelity shows you and I believe you only have to pay $1/bond on any trade no matter whether you buy 1k or 50k… They used ot have a minimum charge higher than $1, but I think they’ve dropped that. I think they also cap the amount you pay for lots above 50k. Accurately speaking this means Fidelity is acting as a “broker” on your transaction, not as a “principal” with the difference being they get paid a set amount per bond per transaction as opposed to them selling you a bond at a price that’s been marked up to include a commission that could be just about anything. Acting as a broker levels the playing field for you as opposed to them acting as principal. IBKR acts as a broker as well.

Incidentally these days, the baby bond market is much cheaper than the institutional bond market.. That’s why many baby bonds are being refunded by companies by issuing bonds in the institutional market these days.

No, just a regular brokerage account. Sign up for a simulated money account, use the Webtrader platform, go to “new order” and “bond”. You will need a CUSIP. 21871NAA9 Try that one for fun.

Trading institutional issues at IBKR lets you enter your own limit bid, buying or selling. That is the big difference with the other brokerages with which I am familiar that require you to take the bid (if selling) or the ask (if buying). The bid/ask can be quite wide and can make 100-200 bps difference on a round trip.

Agree many brokerages require you to either take the bid or the offering, but not Fidelity… With them you can set your bid or offering just like you can create a limit order on stocks or baby bonds…. What you can’t do is set a minimum amount you’d be willing to execute. In other words, if you have 25k to sell but you’d be willing to have someone buy 5k of your offering if that’s all a buyer is willing to buy, you can’t do that and that 5k order might execute away from you even at a higher price than you’re willing to sell.

I have accounts at Fidelity and TDA. I never use TDA for exactly the reasons JOel points out.

Thanks all for your detailed responses to my question. I didn’t realize that I was already in the institutional market, so no new frontiers of fixed income to explore…..

A typical purchase for me is about $5K of bonds, which costs $5 at Fidelity or $10 at Etrade. I appreciate Fidelity having removed their minimum fee, which remains at $10 at Etrade. Yes, the ability to set my own bid price & quantity at Fidelity is nice and I do use that feature, but in today’s exuberant market I haven’t had much luck with it since the sellers don’t seem interested in negotiating.

I agree that the baby bond/preferred marketplace has better pricing now than the bond market. It also has more volatility, which can open up fleeting opportunities as well. I’m still keeping an eye on the bond market but only buying in baby bond/preferreds, almost all call-risk securities where yields can be higher but very short term. I see that the 10-yr Treasury is above 1.35% as I write this, perhaps rising rates will eventually push up corporate bonds to better rates. It would help as well if the Fed would stop buying corporates. As they say, “don’t fight the Fed”.

I did not know that about Fidelity as I don’t have an account. If you’re going to participate meaningfully in the institutional market you really want to be entering your own bids, not accepting the bid or ask. The bond dealers are thieves. The “spread” on most issues will knock 30-40-50 bps off the yield.

I pay less vigorish than that in my DraftKings account

I can only agree with you. However, when I want to lock in yields for 10 or 15 years the best place to go is the bond market. Baby bonds/preferreds just keep being called away.

But, in today’s markets, I’m just scratching in the dirt for yield, like everyone else.

Tim, Libor vs 90 day T bill rates? About the same for the past year? I am concerned that t bill rates will be become a “political “ issue as The American fiscal budget becomes increasingly unable to pay any increases in rates on the tens of trillions in short term treasury bills. Low interest rates will become less of a policy option and more of a political necessity. Is Libor set by a political body?

LIBOR is rigged (oops, I mean set) by a group of banks. The good news is we’re shifting from Libor to SOFR as the basis for everything. SOFR is determined by the free market. The bad news is that SOFR tends to be a little lower than LIBOR.

Very true. SOFR is an overnight rate and a secured rate so, by nature, is going to run lower than LIBOR. I believe it’s sitting at 6 bps. The new Enbridge floater is SOFR based and has no rate floor, not even at zero.

LIBOR is going to look like the good old days I’m afraid.