Here we go with another week with all indexes trading at or near record highs. Tech stocks continue to lead the way so the NASDAQ has been really flying–up 1.7%. These tech stocks are the big driver of the S&P500 so it has been drug higher and higher–up 1.3.% on Friday.

The S&P500 closed the week near 4840 which is 56 points higher than the close the previous Friday–so once again up over 1% on the week.

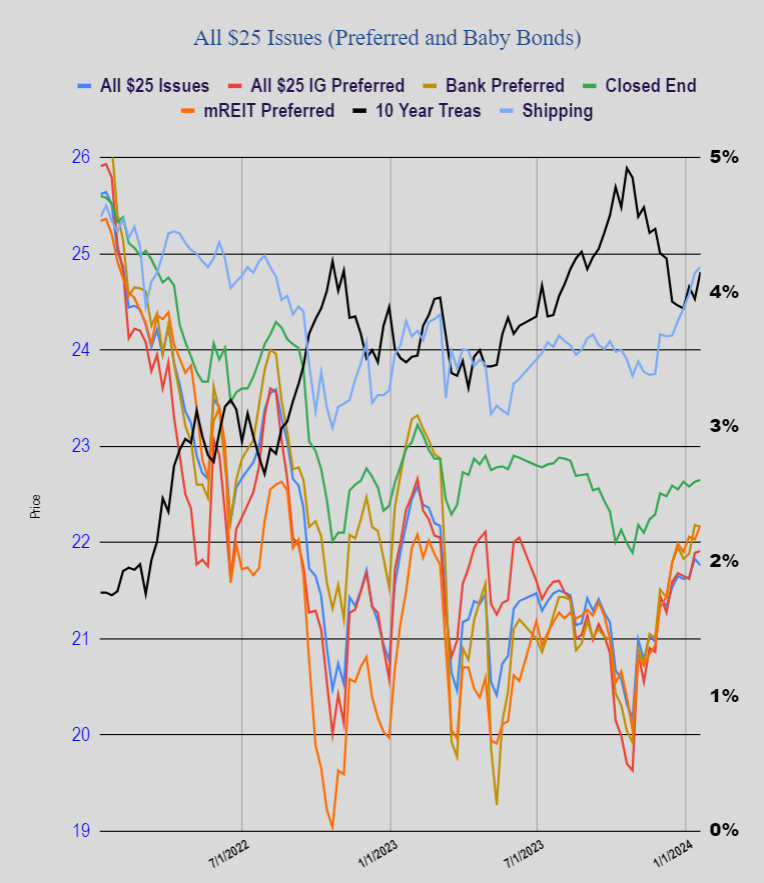

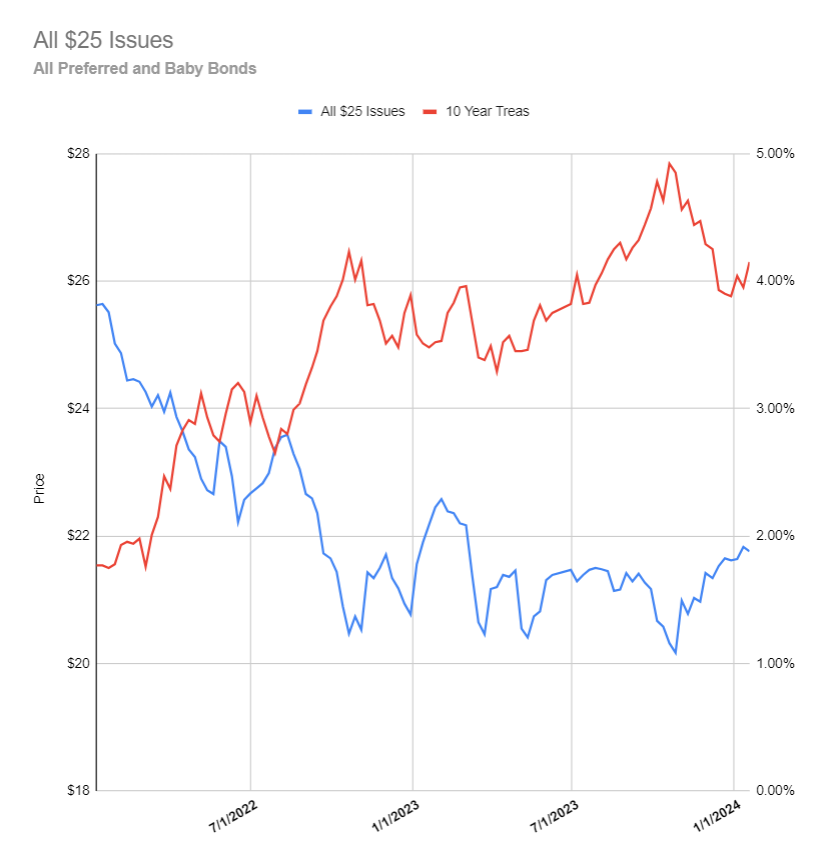

The 10 year treasury closed the week in the 4.14-4.15% area which is almost 20 basis points higher than the close the previous Friday (3.95%).

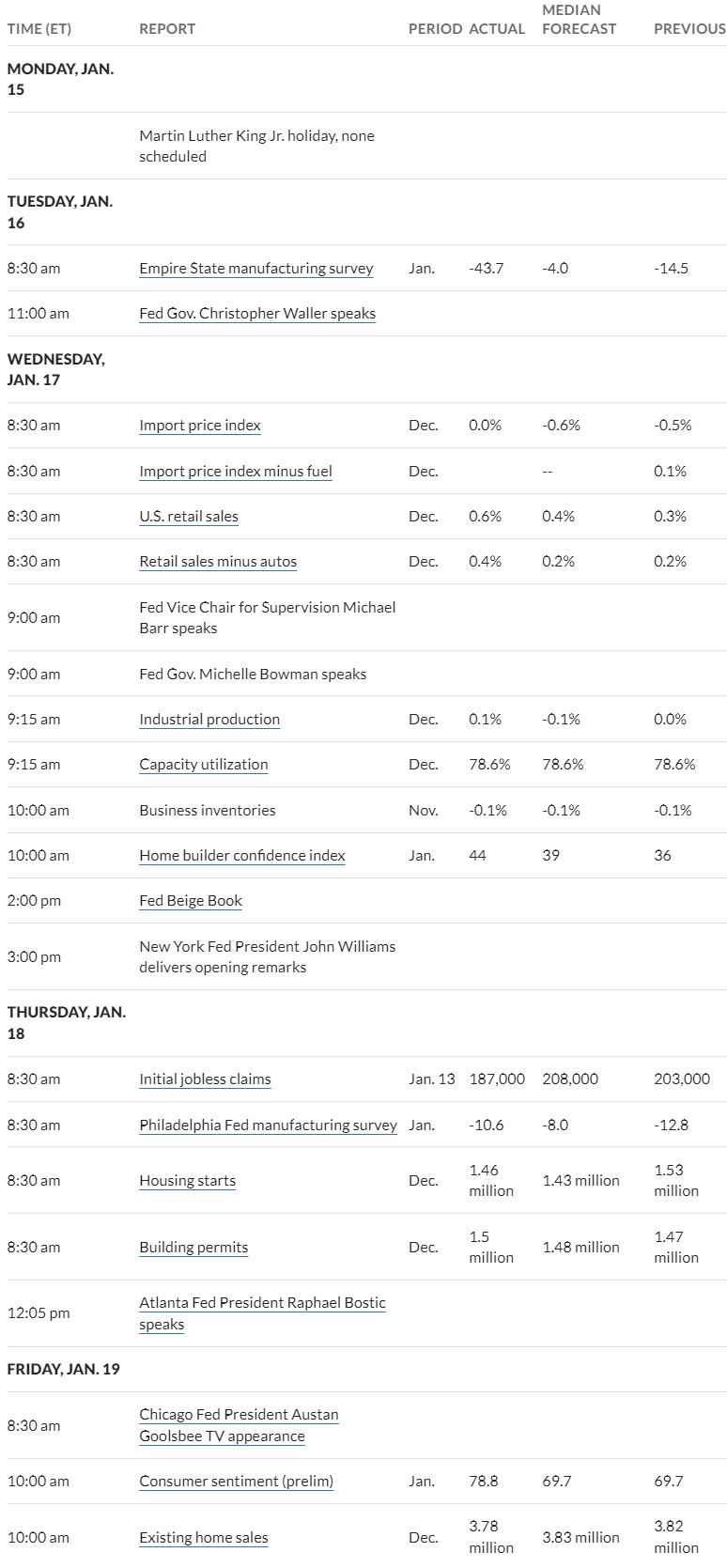

Last week we had economic news that showed the economy is still holding up well with retail sales much stronger than forecast and 1st time unemployment claims coming in at 187,000 versus expectations of 208,000. Certainly these types of numbers served to drive interest rates much higher.

This week we have the supposed most important inflation gauge with the personal consumption expenditure (PCE) being released on Friday. And of course there is plenty of other economic data being released–but at least we have no Fed yakkers as they are in a quiet period leading up to the FOMC meeting next week.

The Federal Reserve balance sheet fell last week by $13 billion to $7.68 trillion.

Amazingly last week the average $25/share preferred and baby bond fell by just a tiny amount–7 cents. Investment grade issues rose 2 cents, banking issues fell 2 cents with mREIT preferreds up 15 cents. All in all a stellar week for income issues considering interest rates rose by 20 basis point.

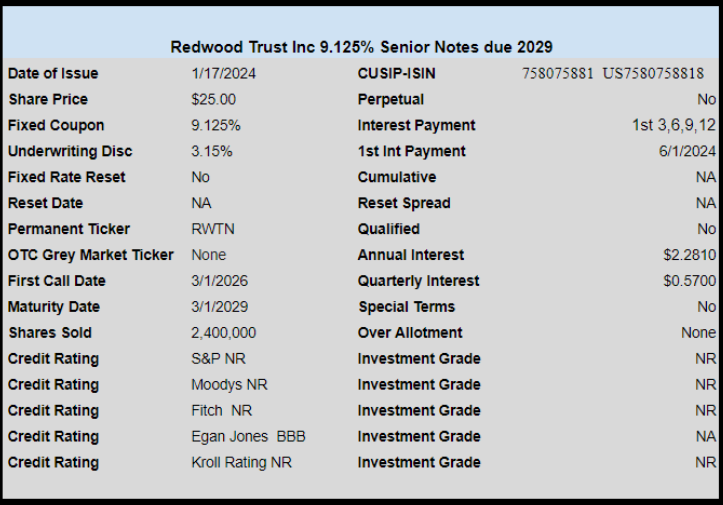

Last week mREIT Redwood Trust (RWT) priced a new issue of baby bonds with a coupon of 9.125%. The issue is not trading yet, but should trade sometime this week.

MFAN, ECCF, RWTN

Noone is trading yet.