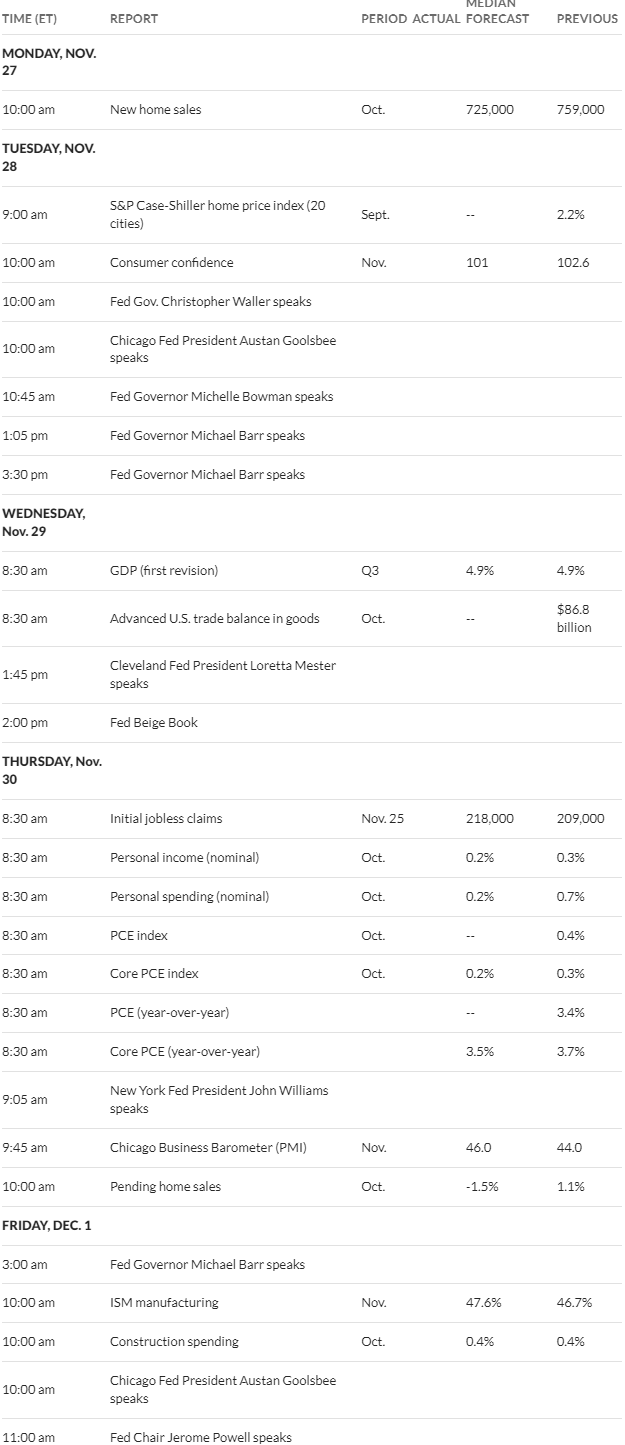

Well we get back to normal this week after a pretty quiet Thanksgiving week in the U.S.

The S&P500 moved higher by exactly 1% from the close on the previous Friday. Most of the gain came on Monday with the balance of the week drifting with the Thursday holiday.

Interest rates didn’t move too much last week either as economic news was lite and not of the type that moves markets too much. The 10 year treasury moved 3 basis points higher to close the week at 4.47% versus 4.4% the previous Friday.

This week the economic calendar is not overly heavy (although way too many Fed yakkers), BUT the main show of the week will be the personal consumption expenditure (PCE) number which will be released on Thursday. Seems to me that a soft number on this data point will cement a ‘no hike’ at the December 12-13 FOMC meeting.

The Federal Reserve balance sheet assets number was not released last week because of the Thanksgiving holiday–we will see if they provide an update today.

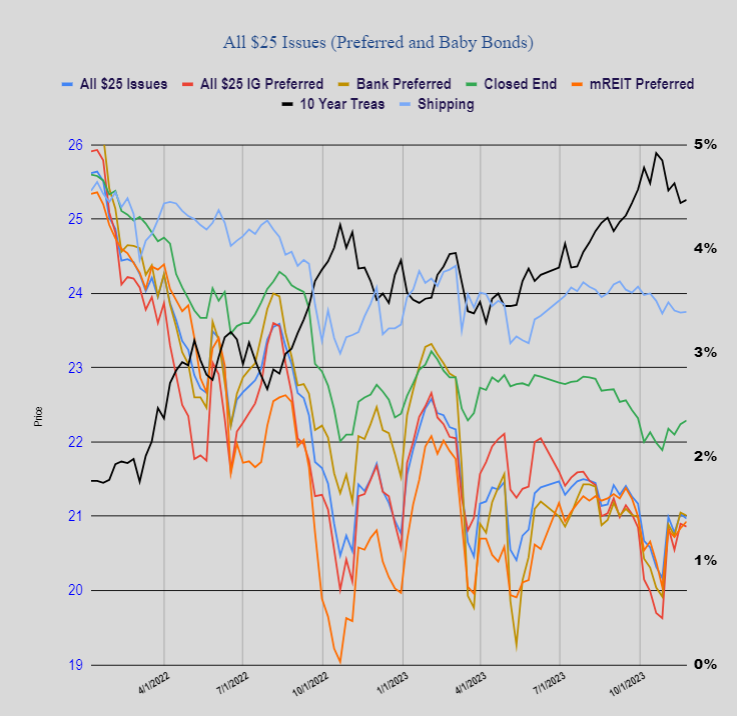

Like everything else $25/share preferred stock and baby bonds just barely moving – down 6 cents. Investment grade issues were off 4 cents, banks off 4 cents and mREITs up 9 cents.

Last week–as normal we had no new income issues priced.