The OTC ticker is SNSHP as StackingNickels posted below.

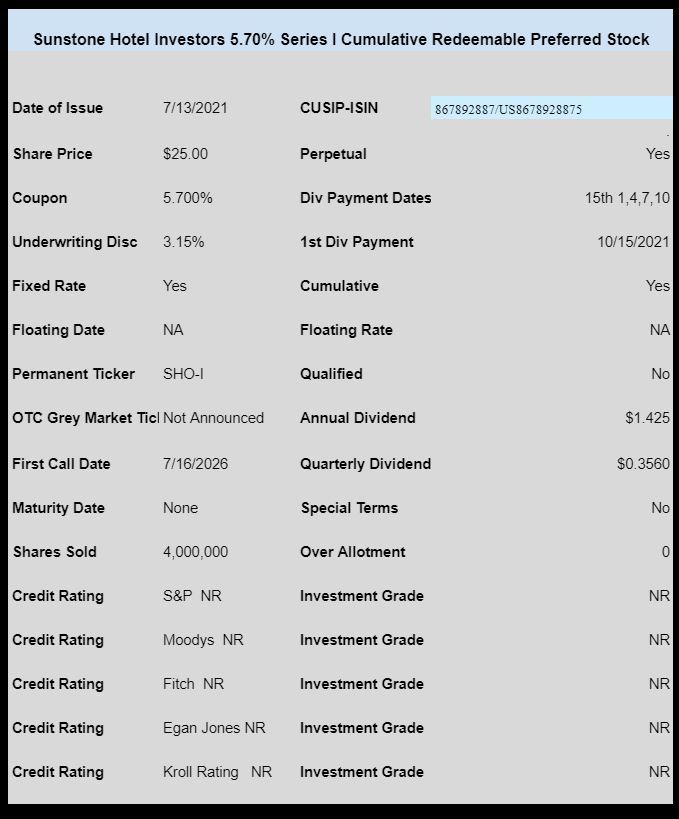

Lodging REIT Sunstone Hotel Investors (SHO) has priced their previously announced preferred stock issue.

The issue prices at 5.70%–.425% below their last new issue 2 months ago.

The issue is cumulative and non-qualified. It is unrated.

Proceeds from sale of 4 million shares will be used to redeem the SHO-F 6.45% issue which became redeemable last month.

The OTC grey market ticker has not been announced, but should be published this morning and the issue will trade immediately on the OTC grey market.

The pricing term sheet is here.

SHO-F Officially called – https://sunstonehotelinvestorsinc.gcs-web.com/news-releases/news-release-details/sunstone-hotel-investors-announces-redemption-6450-series-f

Sunstone Hotel Investors Announces Redemption of 6.450% Series F Preferred Stock

IRVINE, Calif., July 13, 2021 /PRNewswire/ — Sunstone Hotel Investors, Inc. (the “Company” or “Sunstone”) (NYSE: SHO), the owner of Long-Term Relevant Real Estate® in the hospitality sector, announced today it intends to redeem all 3,000,000 outstanding shares of its 6.450% Series F Cumulative Redeemable Preferred Stock (CUSIP: 867892-70-5). Series F Preferred Stock held through the Depository Trust Company will be redeemed in accordance with the applicable procedures of the Depository Trust Company.

The redemption date will be August 12, 2021. The Series F Preferred Stock will be redeemed for $25.00 per share, plus all accrued and unpaid dividends to, but not including, the redemption date in an amount equal to $0.183646 per share, for a total payment of $25.183646 per share, which will be payable in cash, without interest, on the redemption date. After the redemption date, Series F Preferred Stock will no longer be deemed outstanding and all the rights of the holders of Series F Preferred Stock will terminate, except the right to receive the redemption price. In addition, because all the issued and outstanding shares of Series F Preferred Stock are being redeemed, the Series F Preferred Stock will no longer trade on the New York Stock Exchange after the redemption date. The Series F Preferred Stock currently trades on the NYSE under the symbol SHO.PRF.

RE – SHO-F call – HOW ODD! Their math of paying 25.183646 means they are paying 41 days of accrued which means they are calculating from the EX-DIV date, not the 7/15 payment date… I’ve seen this before, but it’s certainly unusual…. it’s like a 6 cent bonus……..

They will figure it out and the 2nd assistant treasurer who did the calcs will get spanked.

Mr. C…good point but another piece of advise is that preferred stock is off balance sheet as they do not show up as debt. The real question would be: Is the company cash flow capable for servicing all the current debt + Preferred?

To correct slightly, the preferred is on balance sheet but as equity. If looking at the balance sheet or calculating coverage ratios one needs to re-pot the preferred with the debt. Not just the 1 cent per share par value but the hundreds of millions they have stashed under Additional paid in capital.

SHO is more debt heavy than the balance sheet, as presented, makes it appear. Not quite AHT but it isn’t PSA either.

Yes Bob…bad choice of words as it is in fact on the balance sheet but as equity as you call out. As SHO’s occupancy rate continues to rise, they should have the needed cash flow to cover both the debt service and the preferred dividend. A bonus, as it is cumulative, so we get a catch up if needed!

Are you buying this one ?

I have it on authority that a group purchased $100 million of the new SHO.

The cool thing Leo, is that no matter the public company, or what the company sells, or what the company does to make money, they all have one thing in common. They have financial documents that they publish. So “is this a good company” is a very different question than, “How much debt do they have?” You have to come up with a list of financial #’s that all add up and have weightings that give the answer to, “is this a good company?” There has been some good books published, as well as specific articles on how to read the financial statements. If you do this, then you can come up with the answer for your own risk tolerance. Also, some here are also buying investments for “not so great companies,” so that we can diversify and invest let’s say 10% in high risk. For this latter group, you just want to make sure they don’t go bankrupt.

If you don’t take the time to do your own analysis, then it might be good to get a financial advisor. Otherwise you will have to find someone here that you read their posts that you trust, and say, “Hey Grid, would you invest in this company?” They would give you quick advice, but then you are not doing your self service by trying to analyze a company and the specific investment. You are simply wanting someone to tell you what to do each time a new bond or preferred comes to market. That might be best to purchase a service from one of the great service providers of Seeking Alpha 🙂 But at least new issues some would do a write up on.

Thanks for patient reply , appreciate it

Temp symbol SNSHP

Thanks StackingNickels

Trading at 25.16.

Trading any retail platforms?

SNSHP not valid symbol it at TOS, Fidelity or Schwab

Nor at eTrade. Is this the correct symbol?

Is this good company?

Sorry for asking these questions.

As a rookie I the preferred world, I know little of these companies !

Middling. If investing in individual issues would do well to do the research.

Leo:

SHO has one of the better balance sheets in the hotel REIT sector, but getting an all-time low yield of 5.7% for a preferred issued by this company is an extremely poor risk-reward.

Investors seem to be forgetting that this sector can be extremely risky at times.

I do believe that 5.7% does qualify as the lowest rate for a hotel REIT for a straight cumulative (non-convertible) preferred in the history of REITland.

Pass.

I totally agree the yield is ridiculous. Thanks for confirming.

Leo – Hotel Reits, Shipping, Insurance, Not Rated or Non investment grade (BBB/Baa) issues are inherently more risky but come with higher reward.

When a risk off (selling) event happens you can expect a greater amount of price movement and longer time for the price to recover.

Most do not want to recommend as they do not know your risk tolerance (age) or goals.

A common strategy with so many new offerings right now is to buy enough and wait for .25/.50 rise in price and book profit. New issues look extremely attractive as everyone is chasing yield.

This helps many with the QVC boxes arriving on the doorstep.

does it make sense to buy a couple of shares of SHO, and sell it in a few days to make some capital gains ?

In this market within the first week this issue will by 25.60-80. Easy lobster dinner money.

Well that sure makes more sense than buying a couple of shares and selling them in a few days and not having some capital gains to make….. lol…….. why I can remember the days when people actually had to consider that as another possibility… maybe back when a McDonald’s hamburger was 19 cents…