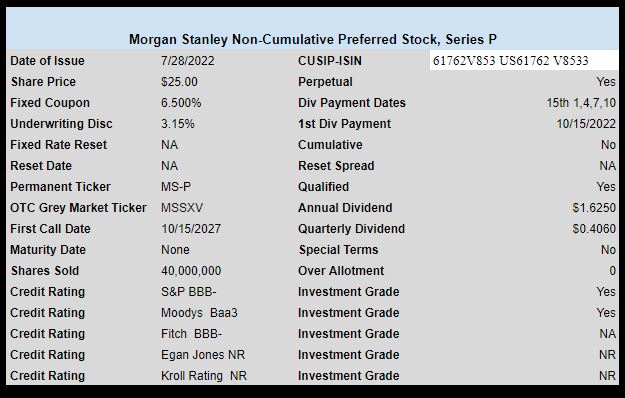

Morgan Stanley (MS) priced the previously announced preferred stock.

The 40 million share issue prices with a 6.50% coupon. The issue is investment grade.

The issue is non cumulative and qualified for preferential tax treatment.

MS has lots of preferred issues currently outstanding which can be seen here.

The pricing term sheet can be found here.

OK this looks bad but the last two numbers on furtherest to right are Half 1 and Half 2 back to 2012.

No great deal VS preferreds. And seeing the number can go to zero I suppose the escape valve is one can get out just giving up on the first 90 days. So if they tank again you just bail.

Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec HALF1 HALF2

2012 2.3 2.2 2.3 2.3 2.3 2.2 2.1 1.9 2.0 2.0 1.9 1.9 2.2 2.0

2013 1.9 2.0 1.9 1.7 1.7 1.6 1.7 1.8 1.7 1.7 1.7 1.7 1.8 1.7

2014 1.6 1.6 1.7 1.8 2.0 1.9 1.9 1.7 1.7 1.8 1.7 1.6 1.8 1.7

2015 1.6 1.7 1.8 1.8 1.7 1.8 1.8 1.8 1.9 1.9 2.0 2.1 1.7 1.9

2016 2.2 2.3 2.2 2.1 2.2 2.2 2.2 2.3 2.2 2.1 2.1 2.2 2.2 2.2

2017 2.3 2.2 2.0 1.9 1.7 1.7 1.7 1.7 1.7 1.8 1.7 1.8 2.0 1.7

2018 1.8 1.8 2.1 2.1 2.2 2.3 2.4 2.2 2.2 2.1 2.2 2.2 2.1 2.2

2019 2.2 2.1 2.0 2.1 2.0 2.1 2.2 2.4 2.4 2.3 2.3 2.3 2.1 2.3

2020 2.3 2.4 2.1 1.4 1.2 1.2 1.6 1.7 1.7 1.6 1.6 1.6 1.8 1.6

2021 1.4 1.3 1.6 3.0 3.8 4.5 4.3 4.0 4.0 4.6 4.9 5.5 2.6 4.5

2022 6.0 6.4 6.5 6.2 6.0 5.9 6.2

Opps sorry tim wrong thread

More mystery on how/why this issue was priced @ 6.5%. Make two dubious assumptions for just a second:

1) All Moody’s Baa3 rated preferreds are truly equal as to non-payment probability.

2) With the current interest rate situation, we are going to NOT consider Yield to First Call, i.e. we are going to assume that every issue will be outstanding ad infinitem

With those two assumptions, I show 54 Baa3 rated prefereds that traded yesterday, 7/29. The median current yield of all was 5.55%, so the Morgan Issue that came to market @ 6.50% was way out of line. I also removed all convertible issues.

Here are the top 20 issues sorted by decreasing current yield:

FITBI, 6.27%

MSSXL, 6.24%

ZIONO, 6.09%

BAC-B, 5.94%

AXS-E, 5.88%

FITBP, 5.88%

ASB-E, 5.88%

FCNCP, 5.87%

BAC-K, 5.8%

COF-J, 5.76%

KEY-I, 5.74%

COF-L, 5.74%

HPP-C, 5.73%

HIG-G, 5.72%

WAFDP, 5.67%

KEY-J, 5.67%

KEY-K, 5.63%

DLR-K, 5.62%

FULTP, 5.61%

ACGLN, 5.6%

Maybe some of the ratings I have in my database are out of date, but the Morgan issue really stands out to me. I am guessing the price will rise to cause the current yield to fall more in line with the median. I find it hard to believe that it has the second highest non-payment probability of all of the other issues.

We currently do not hold this in any account or have any open orders. I am strongly considering:

a) Buying some in non-margin accounts

b) Buying a lot and shorting a correspondingly rated issue with lower yield in margin accounts. Aka a pair trade.

Obviously, this analysis might be 100% wrong. In particular, if ALL preferreds tank, it could be ugly. Although it might not be as ugly as holding some of the ones with lower current yield.

What is surprising to me is how Morgan and the underwriters could misprice so badly, costing Morgan money. It closed today @ 26.06, so clearly they could have sent it out at a lower coupon rate. Probably could have floated it @ 6.25 instead of 6.5. . .

Agreed Tex – seemed to be lots of demand from big players in the 25.90 – 26 range so Morgan could very well of priced this at 6.25%

Probably didn’t hurt demand either that there has been a dearth of new issues as of late

I actually bought more TRINL than MSSXL. While the Morgan issue is investment grade and Trinity is obviously not, TRINL has a short maturity of 1/16/25 and a fixed 7% rate. With it selling with a month and a half of accrued interest, I was able to get it around 20-25 cents over par. But I like them both

Nobody I know who got filled was crying about the rate being too high.

Was any of you able to buy below $25.85?

Sprinkled in among all the orders at $25.85 and above (most in the $25.9x range), I see (via Power E*TRADE, for what it’s worth) a tiny fraction of the day’s orders ranging from $25.10 up to $26.778. The volume on each order is high by my standards (5k – 25k), but no higher than the volume of orders at much higher prices.

For the brokers among you: are those dealer-to-dealer orders?

Merrill shows the pricing but not allowing OTC trade.

This is strange as I have done it in the past.

Will try again Monday I guess.

But I feel the train will have left the station by then.

Bur–my order was a day order with a limit of 25.90 and it did not execute.

No, I would have liked to get it at $25.85 or less but I was not around in the morning and by the time I place my order, bids were around 25.95. And even then I had to wait a while for a fill as like you noticed, the orders being filled were typically much large ones

Just delicious.

Neither ticker showing up on schwab.

MSSXL shows up at Schwab

I see 25.90 not too shabby for one day.

Now 25. 10…hmm below par wouldn’t surprise me. I’d think 24.65-70 a natural level post offering.

Lol now I see 25.95

I think Morgan Stanley badly mispriced this one.

Currently trading at 26 for a yield of 6%

Seems like they could have cut the coupon to 6% and still sold this one in this market.

When MS is representing MS, they don’t give a hoot about the other underwriters or selling syndicates etc. And who is going to get mad MS issued a ‘high’ rate? They underwrite to their own investors. After one of the worst bond markets to start a year of all time, they did their investors a solid if you ask me. Compared to most $25 pfds and $1,000 preferreds being down 15-25% across the board, it’s nice to get a win for a change.

The real Q is who had the balls to buy in this market. And who’s next and what rate will they pay. Me I wasn’t happy it slipped to 6.5 from 6 7/8-7. If a big one comes at 6.25 I’m probably not touching it.

same symbol and price on TDA at 11 o’clock

I believe the OTC grey market ticker is incorrect.

I see the ticker as MSSXL at otcmarkets.com

First day or two those tickers change and often are dummies or backup symbols. Not unlike you having an account at brokerage with check writing/where the checking account has a different account number.

Its neither, the V in the ticker stands for “when issued”.

That looks correct but Fidelity won’t let me buy OTC.

Fidelity doesn’t show bid/ask prices but let me put in a buy order.

Was able to buy both MSSXL and TRINL today via Fidelity without a problem

Was also able to by MS via Fido–truly surprised.

I gotta say I get the feeling that Fidelity’s coming around a bit – they’re becoming easier to work with what with loosening their f/f trading restrictions and getting quicker on the draw with issues like this.. Heck I’ve noticed where they seem to be allowing bidding on some dark issues as well…. Couple that with the more interesting opportunities in the bond market overall now with the increased interest rate levels and I’m liking Fidelity more. Even their Active Trader Pro platform seems to be becoming a more valuable platform than before thanks to a few recent changes. On the other hand, I’m feeling Schwab influences creeping into TDA enough to make me consider moving some cash from TDA to Fidelity, especially TDA, with only Schwab funds available for sweep accounts, still offers next to nada yields on idle funds. Moving funds FROM TDA to Fidelity was never even worth thinking about in the past..

Yeah 2WR – I never had a problem with Fidelity and years ago consolidated all my brokerage accounts (and I had them all ) into one at Fidelity. Just easier to manage and deal with everything at one institution

Yeah their old f/f trading restrictions were a pain but given that I typically only was buying them a handful of times a year, making a phone call to get the trade done on a f/f never bothered me much. Although I will admit now that you can trade f/f issues online with no restrictions, I probably have bought and sold them much more in the past. Mainly due to the environment we are in these days that made several f/f issues more attractive to me where I used to mainly stick to fixed rate. So it was nice that they loosened that restriction when they did.

Did the same Libero