Well overall last week was a quiet week with the S&P500 moving very little week over week and the 10 year treasury mirroring the stock markets.

The S&P500 moved higher by almost exactly 10 points last week closing the week at 4604. The index moved in a range of 4546 to 4609–it is seldom tha the index moves in a range of just over 1%–some indecision as where we go next.

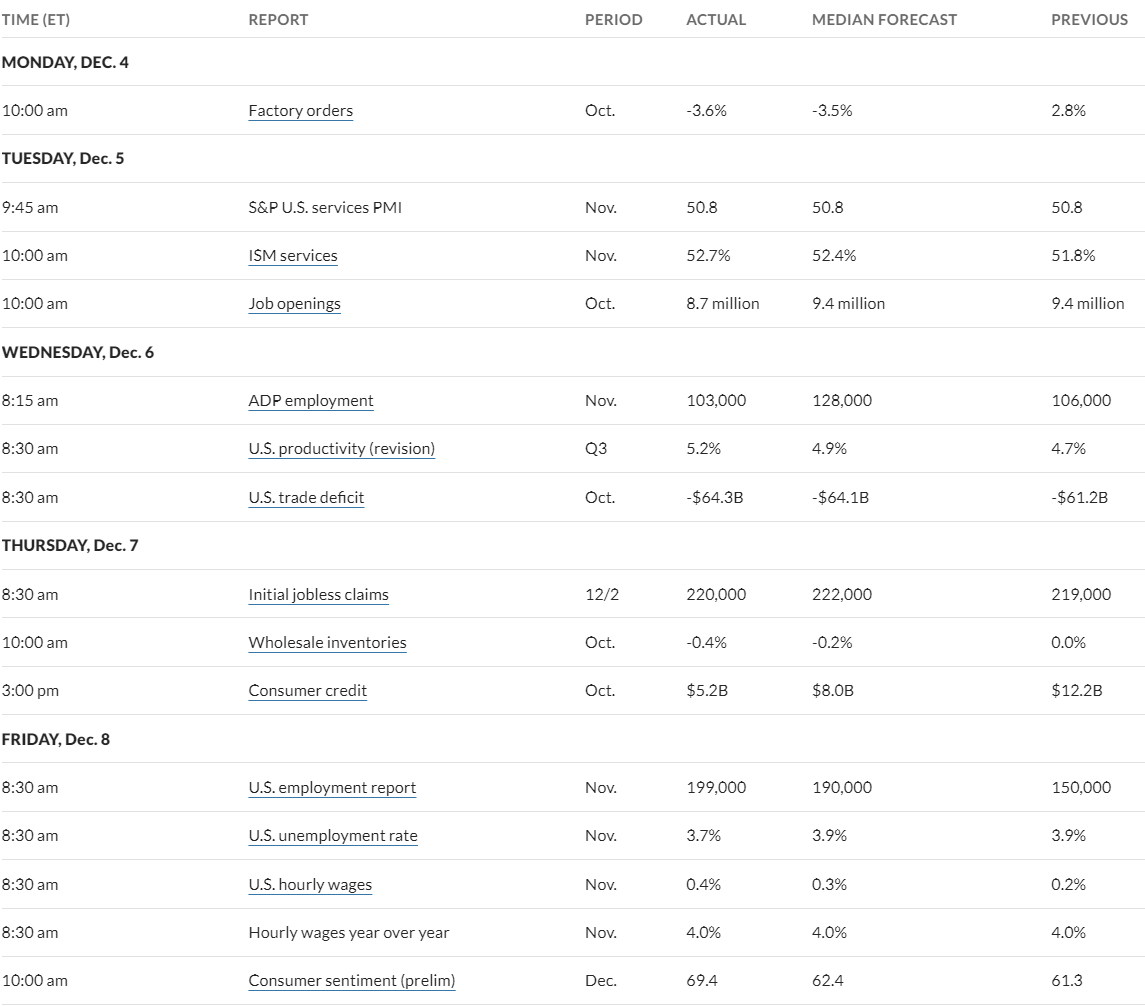

The 10 year treasury got as low as 4.10% and as high as 4.30% before closing the week at 4.25%–up a measly 2 basis points from the close the previous Friday. Economic data from last week included monthly employment reports–from ADP and the government report. ADP showed weakness with 103,000 private payroll jobs (weaker than expected) created in November while the government report showed 199,000 new jobs created versus 190,000 expected. The unemployment rate fell to 3.7% from 3.9% (versus 3.9% expected).

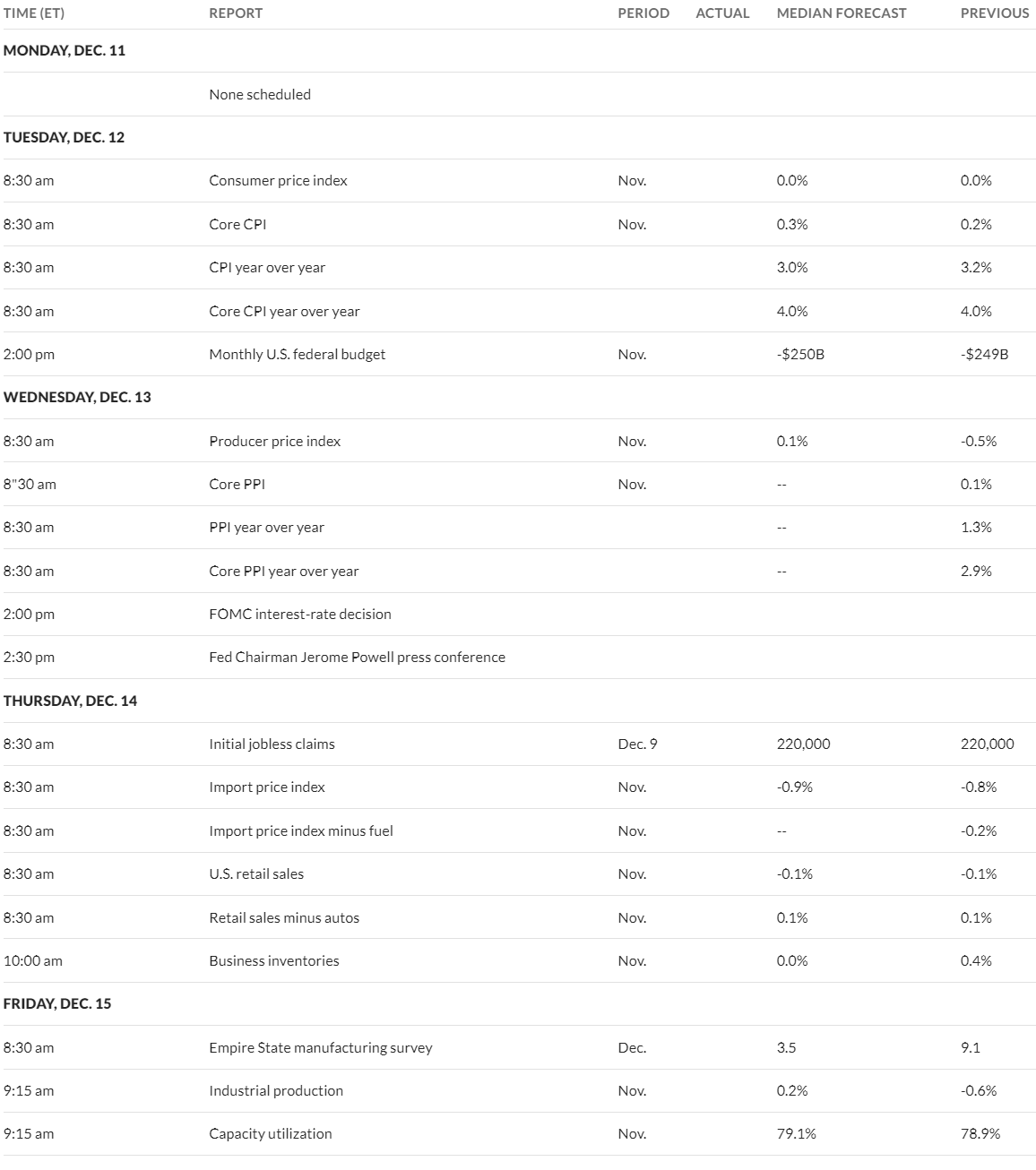

For this week we have the important CPI and PPI reports (consumer prices and producer prices) as well as a FOMC meeting starting on Tuesday and wrapping up on Wednesday with an announcement at 1 p.m. (central) on policy changes and a 1:30 pm (central) press conference with Jay Powell.

The Federal Reserve balance sheet plunged by $59 billion as the Fed continues to run their quantitative tightening program at a runoff of $85 billion per month.

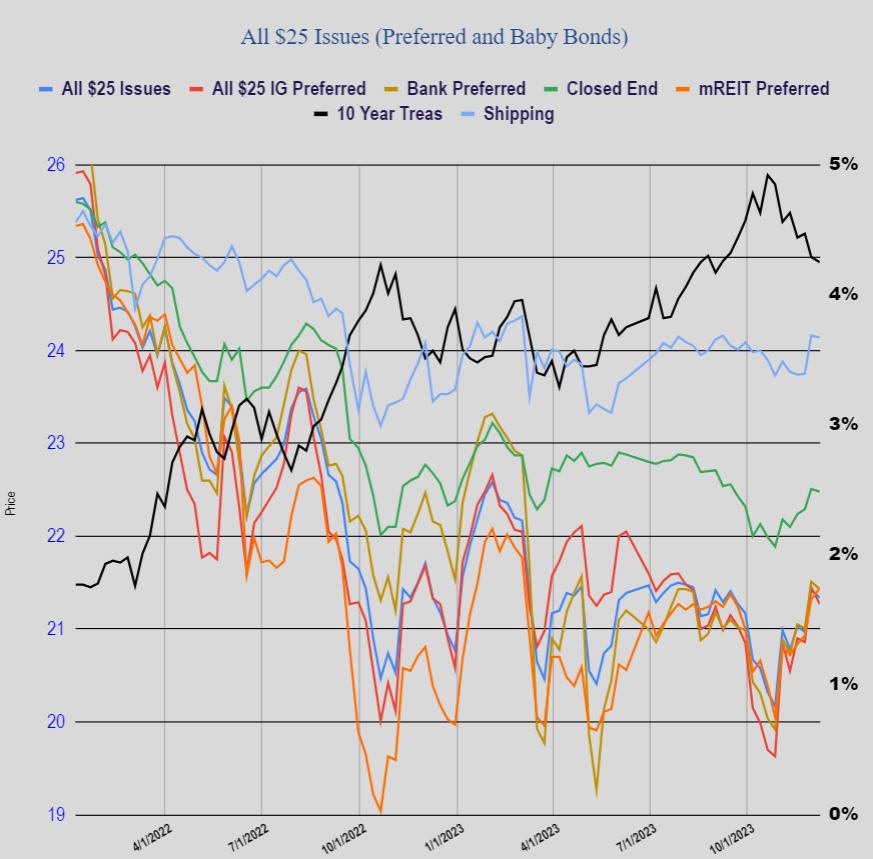

Last week $25/share preferreds and baby bonds, just like common shares, moved very little. The average share price fell by 8 cents/share. Investment grade issues fell 18 cents, bankers fell by 8 cents, mREIT preferreds rose by 12 cents and shippers were 2 cents lower—all in all a quiet week

Last week we had Midcap Financial Investment (MFIC) (the old Apollo Asset Investment) sell an issue of 8% baby bonds. MFIC is a BDC. Details are here.