UPDATE/Correction–dividend is monthly at .1302/month–1.5625/annually.

Oxford Lane Capital (OXLC) has priced their previously announced term preferred stock issue.

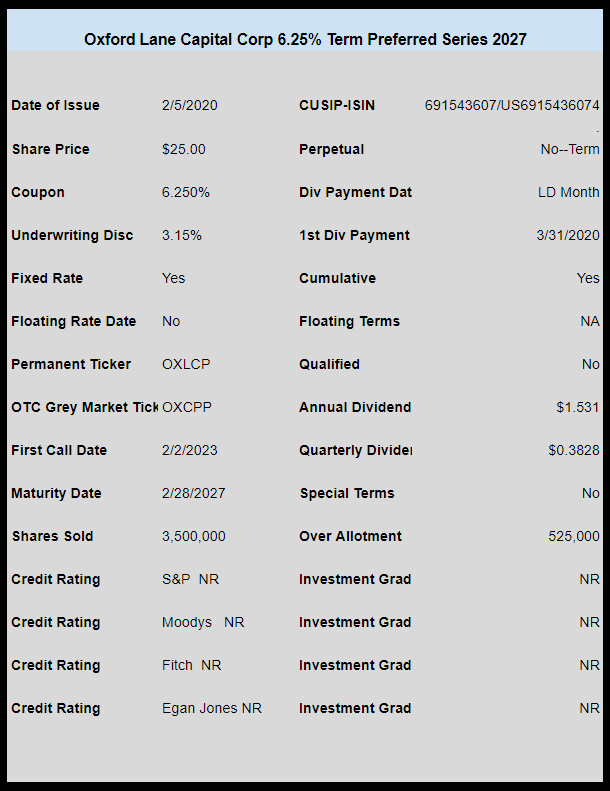

The issue will carry a fixed rate coupon of 6.25%, will be cumulative, but non qualified. This issue in unrated.

The company plans to use the proceeds and to possibly redeem some of the 7.50% OXLCO term preferred. The new issue is 3.5 million shares plus an over allotment of 525,000–this is enough to call all of the OXLCO issue if desired.

The issue trades immediately under OTC Grey market ticker of OXCPP.

The pricing term sheet can be see here

Thanks to Nomadicmist, Fabrib and Steve all of whom were right on top of this announcement and within 1 minute of each other in posting.