Futures markets are looking pretty soft this morning with both the DJIA and S&P500 looking down almost 1%. Interest rates are popping a bit with the 10 year treasury yield at 3.89% at this moment (6 a.m. central)–if economic data shows strength this week we may well see the 10 year yield over 4% once again.

Overall last week was a quiet week for equities as the S&P500 fell by 1/4%, although the index was up as much as about 1 1/2% mid week–with the CPI and PPI both being reported in the same week things ended up somewhat ‘calm’.

The 10 year treasury yield moved 8 basis points higher on the week to 3.83% from the close the previous Friday. On Friday the yield had hit 3.90% before backing off into the close. Economic numbers continue to be somewhat stronger than anticipated–in particular employment related data is not showing substantial weakness. Time and time again Fed chair Powell has reiterated that he watches the employment numbers closely.

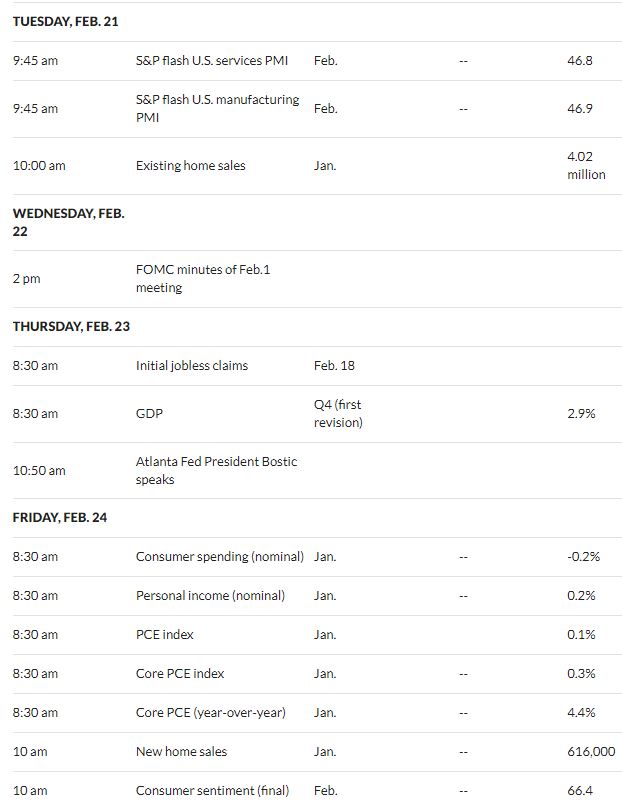

Once again we will have plenty of economic news this coming week. We have the Q4 1st revision of GDP–likely not a market mover. We have FOMC minutes on Wednesday–and while this is old news it almost always moves markets as participants parse every single word. On Friday we have the personal consumption expenditures index (PCE) being released and the Fed chair has indicated that this is his favorite inflation data.

The Federal Reserve balance sheet assets fell by a giant sized $50 billion. Of course it was flat the previous week so a big drop was going to come sooner or later.

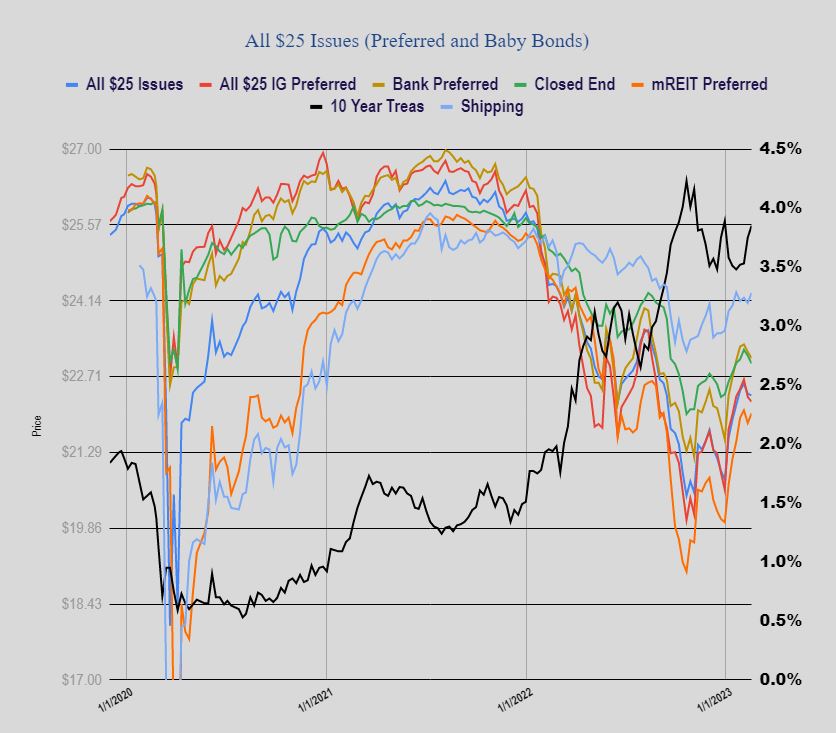

The average $25/share preferred stock and baby bond fell by just a bit last week – 3 cents. Investment grade fell by 9 cents with banks off 10 cents. mREITS jumped 18 cents with shippers up 19 cents. So quality issues down and high yield junky issues bouncing.

Last week we didn’t have any new income issues priced.

Been laddering 3-, 6-, 9- and 12-month T-Bills the past several weeks averaging at right about 5% . 35% of my portfolios. Fixing to retire at the EOY and foresee a pretty crazy environment here the rest of 2023 into 2024 so want the safety for the time being. I’ll re-evaluate whether to re-ladder or use the funds to buy stocks as these mature. Another 30-35% of my portfolio is IG fixed-to-floating and the balance are other preferreds and some divvy-paying equities. Very small technology positions that pay divvy (think QCOM). I think I am pretty adequately sheltered from the potential storm coming.

Any concerns with all the talk of government hitting limits this summer and potential debt defaults.

Concerns about that and a number of other things that could hurt the economy. But not enough to do much about it other than to know there is some systemic risk. If the economy implodes everything goes down with it.

Personally I have been in ostrich mode over the debt limit.

But, if I wanted to place a small black swan bet on default happening, what would be a good way to do that? Just buy QQQ puts? TLT puts?

Long puts are more effective at protecting as well as profiting if your timing is impeccable. If not, theta decay will erode the value of your puts unless you go out a year or more. You can lower the cost by doing a vertical spread but that caps the gain from a market drop.

On occasion, I do a one year vertical on the IWM or SPY that is 10% wide and 10% out-of-the-money. It tends to cost about 1.5% of the principal being hedged (a 1 year ATM put currently costs about 7.5% which is a lot of drag on a portfolio).

If the market oscillates during the year, I can usually get the cost of the spread down near zero with a few adjustments. Later in the year, when the short leg is near worthless, I cover it and end up with long puts. In 2020, when Covid hit, such long puts saved my bacon (the hit on my long stocks).

The short answer is that risk and reward go hand in hand. Better insurance costs more. More potential profit costs more (long puts). A larger deductible (OTM puts) costs less.