Almost every business day we have Fed speakers–you know the folks–the ones that had no idea that interest rates were too low a year ago and missed the obvious (which almost all of us knew). They are the ones that say they are ‘data dependent’, but yet every day shoot their mouths off about what they will do in a few months. Give me a break!! Are you data dependent or do you simply like to hear yourself talk?

Anyway Fed folks Bullard and Williams shot their mouths off yesterday–stocks tumbled but the bond market yawned. Almost without doubt these Fed officials are ‘pleased’ when stocks tumble – whatever. Eventually markets will turn a deaf ear to these clowns–see them as the buffoons they are. I think the bond markets have them figured out already–yawn.

I see the futures markets are up a bit–mostly meaningless of course. The 10 year treasury yield is at 3.65%–steady as we go–perfect.

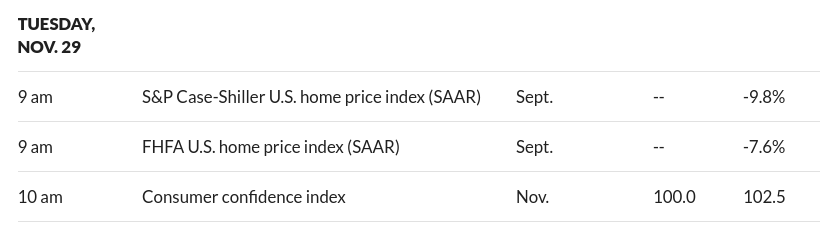

So today we have some housing data and some consumer confidence numbers. No reason to think these pieces of data will move markets absent major (huge) surprises. I think markets are focused on PCE (personal consumption expenditures) on Thursday and employment on Friday.

I didn’t do a thing yesterday–no buying or selling–in fact I only checked my accounts at the end of the day to see the bottom line–very tiny amount of red–almost a rounding error. As I mentioned before I like the end of the month since that is when dividends and interest roll into my accounts–kind of a silly thing really since the amounts are not exactly life changing–BUT over time it is real money.

Yesterday I paid $2.34/gallon for gas for my SUV–felt like the olden days. Locally we have a bit of a ‘gas war’ raging with prices much below the Minnesota state average prices–regional giant operator Kwik Trip is putting the hammer to competition–capitalism at its finest for consumers (although long term maybe not). Minnesota has a law that puts a floor under retail gas prices so we don’t see gas wars often, but it sure feels good to fill up for $30 once again.

I see another crypto brokerage firm went bust yesterday. I understand zero about crypto–I simplistically equate it to precious metals, but I can hold my precious metals in my hand. The concept of digital coins is a bit far for me–BUT if bitcoin ever went to $1 I would buy some just because–because maybe a more foolish person would pay me $67,000 for it someday.

Getting political and posting personal like and dislike posts about the fed is useless information. It does not belong here. Information about how we can make some money based on the Feds actions would be useful.

Removed

The fed is a domestic bank regulator. Recently they increased money supply by 20% per year for 2 years. While US GDP has been averaging roughly 1.3-4% growth. Seems like a lot of excess liquid in the bath tub.

If the FED completes all rate hikes as expected and keep rolling off $100B/mth by my calculations they would have brought monetary growth in line with GDP growth by March of 2023.

For the rest of the world the FED tracks the movement of US dollars (Eurodollar) using velocity of money. foreign governments are having a hell of a time finding US dollars to purchase materials and goods using up their reserves. This could eventually lead to a lot of deflation getting sent back to the good old US of A.

You nailed it….The reason we have inflation is because of the 20% increase in money supply. We added $6 Trillion into the system over 2 years…more than the previous 15 years combined.

If you look at a historical graph, whenever the M2 Money supply increased drastically, inflation peaked around the same percentage 6-9 months after. The Fed seems to be clueless about this matter and thinks that increasing interest rates will solve the problem….it won’t. The government spending must significantly slow down in order for us to have a chance at controlling inflation. The government throwing money at the railroad industry, increasing Social Security spending by 9% next year and other reckless policies will continue to add to the problem.

I totally disagree. Though I’m no fan of the Fed and 14 years of interest rate suppression. Nor Yellen’s decrees that have hurt Wells Fargo equity owners so badly, nor the Feds, the SEC, the US Treasury, the Office of the Controller of the Currency et.al. escape punishment and prosecution for their total incompetence in the lead up to the never ending 2008 Financial crises.

I see the current situation differently. The Fed has stated over and over again where their heading and what their target Fed Funds Rate is. Every miserable mass media and supposedly Business publication outlet have seemingly hired hundreds of 2 cent a word hack journalists to push back against this and write a sham article twice a day about hallucinatory signals only these journalists can see about a bogus Fed Pivot.

So, I don’t blame the Fed for any inconsistency recently. The blame clearly falls on tainted news, from tainted news organizations and a “Market that only wants to hear what it wants to hear.

Related to the Fed and getting inflation “under control.” I have posted before that Jay Powell wants to be remembered as Paul Volcker 2nd instead of Arthur Burns. Volcker is widely given credit for bringing the 1970’s inflation under control, whereas Burns is widely credited for letting it get out of control. An interesting recent article questions whether the underlying cause of lowered inflation was Fed action ala Volcker or other factors. Here is the executive summary of the article:

1) Decreased union participation in the 1980’s made it easier for US companies to NOT increase salaries as much. Reagan is credited with starting the union “busting” when he fired the Air Traffic Controllers that went out on strike. After that for a variety of reasons, union participation has continued to drop.

2) Offshoring/outsourcing to foreign countries with MUCH lower labor costs.

This is all related to the “Phillips Curve” which used to quantify the relationship between inflation and the unemployment rate. Long story short, the curve/theory has NOT worked the last few decades, which has puzzled economists.

The paper argues that without these two factors, inflation would have taken longer and been harder to get under control back then. The implication for today’s inflation situation is that we will NOT get the benefit of either of these factors going forward. To the contrary, if “onshoring” really takes hold, it will be a force to increase inflation.

Link to Fed paper on the Phillips curve:

https://www.federalreserve.gov/econres/feds/who-killed-the-phillips-curve-a-murder-mystery.htm

Link to Vox article on why Volcker/Fed was not solely responsible for lowering inflation:

https://www.vox.com/2022/11/2/23433474/federal-reserve-interest-rate-inflation-volcker

The Fed works for the banks not the people. Their priorities are different than ours. Much of the criticism results from forgetting that fact. Yes they make mistakes but they are not as boneheaded as they appear when assuming they have different priorities.

Tim—don’t hold back. Tell us how you really feel about the Fed.

Tim,

“The concept of digital coins is a bit far for me–BUT if bitcoin ever went to $1 I would buy some just because–because maybe a more foolish person would pay me $67,000 for it someday.”

Two Tim’s think alike! Enjoy your site, that made me smile today.

I suggest a different approach to anyone’s feelings about the Fed. For better or worse, for richer or poorer, we are married to them. And divorce is not an option. And like all spouses (present company excluded), you get the good along with the bad. It is a package deal. I have heard stories about people that try to change their spouse in some fashion, results are typically not positive. Likely the same outcome for suggesting the Fed alter their behavior.

The Fed deals the cards and we get to choose how we play the hand. . .

Tex – you are exactly right. I am just irritated they have no ability to follow their own rules. Speaking only for myself I pay little heed to them–I am data dependent.

I am not surprised, the Fed said they are going to “break things”…I think broken things are the data they are following. Unfortunately, they will only see the wreckage their rear view mirror, months after the destruction.

How are fed and NFL officials alike? Neither of them know how to do their

Job. Or maybe just corrupt.

** And Will Never Have A Clue

Not to be negative but I just thought adding a future tense to the title of the article would add some continuity and cover all our bases.

Being the holidays the first thing I thought of is ghost of Christmas past, present and future.

PickleNick—I try to look on the bright side – maybe SOMEDAY they will get it.

ha !

yup… (maybe)

cheers,

stay safe

Fed speakers may be acting rationally if they, or their relatives, are short the market. Huge profits from hawkytalk.

You said no politics so this comment is a placeholder. 😁

Consumer spending in my area was at an all time high if you count how many people were circling the parking lots looking for a parking space. Good time to get in line for gas at Costco. I was feeling pretty good that I paid $4.45 until I read what Tim had paid.

Didn’t spend a dime X-mas shopping, just the essentials like 55.00 for prescription cat food and 12.00 for a after Thanksgiving Turkey (.67#)

Cats eat better than I do

And I thought the 45.00 I pay for the prescription food my dog needs was expensive. Maybe there is a stock idea in all this?

Can’t complain new what I was getting into with a great dane. $800 for the dog. $2352/yr in dog chow costs.

Just a reminder, those clowns saved your portfolio in 2020. You got saved 2 years ago now you will give some of it back.

All I remember is those clowns keeping interest rates near zero far too long that it enabled many IG issues to be called away and replaced with much lower coupons at very high prices.

Bill…Yes, I had many issues called and, refusing to pay up for the low coupon versions, went out further on the risk curve with mixed results. Those low coupon preferreds, many of which have the same current yield as the higher coupon series from the same issuers, look pretty good now however, in that they will be the last to be called and you would receive a nice premium if it occurred. I guess from misery comes opportunity.

Yes, but they were a major reason for inflation which we all will cost everyone for years.