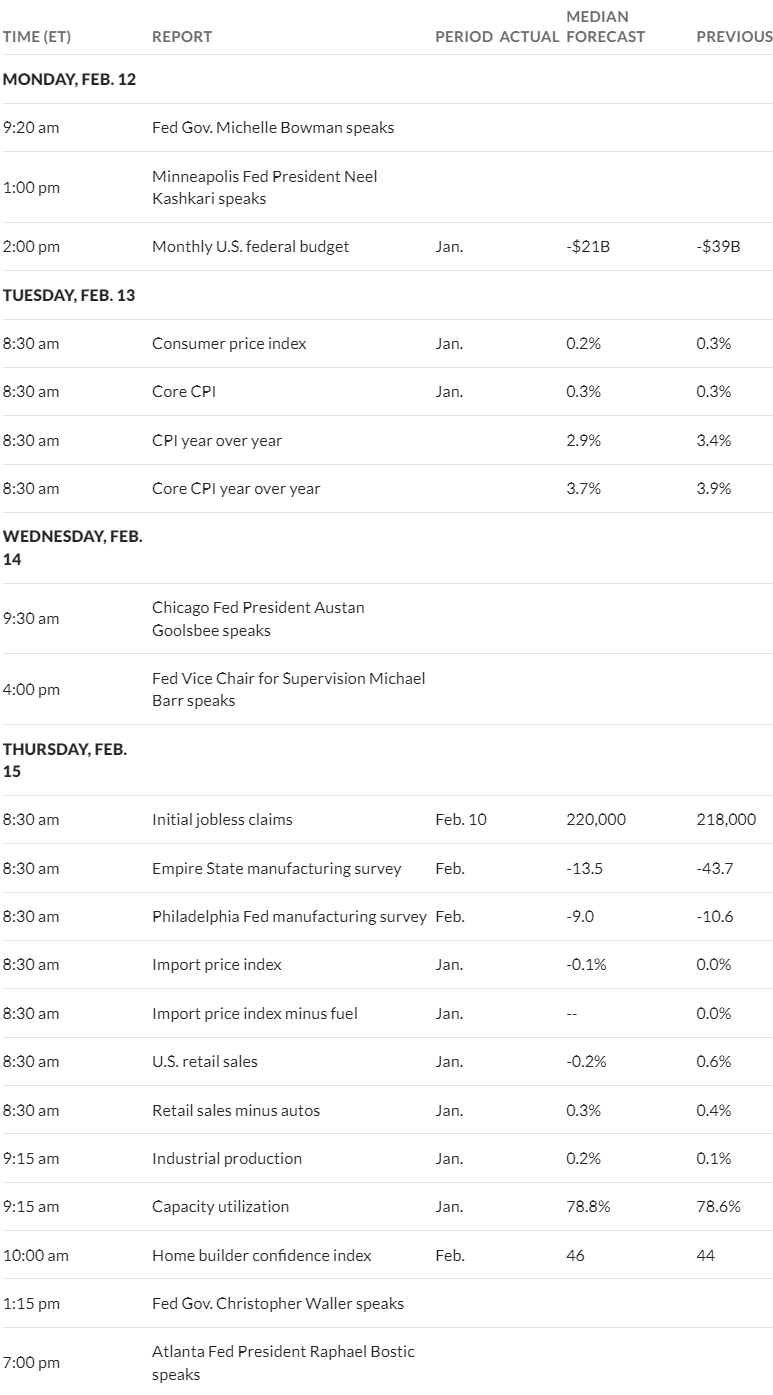

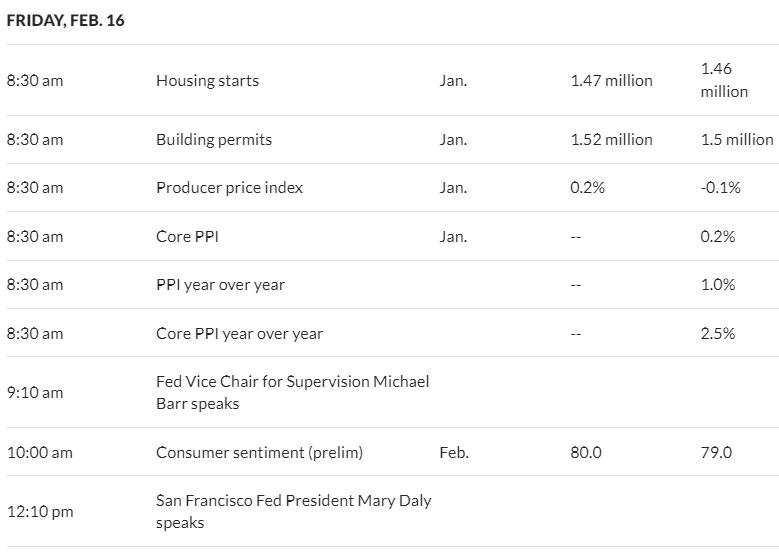

Well it is almost certain to be a exciting week with meaningful and important economic news – the consumer price index (CPI)and producer price index (PPI).

Last week the S&P index continued to hit record highs–up we go. The index closed Friday at 5027 which was up 1.4% from the close the previous Friday. The index is still being lead by the tech sector–one has to wonder how long this tech melt up will continue.

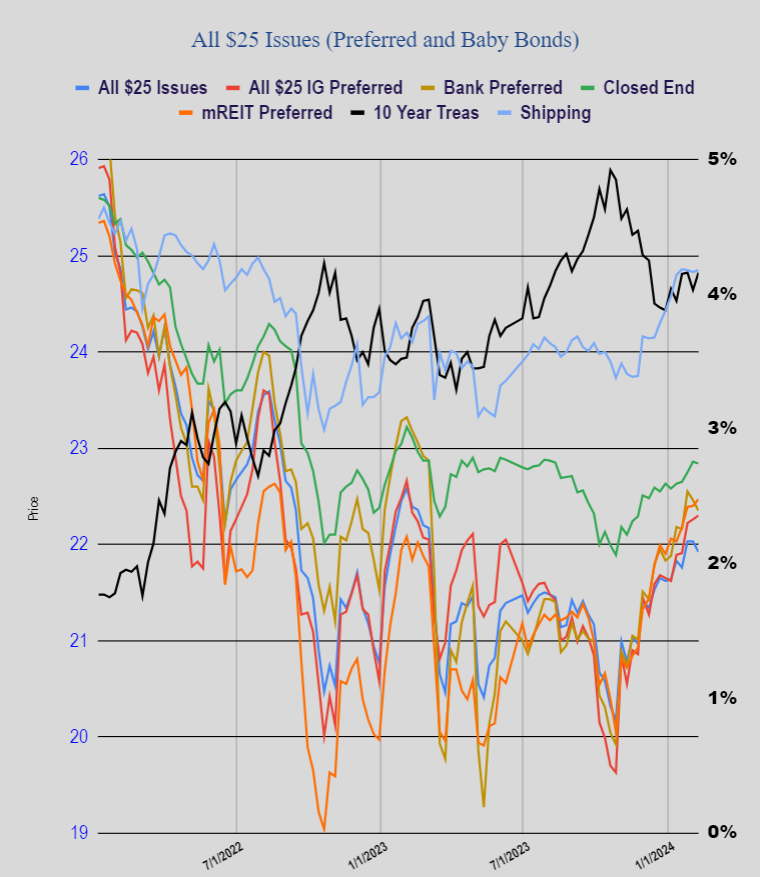

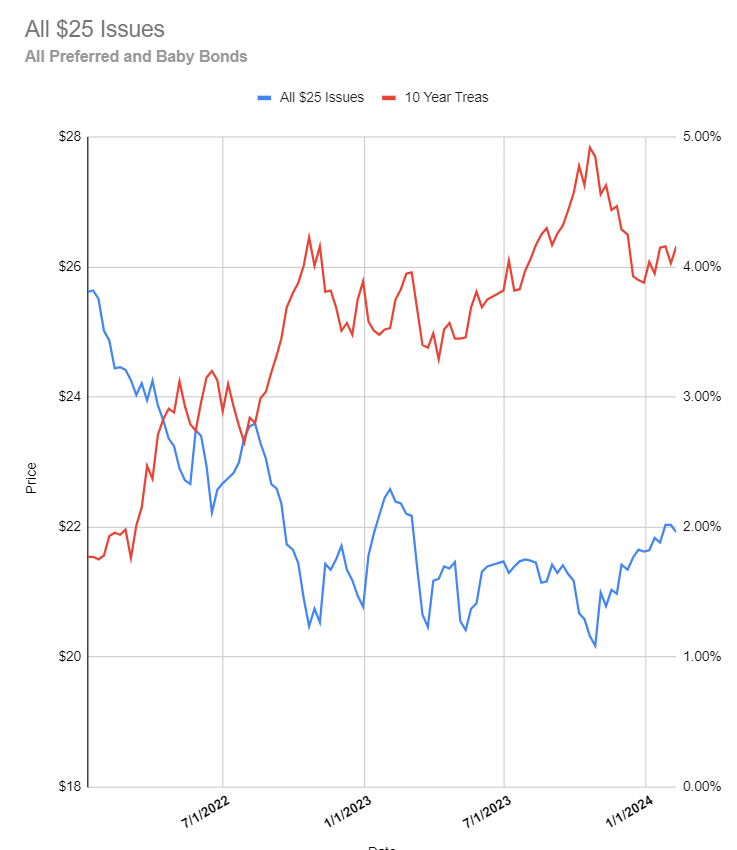

The 10 year treasury yield closed the week at 4.19% which was 16 basis points higher than the close the previous week. The yield continues to trade in the 3.80% to 4.20% range, but with the consumer price index being released tomorrow we could see movement out of this range–we’ll see.

The Fed balance sheet rose by $1 billion last week after falling by $47 billion the previous week.

The average $25/share preferred stock and baby bond moved lower by 8 cents last week–surprising given the rise in interest rates on the week. Investment grade issues rose 4 cents , banking issues fell by 11 cents. mREIT issues moved 7 cents higher and shippers were 2 cents higher.

Last week we had no new income issues priced and finally all previous income issues are trading.

RILYO has a ‘partial redemption’ on 2/29/24

I’m losing complete track of what’s been called. STT d, fitbi wfc R?

It’s as if my screens lost interest in tracking!!

I don’t believe FITBI got a redemption notice. Did I miss it?

(The other two you mentioned will be redeemed. Also FNB-E later this week.)

Evidently it’s not only an internal problem for me…. Some of this is DTC problem too.

also called = Ni-B and AIG-A both for 3/15

OK no call on fifth third, it’s state street D called in full. I see it’s an issue across th e board even Quantum is MIA

Tim, Your laundry list heeds updating. Ni-B has announced a call.

Charles–am aware of the call Charles–unfortuantely.