Just a couple updated items for Oxford Lane Capital (OXLC).

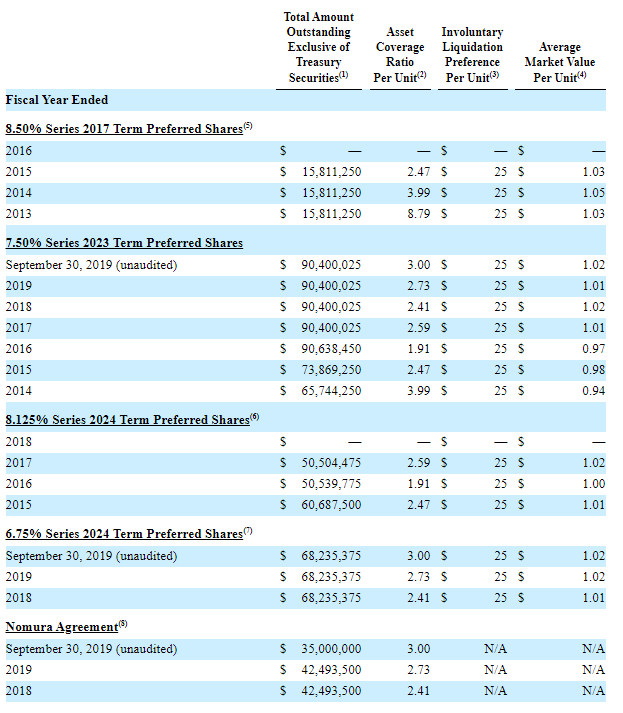

The leverage ratio for the company is claimed to now be 300% by the company as of 9/30/2019.

The number of shares outstanding of the OXLCO 7.50% issue was 3.6 million as of 9/30/2019. This issue was originally 800,000 shares with 120,000 over allotment—They have sold millions of shares since the offering in 2013. OXLC is the king of ‘at the market’ selling–both common shares and preferreds.

Data below is from the offering prospectus of the new issue.